Macroeconomic Update

April was a much calmer month than its recent predecessors. Volatility subsided as fears significantly eased from March’s banking scare. Equities, Treasuries and credit spreads all enjoyed this stability and produced positive returns. Concern over First Republic Bank notwithstanding, investors were able to instead return a bulk of attention to high level economic data, as they now ask whether March’s troubles will generate credit market tightening and therefore actually aid the Fed in its inflation fight.

The economy showed signs of downshifting from the data releases in the first half of April, reinforcing a baseline expectation of a 25 bps hike in May followed by a June pause. Loretta Mester of the Cleveland Fed had set an early hawkish tone for the month, commenting that the Fed has its own view, differing from the market, with respect to a 5%+ terminal rate and the potential need to hold the rate higher for longer. (Traders nonetheless continued to price in 4+ cuts by early 2024.) But the data following Mester suggested the numbers may finally be starting to cooperate with the central bank’s intent to slow the economy. The ADP payrolls data was soft, in addition to the U.S. service sector rate of expansion. Nonfarm payrolls arrived mostly in line with forecasts, but the CPI report on April 12th hinted that the disinflationary process may have legs. Overall and core inflation were each on the lower end of expectations, and the market showed its relief in avoiding an upside surprise. That same day, the Fed minutes were released, which included a forecast for a mild recession later this year. All of this information added up to support the belief that some additional policy firming will be warranted, but that a pause could likely be around the corner following the Fed meeting in early May. Rates markets were choppy but felt under control.

Some of the later month data, such as the Personal Consumption Expenditures (PCE) deflator, were a little less cooperative, although GDP came in softer. Some encouraging numbers aside, inflation has simply not fallen as fast as hoped and the economy has remained resilient from trillions in pandemic stimulus. Smaller businesses have felt the tighter conditions in credit but this has not flowed through to the consumer, as demand is still strong and job growth persists. The upcoming economic data for May data should shed light as it will capture more of the credit impact of the banking scare in March.

Portfolio Review

April continued to be a bumpy ride for the market. Almost daily there seemed to be rumors of another bank on the cusp of failure or some desire from a certain minority to see the whole banking system in flames. As time went on, we seemed to be more in-line with a less lethal, junior version of the Great Financial Crisis (GFC), with smaller and smaller banks in the sightlines and less of a worry for the larger global banks. In a slight twist over the previous iterations however, it did seem the Fed was perfectly happy to see shareholders and certain level of creditors take the brunt of the hit, just as long as depositors were made whole. That is quite a different theme than was witnessed during GFC, and certainly was picked up by market participants. In the end, there was still, however, a reliance on larger banks to step up and when the next in line, First Republic, JP Morgan was able to swallow it up without blinking. What this ultimately tells us that it is a slightly different playing field than in 2008, deal terms are different, and the bigger global banks seemed to be capitalized well enough to not only attract depositors of smaller banks but also healthy enough to grow by adding those troubled banks at discount prices courtesy of the Fed.

Noted asset sector target or bias this month includes:

