“You get up every morning from your alarm clock's warning

Take the 8:15 into the city

There's a whistle up above and people pushin', people shovin'

And the girls who try to look pretty

And if your train's on time, you can get to work by nine

And start your slaving job to get your pay

If you ever get annoyed, look at me I'm self-employed

I love to work at nothing all day.”

- Randy Bachman

Halloween has come and gone. All that’s left is the hundreds of dollars of candy that my wife bought, apparently under the assumption that the whole state of Rhode Island would descend on our house that night. Worse, I don’t like anything that is left. Halloween is a tricky day to plan for. You don’t plan correctly, leave yourself short on supplies, and you are faced with turning off the lights, pretending you aren’t home, and hoping disappointed trick-or-treaters ran out of eggs a few houses prior. You over-extend yourself, and demand doesn’t match expectations. You are looking at piles of supplies that will ultimately lead to a doctor’s disapproving glare as you explain that you are not at fault for the weight gain as you simply cannot tolerate the wasting of food…well, food-type things that are coated in chocolate, nugget, and caramel.

Overextending oneself is becoming more and more a news item these days. We’re seeing a lot of attention being paid to the consumer as we contemplate the higher rate environment and what that means ultimately to those who need to borrow at these levels, what kind of impact it has on their monthly budget, and if it is indeed changing spending patterns. We rely significantly on the consumer to spend, spend, and spend some more. If they are spending what they don’t have, the overextension can lead to problems for the economy and, ultimately, each individual. The good news is we are spending. The bad news is, well, we are really spending. Initially, coming out of the pandemic, most of that was simply shrugged at, even cheered, as something we should expect coming out of a situation where the consumer was making up for the year when they were stuck in their homes. But it is becoming a little worrisome as we don’t seem to be slowing down. If it indeed was just a reaction to being home confined, that would, in theory, have meant a slowdown at some point as we tired from the pace and slowly weened ourselves off the spending. Instead, it would appear we are all getting used to it, and maybe it has become the new normal.

