“The secret of life is honesty and fair dealing. If you can fake that, you’ve got it made.” - Groucho Marx

We are at the mid-point of the calendar. Halfway there. Or halfway done? I guess that depends on whether you are an optimist or a pessimist. My wife and I visited Hawaii years ago. We did the usual tourist things. One of which is the Road to Hana drive. It’s in all the tourist books. A fantastic, scenic ride on tight but paved roads. The books tell you to drive halfway, have some lunch, maybe check out the local tourist merchandise, then turn around and go out the way you came in. It’s a full, slow day. A perfectly relaxed, vacation-friendly day. A “friend” of mine convinced me however that merely driving halfway and turning around wasn’t the move. Rather he insisted I keep driving and go out the “back side.” So, we drove leisurely in, had a nice lunch, and then, taking his advice, ignoring the whole drive out the way you came in move, I hopped behind the wheel of my rental car and went out the back side. It was one of the most harrowing drives of my life. A white knuckler on a frightening road that turned into one lane in various spots, making you negotiate space with traffic coming the other way. There was also limited to no guard rails and ultimately, I had to battle against bottoming out my rental car in massive, crater-sized potholes. I never forgave that “friend” for that advice.

So, as we hit the halfway point of the calendar of what has been a bumpy first half of the year, we must consider where our footing lies and what options might be available going forward. Having learned a valuable lesson in the past, we also feel it important to see what our “friends” are telling us; are they being helpful or are they actually not helping at all?

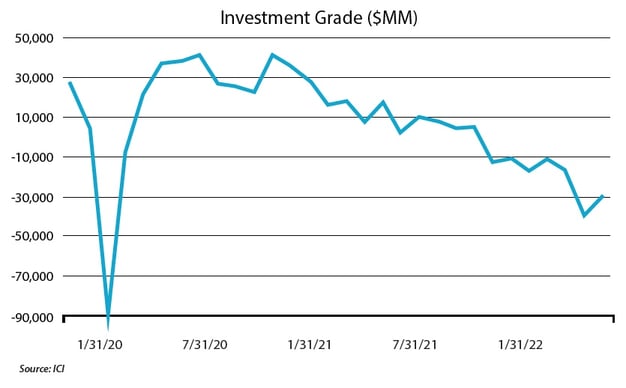

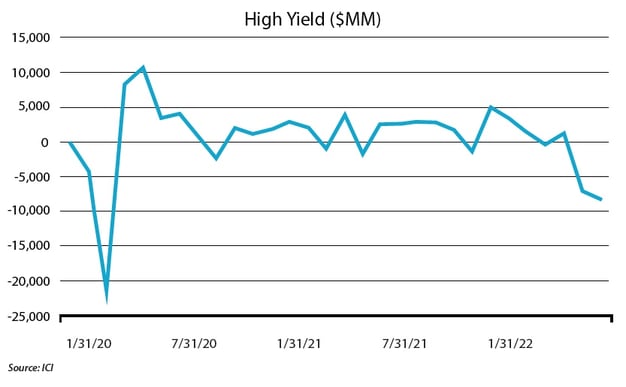

As we have discussed of late, the market has flip-flopped almost daily on whether it fears inflation or recession more. The daily change in attitude has caused havoc in rates and credit spreads. Over the last few weeks of June, it seems recession fears have won the short-term battle and we have seen rates rally and stabilize a bit within a band while credit spreads leak further and further out. A good part of this widening can be attributed to liquidity premiums rising. While fears of a recession are mounting, most corporate reporting (beyond some recent concerns in the leisure sector such as cruise ships) has been, at worst, fairly benign. And yet at the same time spreads have marched further and further out. A good deal of the pressure on liquidity has come from mutual fund flows. It hasn’t mattered much whether funds are investment-grade-focused or high-yield-concentrated, all bond funds have seen flows turn somewhat negative, with some positive traction only now appearing recently in IG.

