Macroeconomic Update

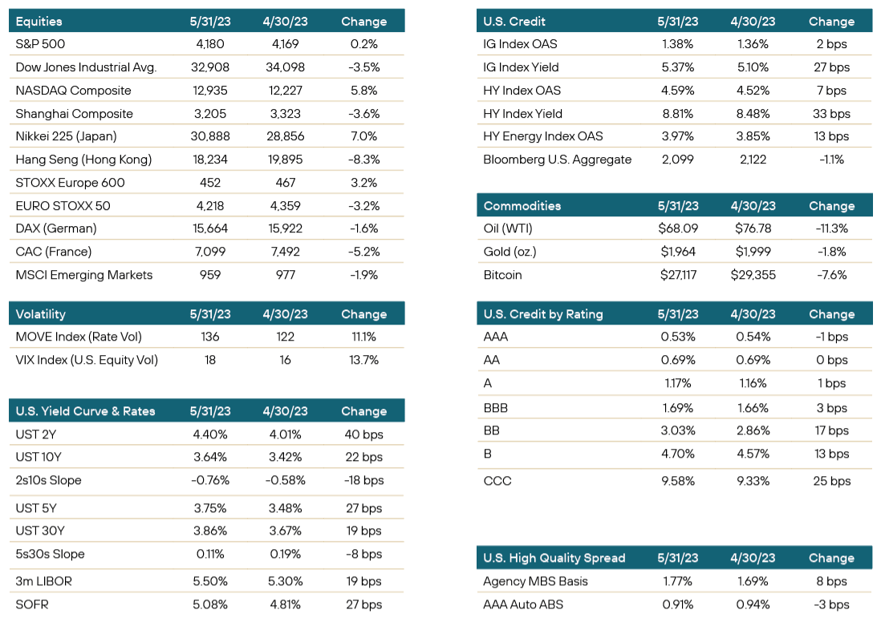

On net, May brought a risk-off move across most asset classes and the course was uneven. Treasury rates initially rallied with JOLTS data showing a slowing U.S. jobs market. In particular, job openings fell to a two-year low as layoffs showed signs of increasing. Nonetheless, within a few hours, focus turned back to the debt ceiling, the next day’s conclusion of the Fed meeting, and renewed concerns about regional bank stability. As expected, the Fed raised by 25 bps, placing the funds rate above 5% for the first time since before the financial crisis. While investors mostly interpreted the Fed statement and press conference to be communicative of a semi-hawkish pause, some felt the messaging was less hawkish than expected. Within the statement, prior language about anticipating that more firming may be needed was removed and replaced with an intention to “determine whether additional tightening is appropriate.” Chair Powell also repeated his belief that “the U.S. banking system is sound and resilient.” Two days later we once again received a Nonfarm Payrolls report that was stronger than expected. April unemployment had fallen from 3.5% to 3.4%, reinforcing the Fed’s predicament. It needs to weigh its inflation fight against ongoing bank stress, with a best case perhaps being that credit tightening arising from banking issues is well in progress.

The much awaited CPI report came in within expectations on May 10th. The inflation print seemed to provide the Fed with its hoped-for opportunity to pause. The core services ex shelter component was nicely up just 0.1% which is below the Fed’s goal. Following CPI, a day later the Producer Price Index (PPI) came in soft. But after PPI, with a short break between major data releases, investors turned to Fed speakers for economic updates and were not comforted. Most notably, Michelle Bowman and Raphael Bostic made remarks about the length of time the funds rate will need to be held in restrictive territory, which remain at odds with the bond market’s expectations for late 2023 / early 2024 rate cuts. Powell was a touch more dovish when he said the FOMC has made a lot of progress and the risks of acting more versus not acting have become more balanced, but nonetheless, long term inflation expectations ticked up. And unfortunately, on the 26th, a faster than expected Personal Consumption Expenditures (PCE) deflator (0.4% for April) release raised the June/July rate hike probabilities.

On the positive side, and to great relief, the debt ceiling standoff seemed resolved by the evening of the 31st as the House voted on and passed the debt ceiling bill. Treasuries had rallied during the holiday-shortened final week of May on these hopes, but all told, UST 2Y sold off 40 bps month over month and UST 10Y was 22 bps worse, comprising a painful, 18 bps bear flattening of the yield curve. Both rate and equity volatility increased by more than 10% and both IG (+2 bps) and HY (+7 bps) corporate credit widened, as did agency MBS (+8 bps). Global equities and crude oil (-11.3%) were hit fairly hard, while the bright spots were the extreme moves by NASDAQ tech stocks (+5.8%) and Japan’s Nikkei 225 (+7.0%).

Portfolio Review

A predominant focus in May was strategies built around risk-off. With the majority of the bank angst behind us, there was still an air of worry in the air, with most unsure if the actual all-clear bell had been rung or not. Overall, however, liquidity remained strong in the market and bids were prevalent, as those with cash and shopping lists took advantage of the environment. Those who still were in sell mode had to expect to give some on the offer if they wanted to move on. Nevertheless, the markets seemed to move more towards a smoother feel overall. That doesn’t mean rates don’t continue to wreak havoc with a market and the Fed seemingly eager for data points confirming a pause in rate hikes. The latest data didn’t cooperate as much as most wanted, but we seem to have turned a corner where data is now being parsed down to those data points that seem to be at least moving in the right direction of a pause. Certainly headlines and market chatter seem to have moved to viewpoint.

