“It isn’t the mountains ahead to climb that wear you down. It’s the pebble in your shoe.”

- Muhammad Ali

We are deep in the Fall now. There is a lot to say about that. I typically like hot weather more than I like the cold, but there is something very appealing about a crisp Fall day. I’ve always been jealous of the portrayal of Fall in coffee or cigarette ads. Those people look like they are having a lot of fun while wearing flannel shirts: running through some leaves, playing touch football, or maybe doing the “two hands on the mug” sip of their Taster’s Choice coffee while looking thoughtfully out their cabin window. I have kids. If I’m sipping coffee, it’s because I am trying to revive myself before they wake up. Nevertheless, I do look forward to the Fall. One of the pleasures of the weather turning cooler on the East Coast is that the air clears off the flying bugs we get in the deep summer. I’m not an entomologist, so I don’t really care what the names of those things are, but there are enough different breeds of them in the air to ruin any summer day. That is especially true around dusk when you think you’ve finally made it through the worst of the heat, only to be greeted by a swarming army of winged intruders. At the end of the day, of course, it isn’t that the individual gnat ruins the day; the constant swatting away of these little pests wears you out. At some point, you succumb. You either sit still and accept that you are the meal or go inside, because there is a tipping point where you realize staying isn’t a great option.

Similarly, the market seems to have grown as weary of rate worries as I do of the summer mosquito. It feels as if we have succumbed. We are no longer swatting them away but instead just sitting still, waiting for a change of seasons. The market has now lived two years through this situation. While data has been encouraging, there has been enough non-encouraging information to keep breathing enough heat into the system that it gives the Fed room to keep insisting they aren’t done just yet. Despite the feeling in the market and that of participants that the end is clearly within sight, there are just enough gnats in the air to make it still a little uncomfortable.

Another part of the rate hikes that isn’t so easily dismissed is the cost. Bloomberg recently published an article that indicated that corporate issuers are looking at an additional $80 billion in cumulative interest costs through 2026 with the current type of rate environment and outlook we are stuck in. According to Bloomberg, that includes an extra $27 billion a year for blue-chip and high-yield fixed-rate refinancing costs between the coming year, 2024, and 2026. This strikes us as more of an issue than a small mosquito bite. But perhaps more importantly, as we grasp and maybe appreciate the higher rates in terms of levels from a historical standpoint and current economic conditions, we also need to contemplate what having higher rates actually means for credit down the road. The longer we are at this level, the more impact it has on what will happen in the future.

This is especially important when considering corporate credit. In this case, we could consider liquidity as a first step. A reflex response to higher rates would be to consider how much it has impacted access to the market for issuers, represented by the primary market, and how much it has influenced secondary liquidity, which investors tend to worry about. When we look at primary issuance, at first glance, it would seem it has caused a bit of a pause. Daily, we see corporations trying to time the market. When rates are selling off, we see deals postponed. While that isn’t such an issue for a large corporation that is issuing for general corporate purposes, it can cause an issue for companies that need to issue in a shorter time span to handle refinancings.