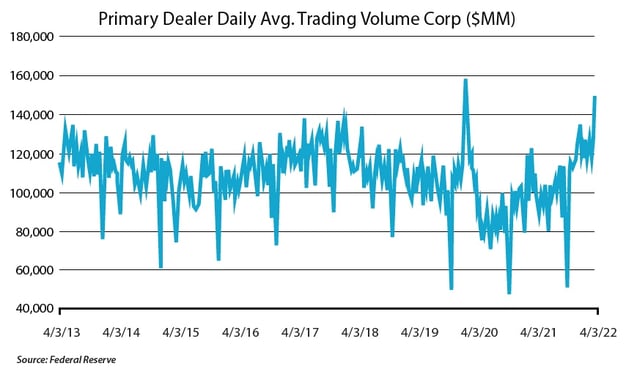

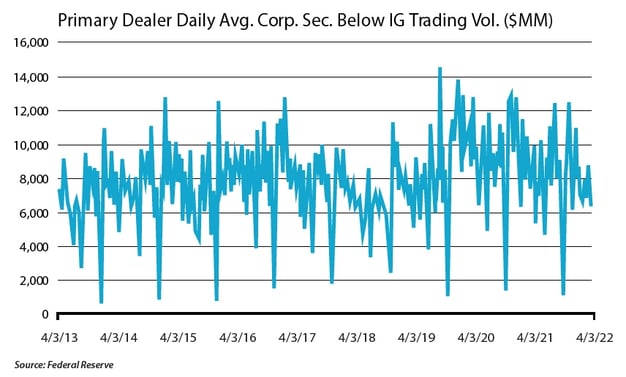

That type of reported movement in flows should result in trading activity increasing to the point of being robust; that is exactly the type of activity we are seeing. The charts below illustrate it quite well. However, interestingly enough, what the charts below don’t show, with regards to primary dealer activity, is a large reason why we would surmise liquidity premiums are increasing.

Typically, with an increased amount of trading, one would expect strong liquidity. In this case, however, we are seeing liquidity premiums increase and price concessions rise. This is resulting in OAS spreads overall widening to levels in some cases that mirror levels not seen since the early days of the pandemic, prior to Fed intervention.

This brings us back to the primary dealers. As we mentioned above, the charts would seem to indicate heavy primary dealer participation. It is important to note that when we use the term “dealer” what most are referring to are the primary dealers; the big names in the marketplace, those who carry large balance sheets and can afford to position securities. Anecdotally, what we have heard from many market participants is a common refrain: the dealers are not looking to buy anything, but at the same time they seem reluctant to sell anything. Thus while trading activity illustrated above would seem to indicate they are still participating, what the chart is really telling us is that the activity is mostly customer to customer, with the primary dealers merely acting as a conduit. If true, this unwillingness to support or participate in this market might be exacerbating the issue, contributing to the liquidity premium rising.

But that is market chatter. And talk can be cheap. Does the data support this?

Primary dealers take a lot of heat for a variety of reasons. In good and bad times, they are accused of acting in their own interests rather than that of their clients or even of the markets. It is important to note these are for-profit businesses. Nevertheless, the larger dealers hold a unique position of reaping the benefits of appearing to be market-makers, while having little downside when they decide that they no longer need to do so. They routinely bring large primary issuance deals to the market, headlining as lead or back-up underwriters and are then tasked with allocating to clients’ orders on those deals. Post-issuance, many investors look to them to support deals, especially new ones, providing bids and using balance sheet to position that security, helping to create a liquid market for those deals. Not participating in this manner can create a sense of confusion in the market as even new issues, months old, may not find a supporting level bid from those dealers on the syndicate that announced, priced and allocated that deal. This in turn has a detrimental effect on how that bond trades and can, if no support is visible, cause liquidity premiums to widen out on a recent issue deal causing pain to those investors who participated in the deal at launch.

As illustrated below, primary dealer positions in corporate securities have been falling over the past 6 months to near 10-year lows. The only time we saw a serious spike in holdings was shortly after the Fed intervened in the bond market, which was obviously an advantageous moment to hold securities that suddenly were going to be heavily in demand. Since that time, and especially since the start of the current year, the amount positioned has been falling regularly, indicating a lack of buying or providing supporting bids in the marketplace.

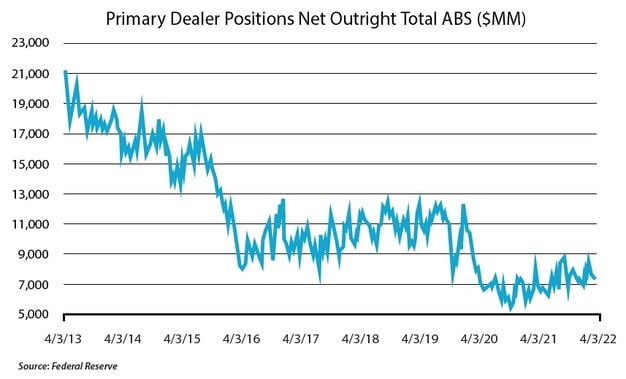

A similar pattern emerges across other credit sectors. ABS typically has much smaller amounts of issuance overall, but also has a much smaller investor base to that of corporate debt. That characteristic can make it easy to justify for the primary dealers a reduced willingness to position, but the overall result is the same. What we see is smaller holdings, and liquidity premiums, rising in outstanding securities.

