"All of life is peaks and valleys. Don't let the peaks get too high and the valleys too low." –John Wooden

May is one of those months where you seem to get lost in time. It is easy to lose track of where you are in the calendar, and just what season it should be. Your inner clock tells you it should be spring, maybe hopeful that it is summer, but the volatility of the weather masks it. Sometimes it feels like spring. Other days it shifts enough that you feel like maybe it is the end of fall. You suddenly get those one or two days where it feels like someone turned the heat lamp on and it’s incredibly hot. I’ve lived in both Colorado and South Dakota, and the occasional May snowstorms there would have you questioning the value of a calendar; sometimes it felt as if winter was never over, and spring never existed. When it comes to weather, May is a month where you see many peaks and valleys.

As volatile as rates have been over the past 9 months or so, as we have pointed out recently, so too have credit spreads. The market has waffled back and forth almost on a daily basis as to whether inflation or recession is the boogieman. This goes hand-in-hand with the flipflopping the market does as it decides whether it will be a risk-off or risk-on trading session. The shifts in credit tone are in many cases extreme, with spreads moving dramatically, especially so as one might expect, in high yield. This creates perceived peaks and valleys in terms of risk. Yet one of the largest components of the capital markets, the rating agencies, typically try to stay above the fray, avoiding that type of whipsaw. In fact, as we are told, ratings are meant to withstand peaks and valleys. For instance, corporations (based on economic environments, sector pressures, consumer preferences, and individual firm results over periods of years) will naturally go through periods of time that include peaks and valleys as far as performance is considered. As such, their credit ratings are supposed to take that into consideration. They are supposed to, if applied correctly, have enough give and take that, outside something dramatic like fraud or a product suddenly being designated as unsafe, the ratings should remain relatively stable.

In reality, it doesn’t always work the way that it “should”. During the Great Financial Crisis (GFC) particular attention and blame was placed on the rating agencies. As a group, they were taken to task during that period of time, accused at first for not anticipating the downturn or not acting despite the warning signs and, in certain cases later, for ignoring warning signs for reasons that impaired their company profits. As the financial crisis evolved, the rating agencies seemed to be intent on making up for lost time and began to aggressively downgrade asset-backed deals and corporate ratings. More so on the corporate side than the structured side, they were later derided for knee-jerk reactions and acting too aggressively. Many of these corporate actions (downgrades) were later reversed, a no-win situation for the rating agencies at the time.

Recently we were witness to a small snippet of something similar. During the initial phases of the pandemic, rating agencies moved aggressively across the corporate and structured spectrum to downgrade and slap negative watch and negative outlook designations on a number of issues and issuers. Not quite as aggressively or dramatically as what we had witnessed during the GFC, but enough to remind us of the similarities. It would seem therefore that perhaps in times of distress the peaks are just that much sharper and the valleys that much shorter. In other words, the ratings didn’t seem as stable as one would imagine.

To some extent the criticism is unwarranted. There is a lot of misunderstanding of what a rating really means and the limits to what the rating is meant to tell investors. Rating agencies, for corporates and structured, spend a lot of time of looking backward, utilizing history to help anticipate what is in the future. But there are always variables, including shifts in management responsibility and initiatives that can’t be anticipated. For structured products, the pandemic was an eye-opener. Who could have anticipated that an assetbacked deal backed by gym memberships would suddenly be at risk because no one was allowed to leave their house? While it does seem the timing of reactions for rating agencies has shortened, that usually seems more in response to times of stress. Typically, without those black swan type of events, rating agencies and rating actions seem to lag versus current conditions.

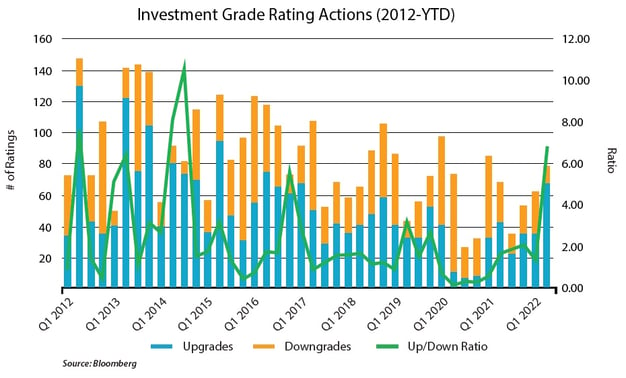

As can be seen below, for investment grade firms, some of the items we have discussed are illustrated quite well. In 2nd quarter 2020, during the initial phases of the pandemic, downgrades dramatically overwhelmed upgrades. For 2022, one can see however that rating actions favor upgrades over downgrades. The rating agencies are pleased with recent results and have aggressively moved to reward those companies with favorable rating actions. The up/down ratio is well over 6x.

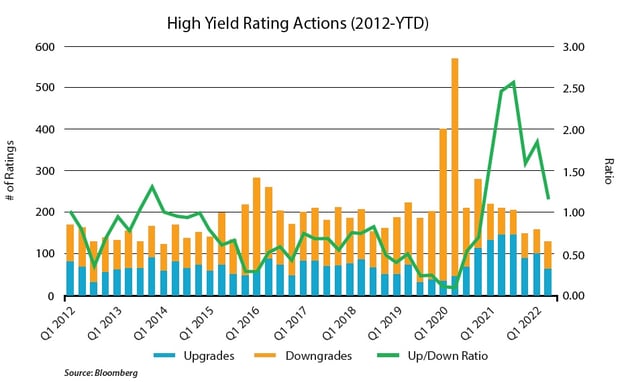

For high yield, a similar story existed with regards to reactions in the initial phases of the pandemic, where rating actions were overwhelmingly negative with numerous downgrades and a pocket full of upgrades. Since that time, upgrades have outnumbered downgrades. We are of course post the Fed stepping-in, post resulting recovery, and at a moment in the financial markets in which many believe us to be in a benign credit environment. While the chart does show the up/down ratio dropping over the past 2 quarters, the ratio remains firmly above 1.0x; indicating that still, up to this point, upgrades are numbering more than downgrades.