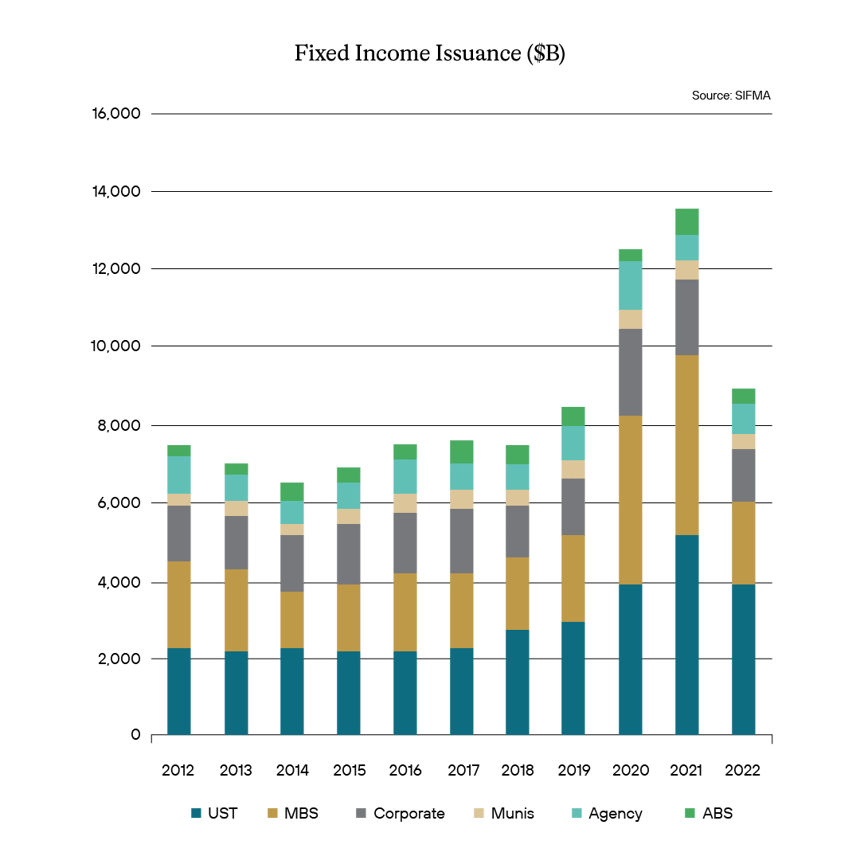

As can be seen below, fixed income had an incredible jump in 2020 and 2021 in terms of issuance. With corporations, as we have discussed in the past, feasting on the post-pandemic low-rate environment, there were new highs in terms of issuance. Also feasting was the government. But that all changed in 2022. With rate hikes starting at the end of the first quarter of that year, issuance slowed. Or so it would seem. For a big picture look illustrated below, it indicates that issuance did slow from the previous post-pandemic rush but, in most cases, slid back to where it was pre-pandemic. Total issuance went from around $8.4 trillion in 2019 to $13.4 trillion in 2021, before falling back to pre-pandemic levels in 2022 at $8.9 trillion.

