Macroeconomic Update

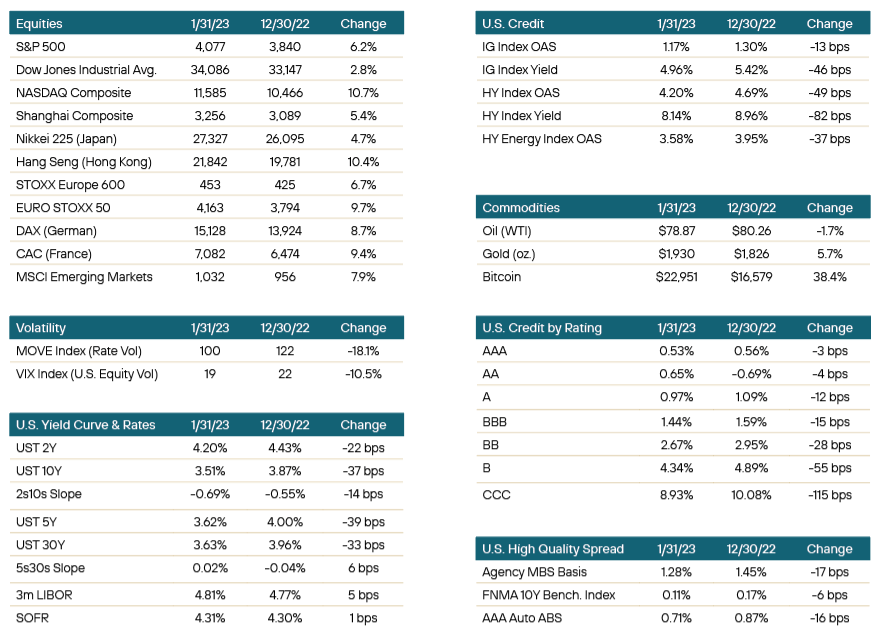

The new year in the financial markets got off to a strong start. January featured a global rally in equities, lower interest rates across the yield curve, tighter credit spreads, and diminished volatility. Economic data releases and central bank meetings continued to drive activity, as they have for some time.

Ongoing tension persisted between market expectations for the Fed Funds Rate versus Federal Reserve forecasts. The Fed says they won’t cut rates this year while rate futures prices disagree, anticipating a cut in September. By late January, markets had even priced in a good chance for a second cut in 2023. FOMC meeting minutes released the first week of the month noted this, indicating that “markets may have a [dovish] ‘misperception’” that has the potential to “complicate” the Fed’s inflation fight. Investors expect one hike in February and one last hike in March to complete the cycle. The Fed, on the other hand, still sees a terminal rate north of 5% and its balance sheet has seen runoff north of a half trillion dollars within the last year.

Key economic data points this past month, per usual, were non-farm payrolls, CPI, and GDP. NFP showed a lower employment rate to beat the headline estimate, but average hourly earnings were below expectations. This deceleration was good news for the Fed, and U.S. Treasuries rallied. A week later we received the December CPI report and it was just as expected; the headline figure declined 0.1% and produced a decline in the 12-month inflation rate from 7.1% to 6.5%. Core CPI remained elevated due to rising shelter costs and higher owners’ equivalent rent. On the other hand, used vehicle prices fell 2.5%. Following CPI, the Producer Price Index (PPI) showed a nice decline, arriving at 6.2% compared to a 6.8% forecast. Lastly, towards month end, the GDP figure came in hot, as did jobless claims, indicating the Fed is still not seeing its hoped-for labor market weakness. The hawkish data brought about a selloff in rates, but not nearly enough to offset the large rally in yields from the inflation number earlier in the month. 5s, 10s, and 30s all rallied between 33 and 39 bps month over month, while the 2Y UST was lower by 22 bps. Supporting the rally in yields was the Bank of Japan, which dismissed concerns over recently policy tweaks. The BOJ stood pat with its ongoing stimulus program.

Portfolio Review

New year. New attitude. What a difference a few weeks can make. The minute the calendar turned over, there was suddenly an influx of interest and what seemed optimism in the markets. Whereas the last year ended with a lot of sitting on hands, the new year has launched with multiple issuers, investment grade and high yield, racing to market. The primary market new issue calendar has been an active platform with seemingly four to five corporate deals a day being announced, and in several ABS deals using the week for marketing purposes. Dealers have used this exuberance to not only help issuers get the funding they need, but to also off-load their own risk. Dealers were saddled with some exposures, mostly in loans the back-end of the last calendar year, where fairly well known companies came to market but found little interest and the dealers ended up taking down the risk themselves. With the market back open, they have taken the opportunity to launch new bond deals or tap existing outstanding deals to use the proceeds to pay down the loans and take the risk off their balance sheets.

Noted asset sector target or bias this month includes:

- With the next big securitization conference on the horizon and a new calendar year, ABS issuance has resumed in full force. With dozens of new deals in the market and being launched, it has helped bring in spreads on ABS, helping the sector be an early over-performer. We consider ABS to be a sector that has still untapped value and even with a sharp rally, several legs to keep going. We continue to be positive on auto ABS but do detect some weakness in newer deals and feel as if enhancement levels will be tested a little more than legacy deals, especially when one considers the drop in used car prices and the impact of what that might mean on those deals. We have moved FFELP student loan ABS to an avoid sub-sector, preferring to steer clear of the political debates surrounding those deals. We also have whole business securitization sub-sector on avoid, as the esoteric nature of them comes with questionable liquidity profiles. We do, however, have a positive bias for container and rail deals, which tend to get overlooked in times like this and can provide solid yield at higher levels of the credit stack.