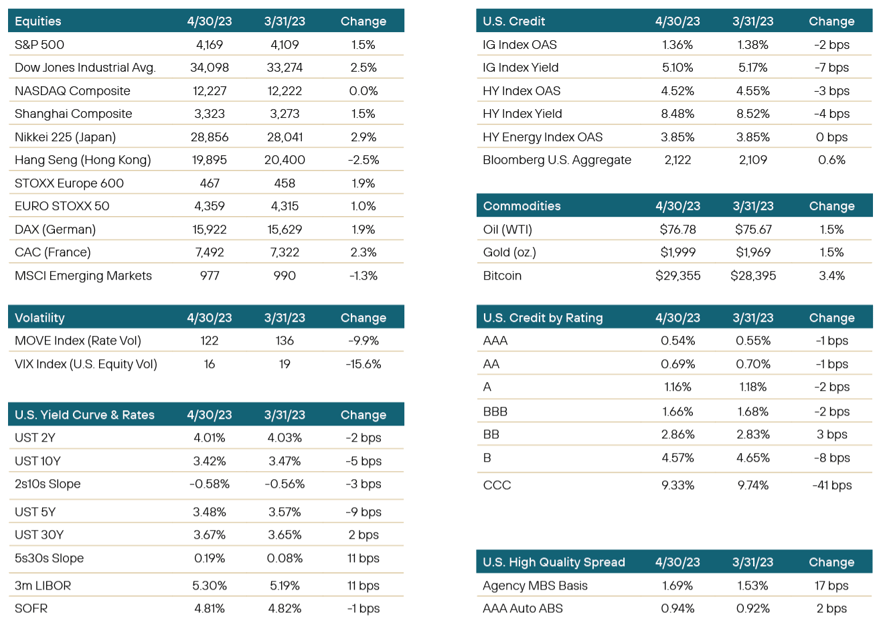

- Mortgages were an under-performer in April as bank buying of MBS remained muted. With the aforementioned lack of regular demand from banks, along with Silicon Valley Bank’s MBS holdings being liquidated, spreads across MBS products widened a good bit. The mortgage basis, reflecting the spread offered by 30Y current coupon MBS over a blend of 5Y and 10Y Treasuries, finished wider by 17 bps, finishing the month at 1.69%. The basis currently sits at a level approaching where bonds traded in March of 2020 and October of 2022. We continue to view this as a buying opportunity, due to both the historic nature of wide spreads and the current levels of market interest rates. Because bank demand is not yet ready to return, we expect further volatility, and therefore prefer higher coupon pools that offer enough current carry to withstand some ongoing volatility in MBS prices. Given our bias towards lower duration (as evidenced by the preference for high coupons), we’ve also been focused on some pools in the 15Y sectors that can be acquired at cheap valuations and which pay down faster than traditional 30Y product cohorts.

- Community banks are an avoid. The headlines of current issues at smaller banks and the shadow of SVB remain an unwelcome hangover. However, beyond the noise of those issues remains a concern about what the future holds for banks of this size. Their loan books are historically heavily weighted towards commercial lending, and with commercial real estate continuing to have issues and more and more defaults seemingly the norm, defaults by large well-known property investors, the future seems to be filled with hazard. We would expect even those small banks that survive the current market and keep deposits intact, that some of them still face a reckoning when it comes to their loan book.

- Corporates remain a preferred target sector overall, but with a bias and preference for defensive sectors and those investment-grade targets a positive bias for us. We continue to consider discount eateries, discount retailers, rail, packaging and utilities to be the more coveted sub-sectors within corporates. With the recent good news in terms of bookings for cruise lines and airlines being released, we tend to take a step-back with those sectors, with a concern that future economic slowdown may mean we have seen a peak in their future bookings. As such, discretionary spending remains more of a neutral target within the corporate space. Overall we continue to prefer investment grade over high yield, as we expect a slowing economy to push credit spreads wider the further one goes down in the credit stack.

- CLOs have moved to a more neutral target for us. We continue to prefer seasoned paper over new issue, whatever has been issued as that market has seen almost a complete shutdown. Seasoned paper out of the reinvestment period for the vintage issuance reduces manager risk and leads to less extension risk, with deleveraging more likely. This allows for historical performance and a look at older loans most likely launched under more restrictive reps and warranties the majority of the portfolio. With less new issuance available, it also means spread should remain fairly range-bound with less new issue available to distract investors, forcing them also to consider secondary offerings and hopefully keeping spreads tighter. Liquidity is still adequate at the more senior trances, which we prefer given our outlook for a slower economy and thus potentially an uptick in delinquencies and defaults at the lower end of the loan spectrum.