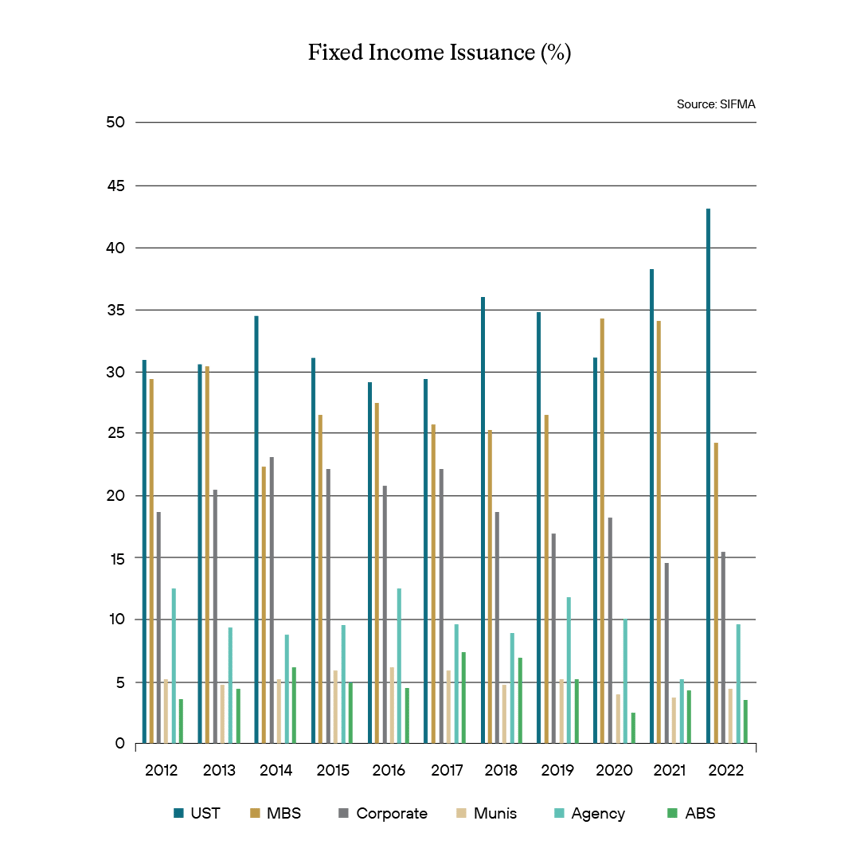

Perhaps more importantly, we need to drill further down. For although the total issuance did fall, what is also important is the asset classes, the shift in terms of what made up this issuance. Agency MBS, for instance, which had to deal with the Fed letting their balance sheet run off at the same time that banks stepped away from buying, led to lower and lower demand, translating into lower issuance. Indeed, Agency MBS issuance went from around 27% in 2019, where it consistently had been previously, up to 34% in 2020 and 2021, before receding to 24% in 2022. Only treasuries continued to really climb in 2022, in terms of percent of total fixed income issuance. But it is worth noting that corporations, which historically had been at or a little over 20% in terms of annual issuance percentage of total issuance, fell to 14% and 15% in 2021 and 2022. This would seem to indicate as rates started to rise, corporations for whom those additional financing costs can cause a crimp in their credit started to step back from issuance, reluctant to take on the additional interest costs of issuing into this rate environment.

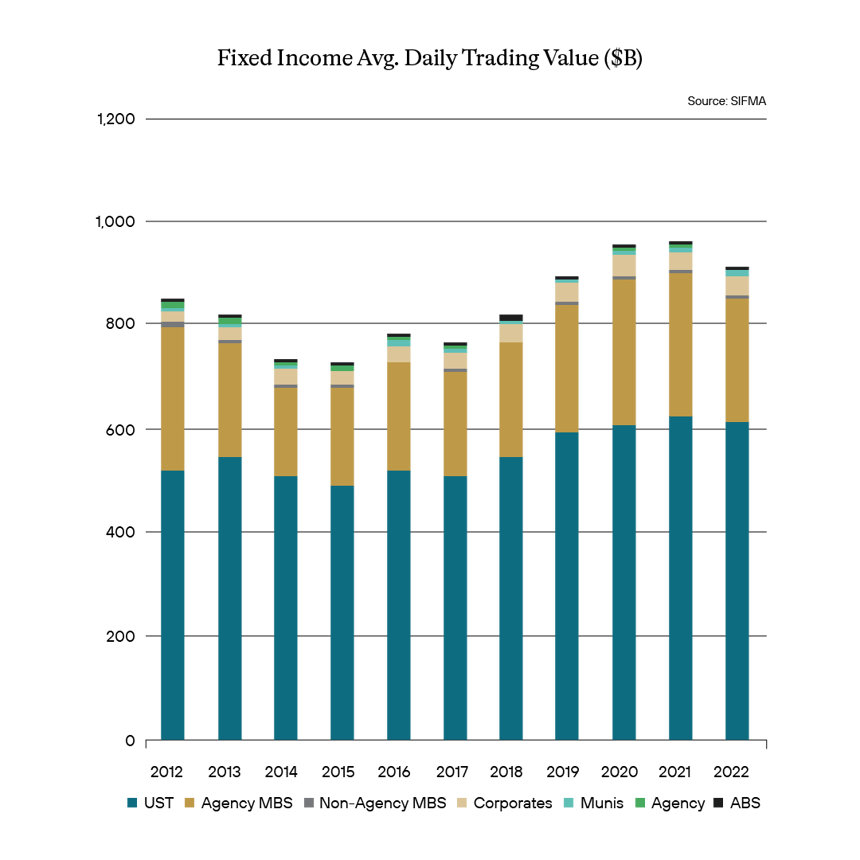

Interestingly enough, the rate hike environment doesn’t seem to have impacted secondary trading as much as one would expect. Daily trading averages in terms of volume seem pretty consistent with the past years. And on a cursory view, it would seem pretty much business as usual. But much of that is buried in the fact that much of the daily trading volume is focused historically and recently on a large concentration of the most liquid sectors such as treasuries and agency MBS. As such, when looking at a 20,000-foot view, nothing would seem to have changed much even through this cycle.

