Macro Update

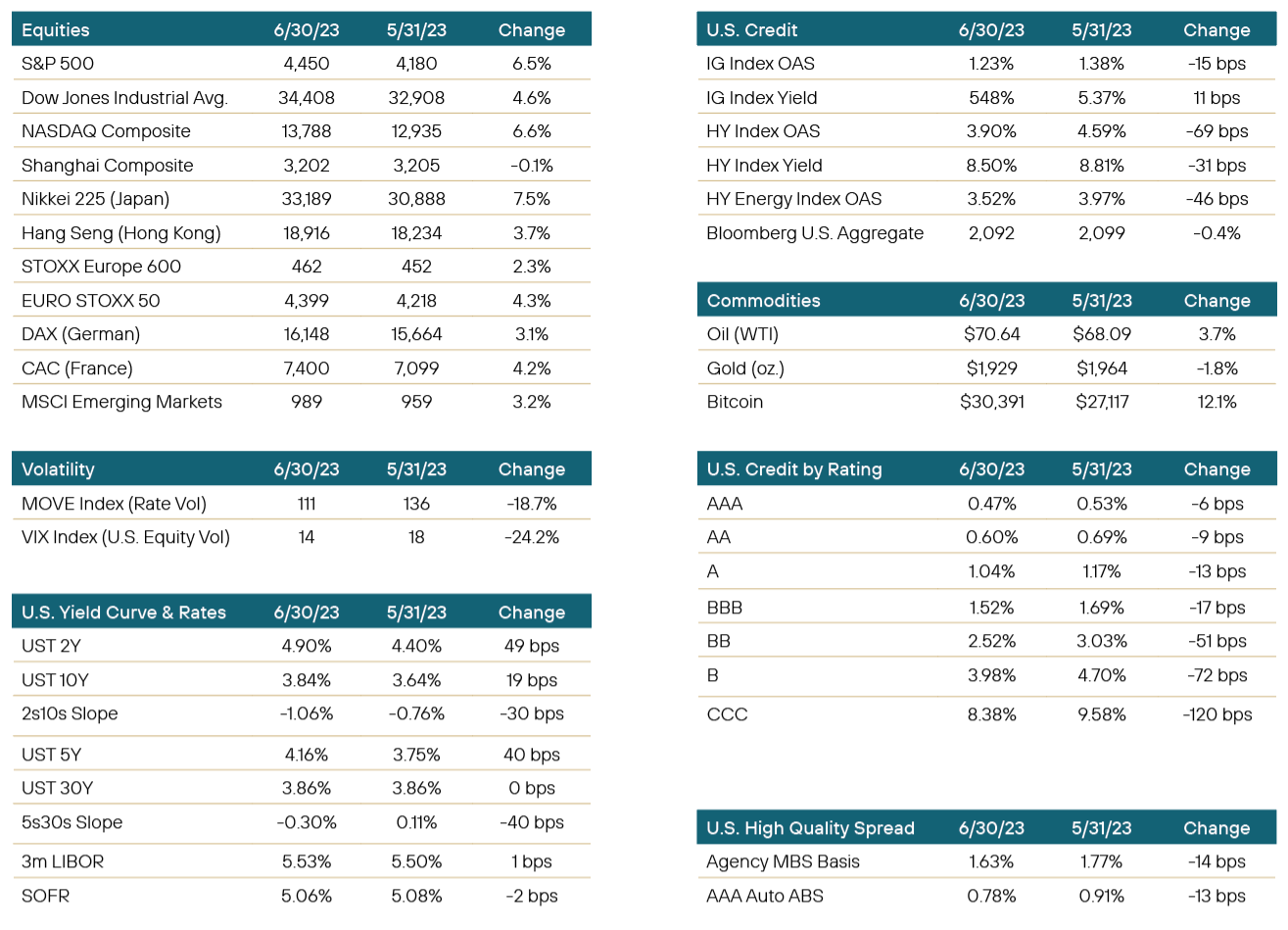

June was a risk-on month as investors began to accept that while the economy is slowing, it is taking its time in doing so. The month’s economic data was too mixed, in aggregate, to alleviate concern over the progress of the Fed’s inflation fight. Case in point: nonfarm payrolls came in hot, but the unemployment rate rose, and wage growth slowed a touch; jobless claims hit a near-two-year high followed by later dropping the most (and in a holiday week) since 2021; Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) cooled and consumer spending stagnated, yet Q1 GDP was revised to the upside. Job cuts have been in the news but are still mostly confined to tech and software.