- Commercial real estate is still in the news. Negative headlines continue to plague the sector with large announced layoffs at a number of firms highlighting the lessening demand for office space. Additionally, high profile, and large private funds specializing in commercial real estate, managed by the bigger names in the market such as Blackstone and KKR continue to be in the news as they drop the gate on how much redemptions the large funds will allow on a quarterly basis. While those funds are operating as they should, and as allowed under fund documents, the headlines generated do not help the overall sector and we are seeing a ripple from that affecting other areas of commercial real estate such as CMBS. Not a new story, but one that is once again pushing the sector into avoid as we do not anticipate any upside performance possibilities in the short or near term.

- Corporate continues to be a positive sector for us. Sub-sectors such as auto related manufacturers are more neutral, due to sales data and some concern on consumer health. Technology was battered into the end of last year and spreads make it an attractive sub-sector to consider adding risk to. Other sectors of interest include insurance, packaging and air lessors. Air lessors continue to show strength and with aircraft valuations climbing and air traffic demand increasing, should be able to increase lease rates and improve margins and overall credit strength. With the pandemic not fully in the rear view mirror, levels are attractive in that specific sub-sector.

- We maintain a relatively positive outlook on agency MBS. The current coupon MBS spread over Treasuries has tightened 50 bps since mid-October and Treasuries have rallied, but the sector still offers value in a time when corporate credit spreads grapple with potential recession risk. MBS spreads are still attractive and paper that was trading at a premium not long ago can still be acquired at discounts. There are risks that technical factors, such as Fed demand and bank demand, may remain as headwinds to MBS performance. At the same time, lower rate volatility should help nominal spreads. Meanwhile, we see value in multiple segments of the market, and have recently focused on pools with profiles that won’t extend too much if refinance incentives remain stagnant or the housing market slumps. Examples of recent purchases are investor property collateral pools and shorter duration pools composed of the less traditional 10-year mortgages.

- Banks overall continue to be attractive. This is especially true in yankee banks. The overall health of the banking sector remains strong and with higher mortgage rates, ability to increase margins is available. Trading desks continue to exhibit strength, helping the overall health of those banks that feature those internal corporate revenue diversification areas. Issuance remains strong and liquidity is ample in the sector. With heavy issuance, spreads continue to be available for some yield pick-up against similar rated corporate credits.

- Hybrids have moved steadily into a positive sector for us. The sector has rallied over the past month, and the legacy paper in certain cases has the added benefit of moving out of fixed into floating paper with lagging coupons. Bank paper remains popular in the sector, which we find attractive at current levels. Given regulatory demands, most of that paper should be called in shorter time horizons than final maturities would indicate, making them attractive for duration reasons. Corporate perps have additional value, given their name diversification but come with a structure that makes it unlikely they will be called in a similar fashion to bank paper. We find certain corporate names attractive at current yields.

Positioning & Outlook

At the end of last year, we were using our cash hoard to selectively target specific issuers and maturities in anticipation of finding value and opportunities. With a new calendar and a sudden rush to invest, we have continued to be selective and patient, preferring to let some of this excessive demand play out before entering the market too quickly and having it turn in a negative fashion later. We continue to feel there are selective opportunities in the market and remain patient in targeting and executing at the right level to lay a foundation for potential near-term over performance.

Rates continue to be a concern, but the fear of the Fed has slowly dissipated. There is still no real answer as to when the Fed will stop, but the market seems relaxed in their thinking that whatever hikes are still coming, they will be few and small. This goes hand in hand with the new issue market opening as it has the first month of the new year, as most participants feel some assurance that rates won’t overpower the performance of those credits coming to market, turning today’s issuance into tomorrow’s discounts. Rates are still exhibiting a 5.0% or so terminal rate. The first few days have been slightly under that, but it won’t take much of a rate sell-off to push it closer to that level. Nevertheless, most are comfortable operating there as they at least feel rates seem fairly range-bound at this point.

The overall mood in the fixed income market is a positive one. There is a feeling of ease with where rates are and most feel as if they have a good grasp on the direction or range of rates. With increased levels of trading, secondary and primary activity highlight the strong liquidity to be found in the market. We continue to prefer to move up in credit given the additional spread and yield available, and do feel on a daily basis some opportunities will be available if supportive patience is utilized. We prefer the shorter end of the yield curve, given how elevated rates are on the 1-3 year area of the curve. We would expect duration to remain near current levels over the near term.

Learn more about the Yorktown Multi-Sector Bond Fund:

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage - Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

You should carefully consider the investment objectives, potential risks, management fees, charges and expenses of the fund before investing. The fund's prospectus contains this and other information about the fund and should be read carefully before investing. You may obtain a current copy of the fund's prospectus by calling 1-800-544-6060.

Per the most recent prospectus, the operating expense ratios for the Yorktown Multi-Sector Bond Fund are as follows: Class A, 1.11%; Class L, 1.61%; Class C, 1.61%; Institutional Class, 0.61%. The Fund does not use fee waivers at this time.

Fixed income investments are affected by a number of risks, including fluctuation in interest rates, credit risk, and prepayment risk. In general, as prevailing interest rates rise, fixed income securities prices will fall.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. There is no guarantee that this, or any, investing strategy will succeed.

Diversification does not ensure a profit or guarantee against loss.

There is no affiliation between Ultimus Fund Distributors, LLC and the other firms referenced in this material.

Control #: 16437154-UFD-2/14/2023