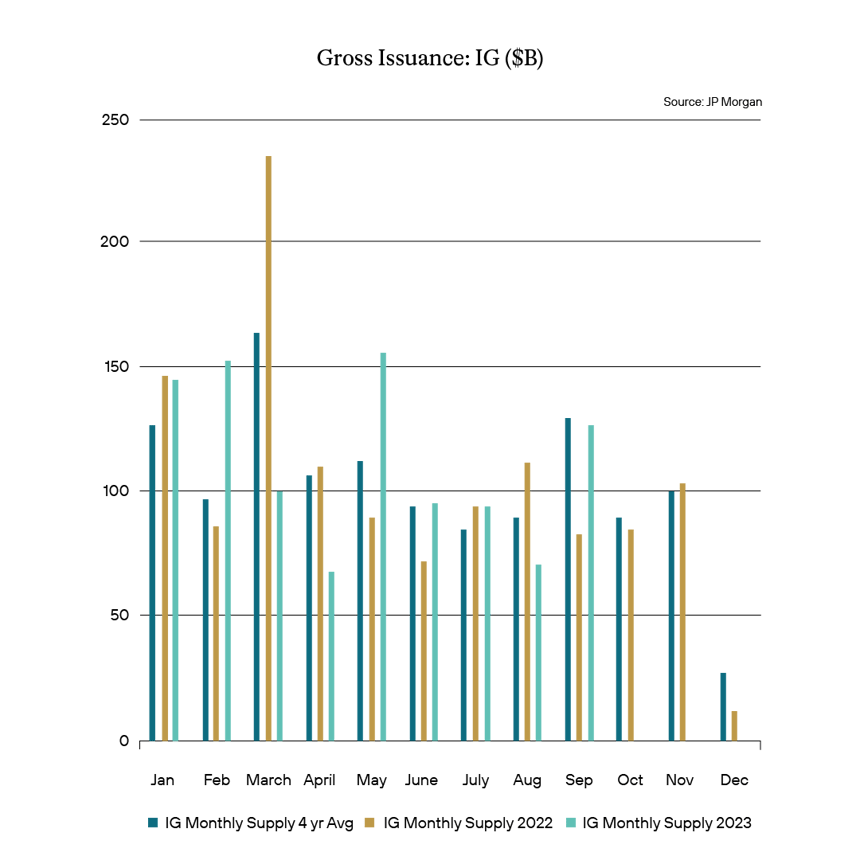

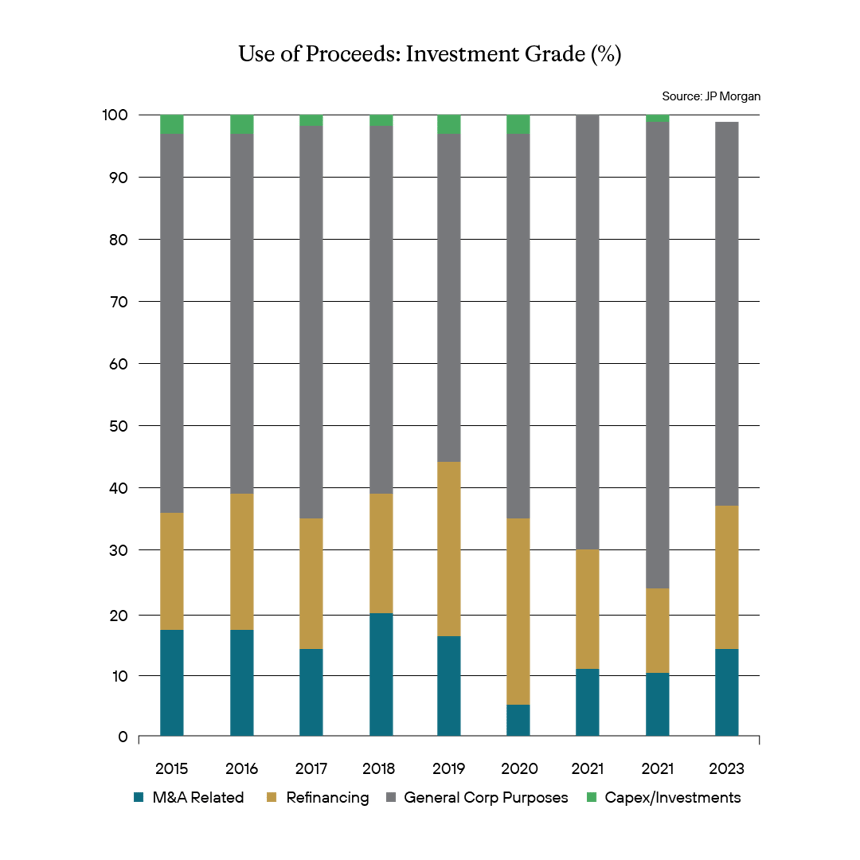

However, stopping there would be a little misleading. Once we dig deeper, things from the standpoint of credit in the corporate world begin to reveal themselves to be more concerning. As an example, gross issuance for investment grade credits is reasonably consistent with what we have seen for the past four years and what we have witnessed versus last year. The reason for that is discussed below. Nevertheless, it would be expected that levels would be maintained.

