Macro Update

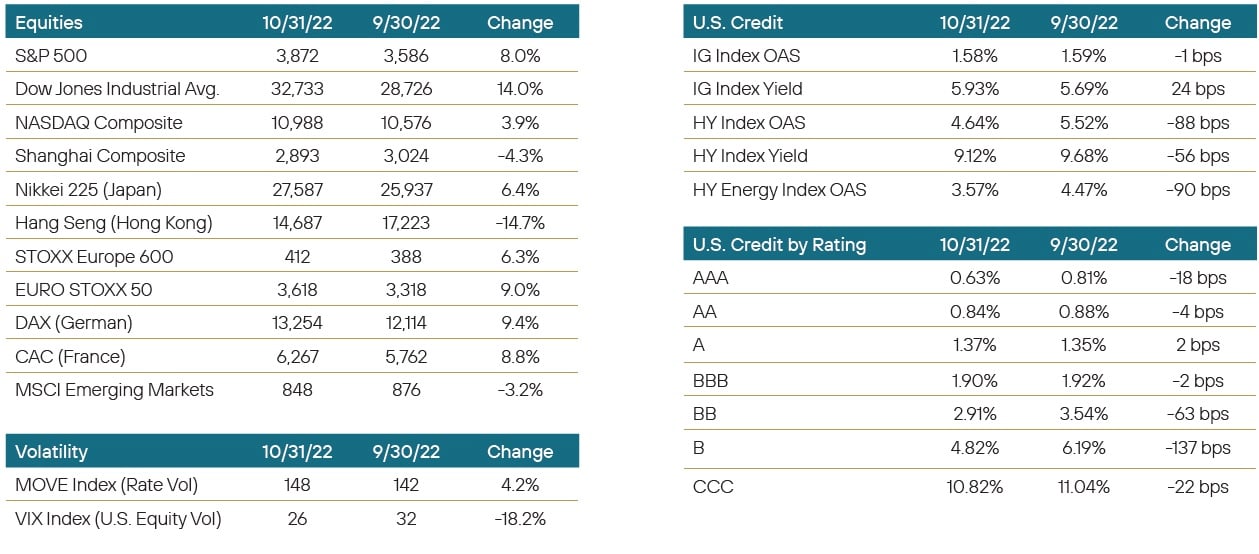

October was a strong risk-on month that saw large gains in equity markets along with spread tightening for high yield bonds. Meanwhile, higher quality corporate debt was mostly unchanged on a spread basis while ABS widened out. Treasury rates were volatile, ultimately ending higher following several moves in both directions. The 30Y UST sold off 39 bps after previously lagging the short end of the curve on a consistent basis. As far as short rates went, 3-month LIBOR moved higher by 71 bps. Crude oil was ~9% higher with global energy shortage concerns emerging.

Markets spent the month deciding whether the Fed is likely to slow its aggressive tightening. When a reasonably strong non-farm payrolls report hit the tape in early October, stocks and bonds sold off, under the premise that the Fed would have no room to pivot. A week later, the anticipated monthly CPI report showed an inflation figure above expectations (0.6% month over month and a headline 8.2% year over year). Services inflation was up and markets sold off, with rate futures traders pricing in an additional hike and a terminal Fed Funds rate slightly north of 5%.

The first half of the month felt like the familiar chorus of the past twelve months. Then the tone changed quickly in a significant way. A mix of bad but not-too-bad news began to convince investors that the Fed could slow its pace of rate hikes. This came in the form of slowing housing and rental markets (contradicting the recent lagging inflation data), a few occasional corporate earnings disappointments (despite solid overall earnings beats), and some prominent investors forecasting recession. In short, these were taken as potential indicators of slowing inflation. On the other side of the coin, bank earnings surprised to the upside and consumer spending remained robust, suggesting that recession could be mild. Markets rallied on speculation of a slowing Fed, regardless of the firm expectation for 75 bps at the early November meeting. However, the biggest catalyst for a rally came towards the end of the month when San Francisco Fed President Mary Daly said that future hikes could come in smaller sizes. The belief that debate exists among Fed officials about slowing its pace after the November meeting unleashed euphoria in the risk markets, generating exceptional overall monthly returns for securities in the riskier parts of the capital structure. With a strong finish in late October, the Dow Jones enjoyed its best month in decades.

Portfolio Review

October was another data driven month, with a confusing, contentious inflation print. It’s all about the data, and yet the data seemed to be series of reports that market participants argued over with regards to accuracy, timeliness, and pertinence. The CPI report exceeded expectations, resulting in spiking treasury yields. But over time notable market names began to question in the relevance, sourcing, and timeliness of one of the biggest inputs: rent, which was responsible for a great deal of the number surprising on the high end. There is an uneasiness in coming to grips with the idea that the Fed uses this number for its outlook and yet, not truly embracing the number. Similarly, the JOLTs report fell under similar scrutiny. The result of this is that there is an underlying theme in the markets that technology, and data gathering methods are not producing relevant data to be relied upon. As a result, there is an uneasy truce that the market itself does not trust the numbers but understands that is what will drive Fed decisions. Strange days indeed.

Noted asset sector target or bias this month includes:

- The asset-backed securities (ABS) industry held its annual fall conference in October, and typically after that there are a preponderance of issuance and activity. This year there were less offerings in the primary market post-conference and those deals widened out in terms of spreads. Of late there has been less interest in the lower end of the credit stack, as those anticipating a slowing economy are concerned that we will be witness to a spike in serious delinquencies and ultimately defaults. As a result, and similar to the last few months, we continue to find seasoned ABS more attractive. The older vintage deals provide solid historical performance that can be tracked, most of the weaker borrowers have fallen out of the deal by this point in its life cycle, and those deals have built strong credit enhancement providing some cushion should performance waver slightly. Auto ABS continues to be highly liquid and a strong preference as a target, due to the factors mentioned above. Equipment leasing and credit cards, two of the older ABS types, with long track records have additionally cheapened enough to make them attractive as well. Performing seasoned deals tend to get upgraded over time, which we believe may lead to spread compression and near-term over-performance, even in a widening spread environment such as this.