With still too much conflicting data, the Fed paused at the June meeting while sending hawkish signals. This was the first time the Fed stood still in 11 meetings, but the statement and press conference indicated clearly that more tightening is to come, barring any major surprises. The most notable communication from the meeting was a revelation that half of the committee supports two more hikes. The market was caught off guard with a dot plot showing a 5.6% terminal rate, as Chair Powell stated that inflation risks are still tilted to the downside (i.e. persistent or entrenched inflation). Later, near month-end, while speaking, Powell signaled that the Fed is open to successive hikes at coming meetings and stated that he doesn’t expect 2% inflation until sometime in 2025.

With the economy not yet slowing as much as hoped, the month brought higher rates (a sharp bear flattening), tighter corporate credit spreads in both IG and HY, and spread compression for agency MBS and auto ABS. Rate volatility actually lessened while equities surged (especially in Asia and North America). Eyes turn to the July 26th Fed meeting with rates traders pricing in a 25 bp hike followed by a great deal of monetary policy uncertainty at the following meetings in September and November.

Portfolio Review

The overall market seemed to be in a bit of a funk for the month. Liquidity was available but bid ask remained curiously wide, and thus liquidity was punishing if one truly needed it. Rate concerns continued to be the story. The pause by the Fed was expected, but in keeping with the narrative, headlines remained firmly in the pause for pause-sake and most participants didn’t feel it was the end of the hike cycle. Indeed, attention and expectations continued to be in the camp of more rate hikes down the road. Further cementing this was a seemingly endless conga line of Fed speakers who chose to continue to hammer home that more rate hikes were necessary and coming. As a result, overall market comfort was not there, and most investors favored sitting on the sidelines versus active participation. It was a slight departure from the previous month’s environment where some optimism that we had entered a shift was occurring. It was also an important reminder that the pushing of this narrative might be more difficult to unwind when the time comes. That is, once the environment is conducive to a shift away from this rate hike cycle, there may be a lag in getting everyone on the same page in believing it. That is something to be aware of, but also something, if analyzed correctly, ripe to produce overperformance if properly approached.

From a credit standpoint, market focus was on the bank stress test results due at the end of the month. Expectations were hopeful, but there was concern that negative results of a few would impact the whole market and cause a setback on whatever recovery had occurred since the March bank selloff post-Silicon Valley Bank. Some exhaling occurred once results were released, and all 23 U.S. banks included in the stress test came through unscathed. Big banks such as JP Morgan Chase, Bank of America and Citibank performed better than regional banks and those that focused on credit cards. Credit cards did seem the hardest hit loan product, and commercial real estate loans a distant second. The bank sector continues to recover in terms of credit spreads, and we expect it will do so in the near term.

Noted asset sector target or bias this month includes:

- Agency MBS spreads remained volatile but underwent a strong net tightening into June’s rate selloff. Spreads still sit at attractive long-term wides, generated by the ongoing hole in the market from bank and Fed inactivity. Headwinds remain but higher coupon securities at attractive valuations offer sufficient carry to weather the intermediate term market volatility. As alluded to last month, it is not a bad time to be an unlevered yield buyer of agency passthroughs. We like low payup conventionals and slightly seasoned discounts. We also believe payups in 20Y product have room to appreciate and offer relative return.