Noted asset sector target or bias this month includes:

- Agency MBS continued to widen with the basis finishing out 8 bps month over month. As written here last month, spreads sit at long-term wides that approach levels from March of 2020 and October of 2022. We continue to view this as a buying opportunity, due to both the historic nature of wide spreads and the current levels of market interest rates. The MBS market certainly has its share of headwinds, from diminishing bank demand and reduced Collateralized Mortgage Obligation (CMO) production, to vanishing Fed demand and FDIC bank liquidations. But despite all of this, higher coupon securities at attractive valuations offer sufficient carry to weather the intermediate term volatility. It’s a good time to focus on yield pickup. We like low payup conventionals and slightly seasoned discounts. We also believe payups in 20Y product have room to appreciate and offer relative return.

- Perpetuals/hybrids/preferreds are attractive on an overall basis with a stronger preference for large global, but domestic-based, names. The too big to fail banks have been battered as part of a sector avoidance by most investors, being dragged down by lesser, smaller names. At current levels, with relatively short duration for most, they have reached a level that can provide solid near-term over-performance. The larger global, Yankee banks, also provide some significant attractiveness at current spreads. However, given that a majority of those opportunities are in contingent convertible or contingent capital type securities, one must be vigilant from a credit standpoint. Nevertheless, in the bigger, stronger, more stable names, value can be found as well. Smaller regional bank preferreds continue to rebound, but the market remains eager to punish those names that show the slightest cracks and therefore, we continue to consider them from a neutral standpoint, preferring to look towards the larger banks for better value.

- Corporates overall remain a targeted sector. We continue to expect some slowing in the economy, and therefore target more defensive sectors within investment grade. We remain constructive on our previous targeted sectors, including discount eateries, discount retailers, rail, packaging, utilities, and lodging. We do expect spread widening as the environment weakens and as such prefer investment grade to high yield. Staying in more liquid, higher quality corporates is a current thesis.

- Private credit remains neutral target for us, with an avoid for things such as BDCs. With a slow down in economic activity expected and spread widening to follow, regardless of the health of the issuer, single B and CCC credits should see the biggest gapping in spreads. In addition, we would expect a rising of downgrades and an increasing number of bankruptcies at that level of credit in the next cycle. As such, borrowers at that level of the credit stack are sure to be the more vulnerable. For overall credit risk at this level, CLO exposure seems preferable. We have CLOs at a more neutral level of interest. However, seasoned paper, out of its reinvestment period, and higher in the credit stack, at senior levels, would be where more value can be found.

Positioning & Outlook

The current economic environment remains resilient as jobs data continues to show strength. However, our concern that we are entering a slowing period has us vigilant on where we are in the calendar and cycle. Furthermore, given our expectation of a downshift in the economy, we continue to focus on credit, liquidity and diversification as a means to mitigate whatever shift we might witness. A fourth quarter rate cut does seem like it might occur, and as such we do expect rates to rally towards the end of the summer. We remain committed to sticking to higher credit quality while targeting specific issuers and sectors to help lay a foundation for future over-performance. The front-end of the curve remains the most opportunistic area for investment targets, and we still feel we find most value in the 1-3 year area of the curve. Duration remains at or near most recent levels and we expect it to stay in the area for the near-term.

The primary market continues to exhibit strength. New issuance has been robust. Of some importance is the return of regional banks to the new issuance market, with both PNC, Jefferies and Truist coming to market and seeing solid demand. This further bolsters confidence in the market with financials, leading to spreads to tighten across the sector. Additionally there was demand for global bank paper, where a number of issuers used the primary market over the month to meet funding needs. Investment grade credit experienced equally strong demand. However, high yield issuance continues to be sporadic with only the stronger names like Ford finding sufficient demand in this risk-off mode market.

With the Fed raising early in May, there continues to be a sense the Fed and the market want to at least pause. That said, there is some push for a potential rate hike still to come in July, but with concurrent expectations that the Fed would potentially then be faced with a rate cut by year-end. An interesting contrast on what the market expects over a relatively short period of time.

This is a market that is rewarding patience and keeping on the path of more liquid bonds. As a result, we continue to focus on risk that is higher up in the capital structure as well as more recent issuance in liquid sizes. Given the credit and rate environment, having dry powder to execute when opportunity arises will potentially lead to over-performance down the road. We remain patient and offer liquidity when we see targeted opportunities present themselves.

Learn more about the Yorktown Multi-Sector Bond Fund:

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage - Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

You should carefully consider the investment objectives, potential risks, management fees, charges and expenses of the fund before investing. The fund's prospectus contains this and other information about the fund and should be read carefully before investing. You may obtain a current copy of the fund's prospectus by calling 1-800-544-6060.

Per the most recent prospectus, the operating expense ratios for the Yorktown Multi-Sector Bond Fund are as follows: Class A, 1.17%; Class L, 1.67%; Class C, 1.67%; Institutional Class, 0.67%. The Fund does not use fee waivers at this time.

Fixed income investments are affected by a number of risks, including fluctuation in interest rates, credit risk, and prepayment risk. In general, as prevailing interest rates rise, fixed income securities prices will fall.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. There is no guarantee that this, or any, investing strategy will succeed.

Diversification does not ensure a profit or guarantee against loss.

There is no affiliation between Ultimus Fund Distributors, LLC and the other firms referenced in this material.

Control #: 17014922-UFD-6/14/2023