- Leveraged loans continue to garner headlines with the latest largest new issuance deal for Twitter in the news. Once again it appears the banks who brought the deal might have to hold onto it rather than syndicate it, as articles describe a tired investor base. Worse, the secondary investor base such as CLOs are seemingly full to technology industry deals. This is pushing the loans onto the banks’ balance sheets, with some acknowledging a potential loss due to shift in market conditions. On the initial run-up of rates, loans were a popular investment avenue as a means to get floating rate risk in the portfolio, but as expected that has dissipated and now over supply hangs over the industry. We previously moved CLOs to a neutral holding. We continue to prefer older vintage deals that are close to deleveraging and paying down, with the spread widening causing deals to be trading at a discounted dollar price, allowing for strong pickup in terms of over-performance as those deals pay down. Deals with top tier managers, out of their reinvestment periods, at the senior level of the capital stack, remain attractive and offer potentially solid performance going forward.

- Banks continue to exhibit strong earnings and underlying value. Since the Financial Crisis, liquidity and capital ratios have been maintained at much higher levels. Currently there is an underlying theme of banks increasing reserves to account for what is expected to be higher loan losses. Prudent management is evident across the board. We have found value in Yankee banks in the past, but now with spread widening across the landscape, more expensive names are comparatively cheap and represent strong value moving forward. Similar to our focus in corporates (see below), one doesn’t have to reach to find strong value in well known liquid names, presenting the opportunity to lock in attractive yields and value that we believe may translate into over-performance in the near term.

- We remain slightly constructive on Agency MBS. Nominal spreads have tightened a bit lately but still remain a few deviations from their historical norms, currently sitting at their 2+ year wides. While volatility has ticked down and reduced the short-option cost in MBS pricing models, this is not yet a stable trend, and there is a dearth of traditional bank buyers for the product right now. We prefer newer issue, higher coupon pools that minimize price volatility risk, but we also see high duration, high discount pools with prepay upside as having attractive total return profiles at this time.

- Treasuries have become solid targets as well. Attractive yields are available in the short end of the curve, combining with what we feel as offering solid value further out in longer duration notes. Currently we feel in the short end of the curve, 2 to 3 year notes which have rolled down the curve at heavy discounts are favorable, with additional interest in 20 year notes when looking further out the curve.

- Value is widely available in highly liquid investment grade corporates. We continue to focus on the sector to take advantage of value with liquidity and diversification benefits. Spreads in high profile, highly liquid names have widened to historically wide levels. Targets in rail, utility, technology and big box retail focused on home improvement offer future over-performance opportunities. Targeted maturity areas are typically 2 to 3 year paper, and in heavily discounted paper.

Positioning & Outlook

The end of the year and holidays are fast approaching. The Fed has two more meetings before year-end and the market is anticipating a 75bps hike in November and a potential 50 bps hike in December. Nothing has changed with that in mind. The only thing still on everyone’s mind is if there will be a pause to figure out where we are and how effective were the previous hikes. For those who moved aggressively over the past six months, trying to anticipate, or bet on a rate slowdown, those parties were hurt by the upward trajectory of rates. Whether it was issuers trying to guess on the best day to enter the market, or investors assuming they would be getting new issue at top of the rate expectations, thus far, all have seen those ideas swallowed up by rate expectations and data prints. The end of the rate hikes is coming. We have long entered the area of where the Fed has indicated the final spot would be and there are but one or maybe two hikes left to accomplish with the market already pricing those in. We have moved cautiously in this environment, preferring to hoard cash and dry powder. There has been no reason to be aggressive and no reward for being early thus far. We continue to approach this market in a cautious manner, however, this month we see room for some optimism and potential of locking in solid values as we come out the other side of the rate hike aggressiveness.

The market has seemingly capitulated with the Fed. Fear of the fed has caused many investors to take a step back; however, with the Fed’s rate hiking nearing its end, we expect issuance and trading levels to start to increase as those first movers take advantage of specific targets such as the ones mentioned above. We continue to move cautiously, taking advantage of a targeted issuance and preferring highly liquid and high credit quality at wider spreads names. We expect 75 bps in November with a follow-up in December of 50 bps. Maturities remain on the shorter side, but we like the 3 year corporate tenor in terms of value. We would expect duration to remain near current levels over the near term.

Learn more about the Yorktown Short Term Bond Fund:

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Disclosures

You should carefully consider the investment objectives, potential risks, management fees, charges and expenses of the fund before investing. The fund's prospectus contains this and other information about the fund and should be read carefully before investing. You may obtain a current copy of the fund's prospectus by calling 800-544-6060.

Per the most current prospectus, (1) Fund total operating expense ratios are: Class A, 0.87%; Class L, 1.52%; Institutional Class, 0.87% until at least May 31, 2023. (2) In addition, the Adviser has entered into contractual expense limitation agreement with the Trust so that the Fund’s ratio of total annual operating expenses are limited to 0.84% for Class A shares and Institutional Class shares and 1.49% for Class L Shares until at least May 31, 2023.

Fixed income investments are affected by a number of risks, including fluctuation in interest rates, credit risk, and prepayment risk. In general, as prevailing interest rates rise, fixed income securities prices will fall.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. There is no guarantee that this, or any, investing strategy will succeed.

Diversification does not ensure a profit or guarantee against loss.

There is no affiliation between Ultimus Fund Distributors, LLC and the other firms referenced in this material.

15622192-UFD-9/13/2022