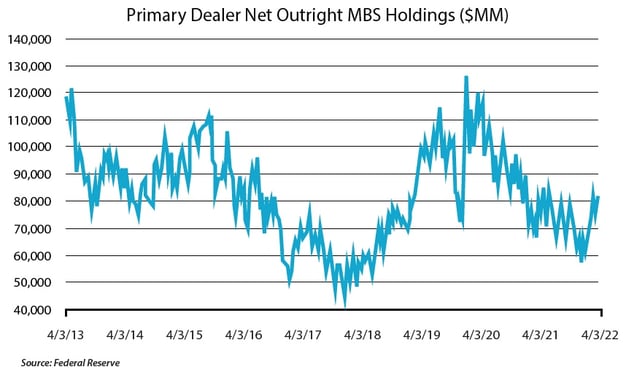

This type of activity, or even lack of it, tends to push liquidity premiums higher and thus spreads wider is also pretty evident in Agency MBS. This sector has been hit quite harshly over the past 9 months, with widening spreads becoming the talk of the market, as this sector has underperformed at a near historic clip. A lot of attention has been paid to the fact the Fed is in the process of winding down their holdings and potentially negatively impacting the market. Lost in that explanation with regards to overall performance, perhaps, is the role the dealers themselves seem to be playing.

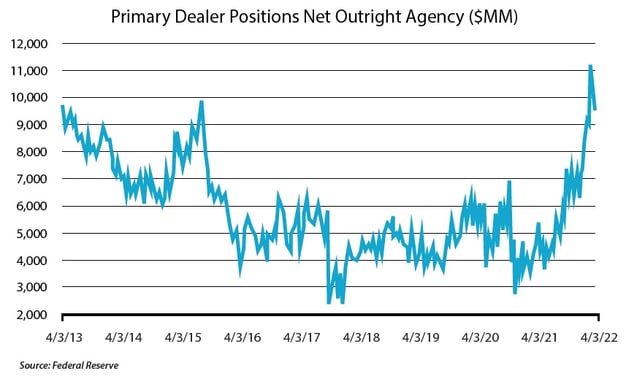

The only place the primary dealers seem to be adding to their positions? Well, it would seem to be Agency paper. With interest rate movement and yields on treasuries climbing, one could see rate volatility having an impact on rate sensitive securities such as MBS. In addition, with a looming concern about credit due to recessionary pressures, dealers would appear to also be stepping away from those markets. Thus, it seems natural that if they were going to use balance sheet, they seem relatively open to it being used for more vanilla, liquid holdings such as Agency paper.

The inaction of the major dealers surely seems like it is affecting the liquidity premium now being folded into the spreads of corporate bonds. It is somewhat noticeable in investment grade securities, and very obvious based on price concessions in high yield. This shines a spotlight on just how markets operate and how even the slightest shift in how each counterparty is operating can have an affect on the overall feel and efficiency of those markets. There are a great deal of smaller dealers that operate in a customer to customer manner now, and always have done so. Those dealers tend to be smaller and thus have limited to no balance sheet to act in the manner of market makers. Their role is mostly to act as a conduit between buyers and sellers in the market, and they have operated in this manner historically. There has been no departure in how this role is played and so no change in how the market would operate when considering this. The larger dealers, the ones you see as lead underwriter on large syndicate deals in the primary market, typically are leaned on to operate or play a different role, that of more a market maker. When those large dealers shift their operation type, start shutting down their balance sheets, and morph into the characteristics more regularly expected of the smaller dealers, it causes a shift in how markets operate and contributes to spread widening. We have seen extreme cases of this during the Great Financial Crisis and more recently, for a shorter period of time, during the initial days of the pandemic. Recently however, it has been less focused on as a contributing factor to what we are currently seeing in the fixed income markets. In this particular case it is far more stealth, but if you dig deep enough, evidence seems to be there that it is happening, albeit in a more stealth manner or one without the screaming headlines.

Data points like this are not only a good reflection point on just where markets are, but as we have said in the past, an indication of where opportunities are available. The dealers are not going to shift balance sheet usage overnight, and thus, it would seem that taking advantage of opportunities by providing liquidity in a targeted manner are going to be available for the near term. Once sentiment shifts and dealers open up their balance sheets again, we would expect spreads to tighten dramatically. That would indicate that legacy positions are seemingly on the cusp of some sort of tightening and a recovery of performance. More importantly, by hoarding cash and selectively pruning exposures to create more cash, one may build value in the portfolio by taking advantage of a moment, in the right securities, to potentially build future performance when maybe credit is less of a concern, but liquidity premiums are advantageous and demanding attention.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

MOVE Index - The ICE BofA MOVE Index (OVE) measures Treasury rate volatility through options pricing.

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

You should carefully consider the investment objectives, potential risks, management fees, charges and expenses of the fund before investing. The fund's prospectus contains this and other information about the fund and should be read carefully before investing. You may obtain a current copy of the fund's prospectus by calling 800-544-6060.

Fixed income investments are affected by a number of risks, including fluctuation in interest rates, credit risk, and prepayment risk. In general, as prevailing interest rates rise, fixed income securities prices will fall.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. There is no guarantee that this, or any, investing strategy will succeed.

Diversification does not ensure a profit or guarantee against loss.

There is no affiliation between Ultimus Fund Distributors, LLC and the other firms referenced in this material.