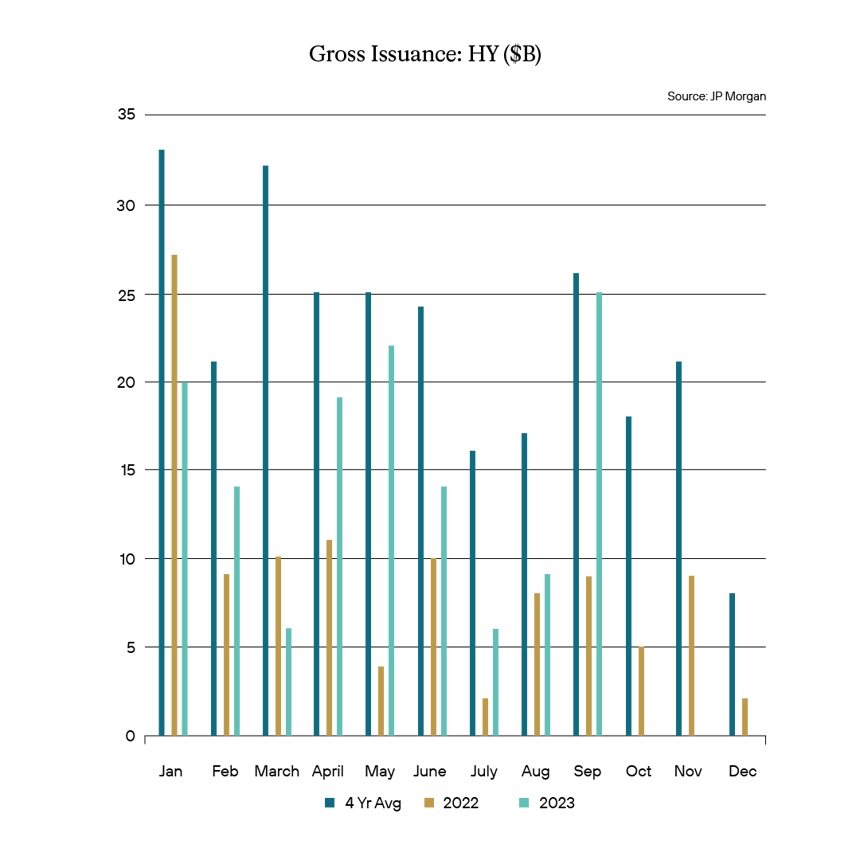

For high-yield, the story is a bit different. This becomes especially obvious when comparing the issuance of 2023 so far versus last year. Again, we have been in a rate hiking cycle, and clearly, a firm would prefer not to have to borrow at higher rates if necessary. As JP Morgan pointed out in a recent research article, the high-yield capital market had a great deal of activity. In fact, the market saw gross issuance of around $25 billion, its highest level of issuance since January of 2022.