- Perpetuals/hybrids/preferreds continue to be an attractive space. Tightening spreads have become a daily common occurrence in the space, especially those large globally, domestic-based banking names. However, given how far they moved in March there is still plenty of upside available and an improving liquidity profile helps make this a targeted area. Nevertheless, we remain cautious on corporate names in the space, given their reluctance to utilize the put feature that banks more commonly execute. We also remain a bit cautious about the more regional bank names which still can have some unwanted volatility on a daily basis.

- Corporates overall remain a targeted sector. We continue to expect some slowing in the economy, and therefore target more defensive sectors within investment grade. We remain constructive on our previously targeted sectors, including discount eateries, discount retailers, rail, packaging, utilities, and lodging. We do expect spread widening as the environment weakens and as such prefer investment grade to high yield. Staying in more liquid, higher quality corporates is a current thesis.

- Esoteric assets remain an avoid. Liquidity is fickle these days. As such we are avoiding issuers in corporate and structured product that would lend itself to be grouped as such. This includes whole business securitization, and sub-sector structures such as Trust Preferred Securities (TruPS), which can be found in corporate and banking sectors. With yields climbing, there isn’t any reason to reach into esoterics for any yield and there is far more downside risk in terms of illiquidity than any upside in performance available.

Positioning & Outlook

The potential of a rate hike in July has morphed into reality. With economic data pushing in that direction, and the narrative not shifting in Fed Governor speeches, we would expect another hike in the near term. However, we are seeing anecdotal evidence building of a slowing economy that just hasn’t seemed to hit the economic reports due to lags. And as such do expect near term that there is a potential that the hike cycle runs its course and there remains a slight possibility of a rate cut by year-end.

Patience and forward thinking are required. We continue to see reward for this type of positioning and focus on keeping true to that strategy. Similar to the last few months, we continue to focus on risk that is higher up in the capital structure, as well as more recent issuance in liquid sizes. Dry powder allows us to take advantage of opportunities as they present themselves and we remain focused on using it for targeted credits and more liquid sectors and issuers.

Economic data continues to support the Fed mission of rate hikes. However, as mentioned, we see headlines and anecdotal evidence of a slowing outcome that just hasn’t seem to impact government data reports. As such, we continue to position ourselves anticipating a slowing economy, but remain mindful to keep as neutral to rates as possible. The focus remains on credit, liquidity, and diversification as a means to mitigate whatever shift we might bear witness to in the third and fourth quarters. A fourth-quarter rate cut is fading, based on market expectations, but we still anticipate one to be possible. The front-end of the curve remains the most opportunistic area for investment targets, and we still feel we find most value in the 1-3 year area of the curve. Duration remains at or near the most recent levels and we expect it to stay in the area for the near-term.

Learn more about the Yorktown Short Term Bond Fund:

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage - Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

Trust Preferred Securities (TruPS) - hybrid securities issued by large banks and bank holding companies (BHCs) included in regulatory tier 1 capital and whose dividend payments were tax deductible for the issuer.

Disclosures

You should carefully consider the investment objectives, potential risks, management fees, charges and expenses of the fund before investing. The fund's prospectus contains this and other information about the fund and should be read carefully before investing. You may obtain a current copy of the fund's prospectus by calling 800-544-6060.

Per the most current prospectus, (1) Fund total operating expense ratios are: Class A, 0.92%; Class L, 1.57%; Institutional Class, 0.92% until at least May 31, 2024. (2) In addition, the Adviser has entered into contractual expense limitation agreement with the Trust so that the Fund’s ratio of total annual operating expenses are limited to 0.84% for Class A shares and Institutional Class shares and 1.49% for Class L Shares until at least May 31, 2024.

Fixed income investments are affected by a number of risks, including fluctuation in interest rates, credit risk, and prepayment risk. In general, as prevailing interest rates rise, fixed income securities prices will fall.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. There is no guarantee that this, or any, investing strategy will succeed.

Diversification does not ensure a profit or guarantee against loss.

There is no affiliation between Ultimus Fund Distributors, LLC and the other firms referenced in this material.

Control #: 17156219-UFD-7/20/2023