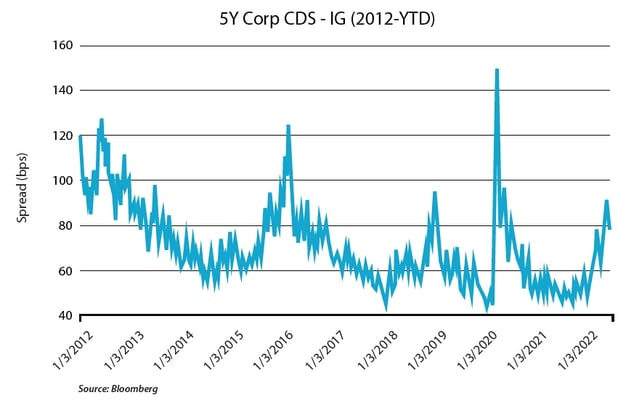

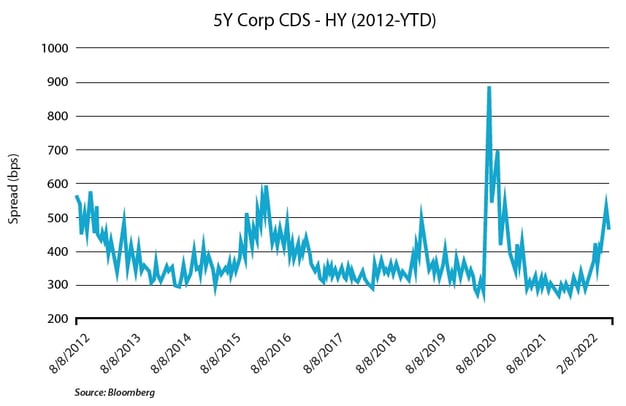

It would seem, based on the charts above and rating agency actions, that we are in a favorable credit environment. Indeed, not only a favorable one, but one that is directionally strong. Yet, while that might be the rating agency viewpoint, the market isn’t quite acting in that manner. As illustrated below for both investment grade and high yield, credit default swap (CDS) spreads continue to tick higher. During a time that rating agencies are moving to upgrade firms in a ratio indicating more upgrades to downgrades, the overall CDS market is ticking up. This indicates to us that it is becoming more and more expensive to hedge your credit risk using synthetics and indicating a softer and softer view on credit overall.

One interesting similarity is just how the CDS market and rating agency actions mirrored each other during the initial phases of the pandemic. In CDS, one can see spikes in spreads during the time in which rating agency downgrade actions far outnumbered upgrades. One should expect CDS to react quickly to market conditions. That is the value of using an instrument that is cheaper and easier to execute than the physical sourcing, buying and selling of cash bonds being to lend a voice to one’s position or bias on credit. What is surprising however in that instance is just how fast rating agencies were quick to move. Perhaps the rating agency actions can be explained simply by their reluctance to go through the same amount of blame they were showered with during the GFC for acting too slow and have now moved to a more aggressive tone when dealing with outlier credit events. That would also seem to indicate that the peaks and valleys approach rating agencies take seems to come with some caveats.

Nevertheless, we aren’t in one of those moments. We are in a different type of market and rating agencies are not reacting. Rather they are acting as they normally do. Currently the CDS market is directionally indicating a market where credit is getting softer, worsening, at the same time rating agencies by their actions are indicating the alternative. Here is where opportunity can exist. Rating agencies tend, outside times of stress, to be laggards. That is, because a great deal of how they approach credits can be backward looking, based on performance, with a sprinkling of forward thinking based on management comments. As such, rating actions can lag overall market movements. What that tells us is that by using the CDS market as a gauge, we can move in an anticipatory manner as we consider sectors and issuers to target for selling as well as purchasing. We would expect at some point in the near future the up/down ratio for both investment grade and high yield rating agency actions to move closer to and perhaps under 1.0x. CDS is in some ways telling us that right now. Thus, this presents opportunities to sell certain credits at their peaks and move into credits that spreads would perhaps indicate as buys. More importantly perhaps is an understanding that the lag in rating actions and CDS moving in a different direction might be a sign that credit deterioration isn’t being fully priced into certain bonds which could be downgrade candidates in the future.

Rating agencies tend to be vilified, especially in times of stress as investors look to place blame. An appreciation for their work as well as what ratings signify can help performance.

There are many signs in the marketplace that can help. Overlaying our targeted issuer list over market data in combination with signals such as rating agency actions can potentially lay the foundation for future outperformance.

|

|

Definition of Terms

Basis Points (bps) – refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature – A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) – A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) – A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) – A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO – The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) – An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) – The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) – One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) – A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) – a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) – a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta – the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) – fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) – a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) – a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Net Asset Value (NAV) – represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 – The Standard and Poor’s 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX – The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ – The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index – The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei – The Nikkei is short for Japan’s Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan’s top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite – is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

MOVE Index – The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index – The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average – The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng – The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 – The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 – The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) – is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk – the name economists give to the risk associated with the sensitivity of a bond’s price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) – the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) – the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) – high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) – an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) – an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) – a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) – an organization that invests in small- and medium-sized companies as well as distressed companies.

151824568-UFD-6/16/2022