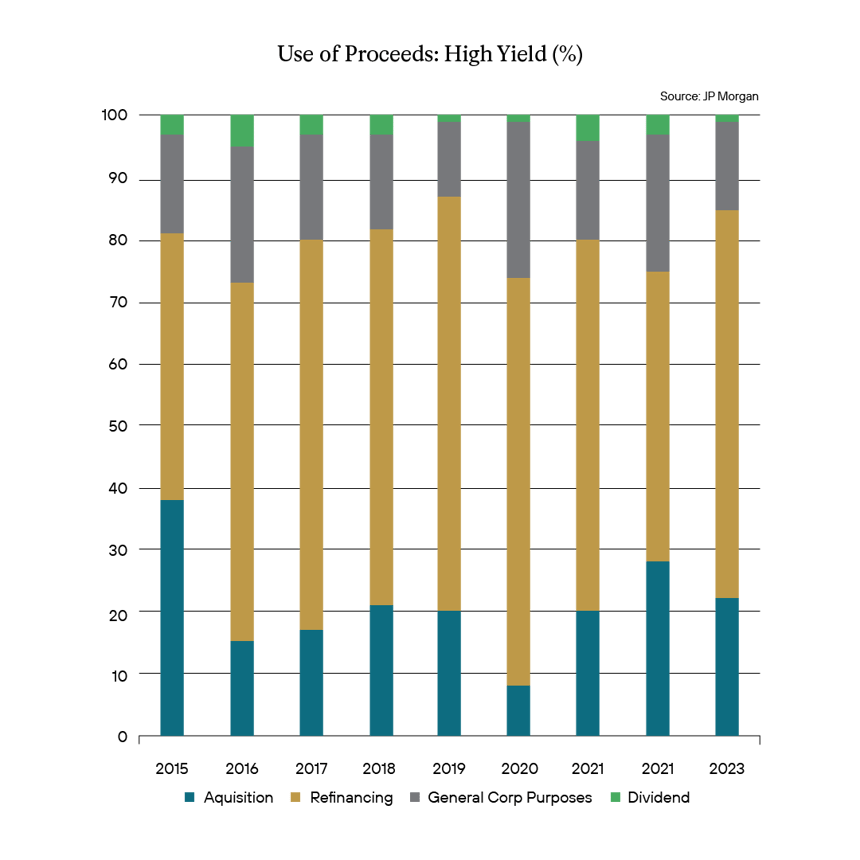

The use of proceeds explains a big part of this. For investment grade credits, a good reason for their issuance levels to be consistent with last year’s and the 4-year average is that most of that issuance is for general corporate purposes. General corporate purposes in 2023 thus far represents some 62% of issuance, versus 75% last year, and in fact, is right at the 10-year average of around 62%. For high yield, the most significant percentage of issuance is for refinancing. That jumped from 47% in 2022 to, so far, around 63% in 2023. Not only is that a significant increase over the prior year, it is quite a jump from the 10-year average of 58%.