- Perpetuals/hybrids/preferred continue to be batted around by the market, and have now been punished enough that we would consider them buying opportunities at those levels on an overall basis. Actual transactions continue however to be a case-by-case analysis. Within the bucket we would avoid the smaller community banks and regionals who are still at the mercy of future headlines and seem to be targets of the vultures in the market. However, bigger global banks have also seen their perpetuals get hit by pricing and represent potential over performance opportunities as their balance sheets, overall size, and diversified funding and asset mixes make them equipped to succeed in this market. Nevertheless, with spreads volatile in the space, we continue to use patience to wait for the sector to settle more and consider the sector a more neutral outlook, but remain opportunistic for favored names if pricing is there.

Positioning & Outlook

There has been a pick-up in new issuance, but overall issuance remains subdued. Between the credit concerns overall in the marketplace, some concern over new economic data points, and the pressure on rates, it has been tough for corporates to find a safe jumping off point. Those deals that have gotten done are quickly at the mercy of the market turbulence, keeping most investors on the sidelines. There seems to be more wait and see in the market than previously seen. And with that type of attitude, while liquidity is adequate, there is a sense that those looking to sell are doing so at weakness and bids are reflective of that assumption. As such, we consider to see perhaps less forced sellers but more sellers in troubled or dinged up sectors, rather than strategic desire to shift targets or prune previous positions and move into more desirable sectors. If one truly wants to pay-up to do these types of portfolio shifts, there is an ability to do so, but it can be costly.

The Fed seems to be slowing. With the market on edge, concerned about the banking sector, rational or irrational, what the Fed does sends seemingly a message. As such, a departure from their path, despite expectations that the banking issues are already doing some of the Fed’s work by taking liquidity and easy credit out of the market, still needs to follow some of the script or perhaps falsely giving the impression there is more to worry about. As such expectations were that the Fed would raise rates at the beginning of May, and all signs were and ultimately proved to be correct. They followed the script, and while perhaps the last 25 bps wasn’t necessary, it did take the question of the Fed knowing more than they were letting on out of the equation. As such, the market got the pre-determined rate hike and quelled some of the fear that the Fed was far more concerned about the banking sector than they had let on.

We continue to see too many headlines involving concerns about local and regional banks. Current economic data however continues to show a fairly strong economy and healthy job market, leading to rate pressures still influencing pricing. As such, there is daily concern about credit but at the same time rate pressures. A confusing time in the market for most participants. We continue to use the environment to strengthen credit and focus on increasing the diversification and liquidity within the portfolio. It is the time to be picky and consistent when looking for targets. Patience is important. We do expect the Fed to cease hiking and as such, with the help of slower economic activity, expect we may see rate rallies come the second half of the year. We remain committed to sticking to higher credit quality while targeting specific issuers and sectors to help lay a foundation for potential future over-performance. The front-end of the curve remains the most opportunistic area for investment targets, and we still feel we find most value in the 1-3 year area of the curve. Duration remains at or near most recent levels and we expect it to stay in the area for the near-term.

We continue to be patient and take what the market will give us. These types of volatile days provide opportunities to buy targeted situations such as sectors and issuers we have shown an interest in adding into. Patience continues to be the best action. Targets include those issuers, sectors and maturities we feel will help reach optimum weightings that ultimately may lead to near-term over-performance.

Learn more about the Yorktown Multi-Sector Bond Fund:

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage - Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

You should carefully consider the investment objectives, potential risks, management fees, charges and expenses of the fund before investing. The fund's prospectus contains this and other information about the fund and should be read carefully before investing. You may obtain a current copy of the fund's prospectus by calling 1-800-544-6060.

Per the most recent prospectus, the operating expense ratios for the Yorktown Multi-Sector Bond Fund are as follows: Class A, 1.11%; Class L, 1.61%; Class C, 1.61%; Institutional Class, 0.61%. The Fund does not use fee waivers at this time.

Fixed income investments are affected by a number of risks, including fluctuation in interest rates, credit risk, and prepayment risk. In general, as prevailing interest rates rise, fixed income securities prices will fall.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. There is no guarantee that this, or any, investing strategy will succeed.

Diversification does not ensure a profit or guarantee against loss.

There is no affiliation between Ultimus Fund Distributors, LLC and the other firms referenced in this material.

Control #: 16879468-UFD-5/15/2023