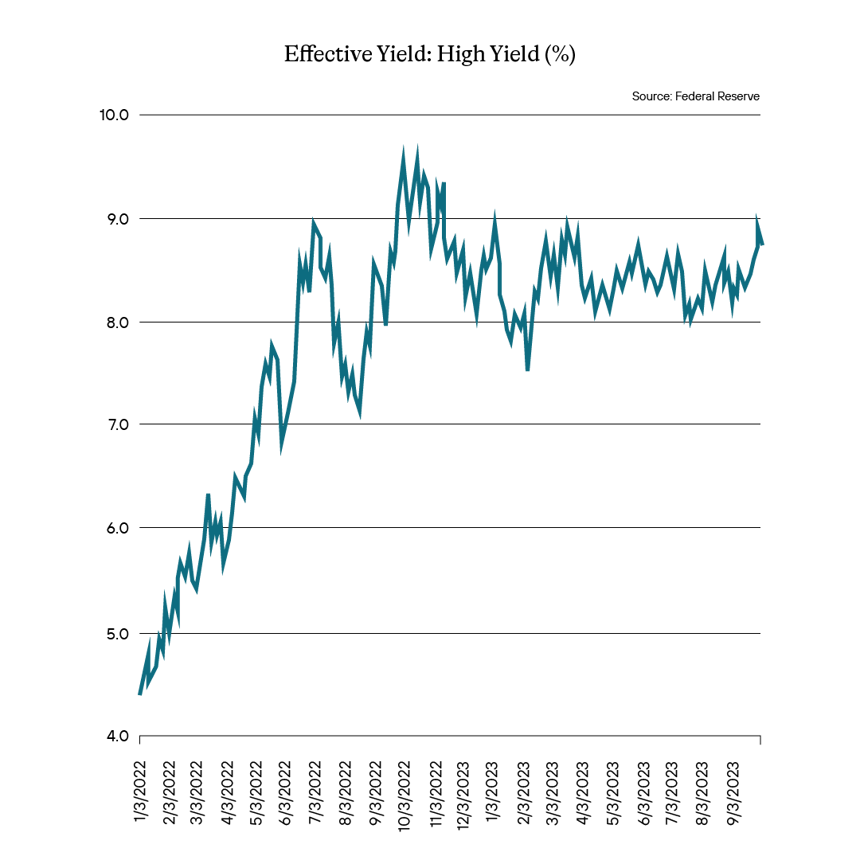

And therein is the concern. At the weakest end of credit, the cost of financing themselves is vastly essential to many of these firms being able not only to thrive, but to survive. If one is forced to spend 63% of your issuance dollars to refinance older, cheaper debt, then there is an issue regarding health. Why would you refinance in this environment unless you had to? All the more obvious a question when one looks at how the effective yield for high yield has continued to increase over the past year.

What the investor base expects to get paid means that firms will have to step up when issuing new debt, and that cost is punitive. As Moody’s points out in a Bloomberg article, non-investment grade firms will have $1.87 trillion of debt maturing between 2024 and 2028. Companies rated single B and below have $206 billion coming due in 2024 and 2025 and $1.1 trillion between 2024 and 2028. That is a great deal of debt that needs to be refinanced. As is most of the case, high-yield firms typically have few options to finance themselves and can’t afford to be picky when they do so because there is a genuine concern that the market can be closed to them at any time. An inability to roll over maturing debt could mean the end of their ability to function. This is sure to put more stress on those firms, and according to the article, Moody’s is expecting default risks to increase pretty dramatically because of it.

We have entered a point in time where we are so focused on the broader picture that things you would typically drill down into are being ignored. We have spent a great deal of time looking at credit spreads and there seem to be numerous articles and thoughts on the pain of higher rates, but outside mortgage rates, things such as this seem to be swatted away as if they are a tiny insect. But the higher rates, especially if they are with us for a longer time, as the Fed keeps insisting will be the case, can’t help but be a catalyst to weakening corporate credit, especially in the non-investment grade space.

We continue to expect a slowdown in the economy, and the higher rates for the longer mantra of the Fed don’t seem to be accommodating for longer-rated, weaker corporate credits. We expect those firms to have some issues in the near term, and the higher rates they are paying for financing could also ultimately lead to even the stronger sub-investment grade credits to see some pain. As such, we continue to like the trade-up in credit quality, staying higher in the credit stack as we navigate through a rate environment where the market does not seem to be appreciating enough currently, or the potential tail risk it represents. It is no time to be less vigilant on even the most minor pests.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

Home Equity Line of Credit (HELOC) - A home equity line of credit (HELOC) is a line of credit that uses the equity you have in your home as collateral.

Government-Sponsored Enterprise (GSE) - A government-sponsored enterprise (GSE) is a quasi-governmental entity established to enhance the flow of credit to specific sectors of the U.S. economy. Created by acts of Congress, these agencies—although they are privately held—provide public financial services.

Qualified Mortgage (QM) - A qualified mortgage is a mortgage that meets certain requirements for lender protection and secondary market trading under the Dodd-Frank Wall Street Reform and Consumer Protection Act, a significant piece of financial reform legislation passed in 2010.

Trust Preferred Securities (TruPS) - hybrid securities issued by large banks and bank holding companies (BHCs) included in regulatory tier 1 capital and whose dividend payments were tax deductible for the issuer.

Control #: 17499460-UFD-10/19/2023