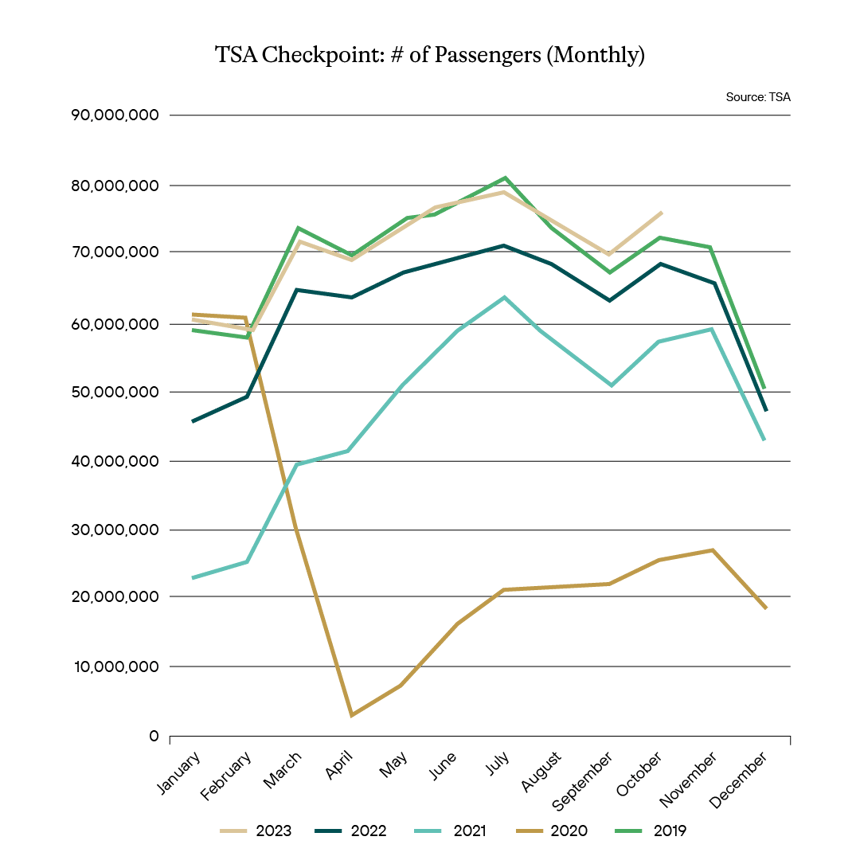

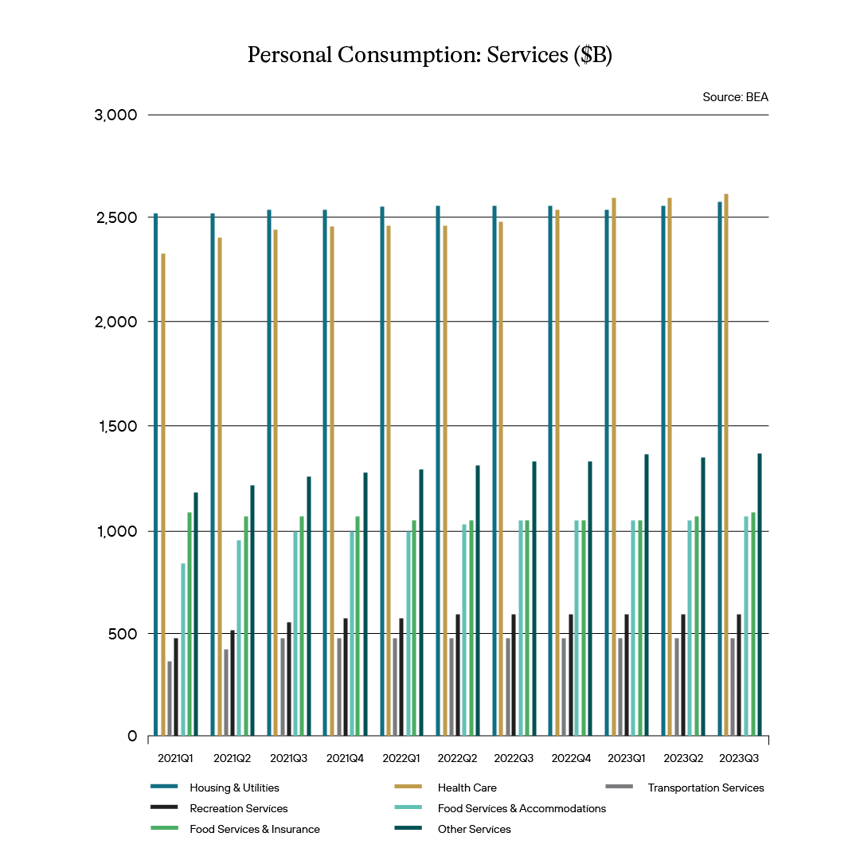

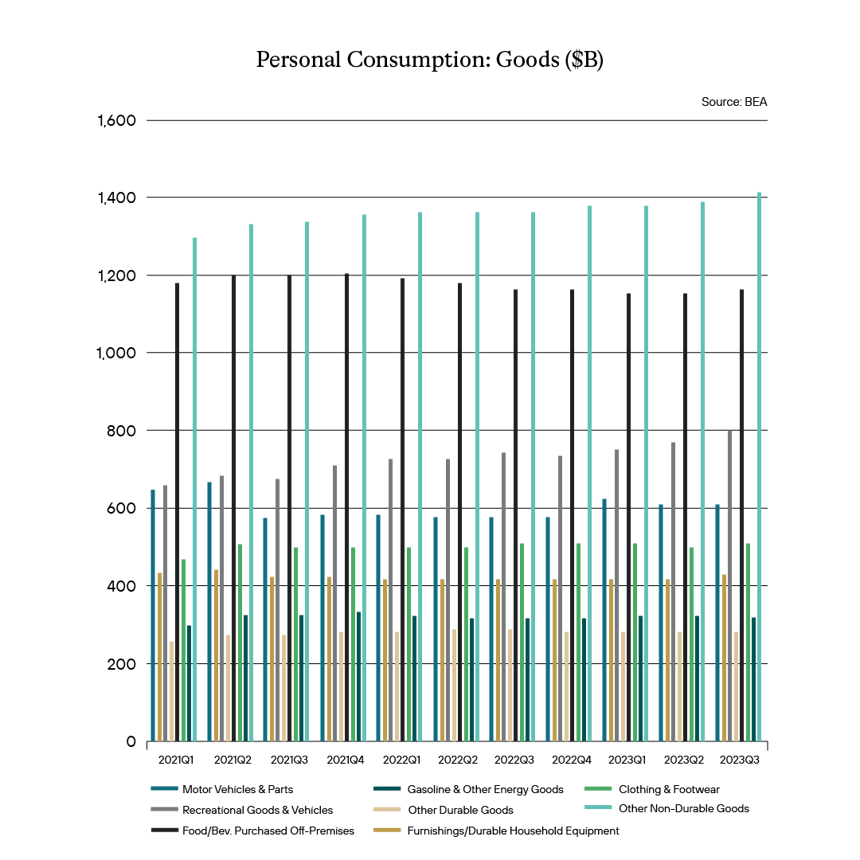

As the data and charts from the Transportation Security Administration (TSA) and U.S. Bureau of Economic Analysis (BEA) below indicate, we have reached a level where we are comfortable spending. Some of the below, like air travel, would, on its surface, indicate we have merely reached levels last seen in 2019, when rates were certainly lower, so what’s the problem? But that seems to forget that business travel hasn’t resumed to the levels seen in 2019, so the higher number of passengers seen currently is certainly more attributable to everyday consumers hitting the friendly skies. The other two charts, illustrating our spending on goods and services, indicate a similar story. Even at elevated levels for necessary items such as housing or energy, we still seem to have no problem spending on discretionary items at these levels over the past two-plus years. We aren’t slowing down, it would seem, even through the higher rate cycle.

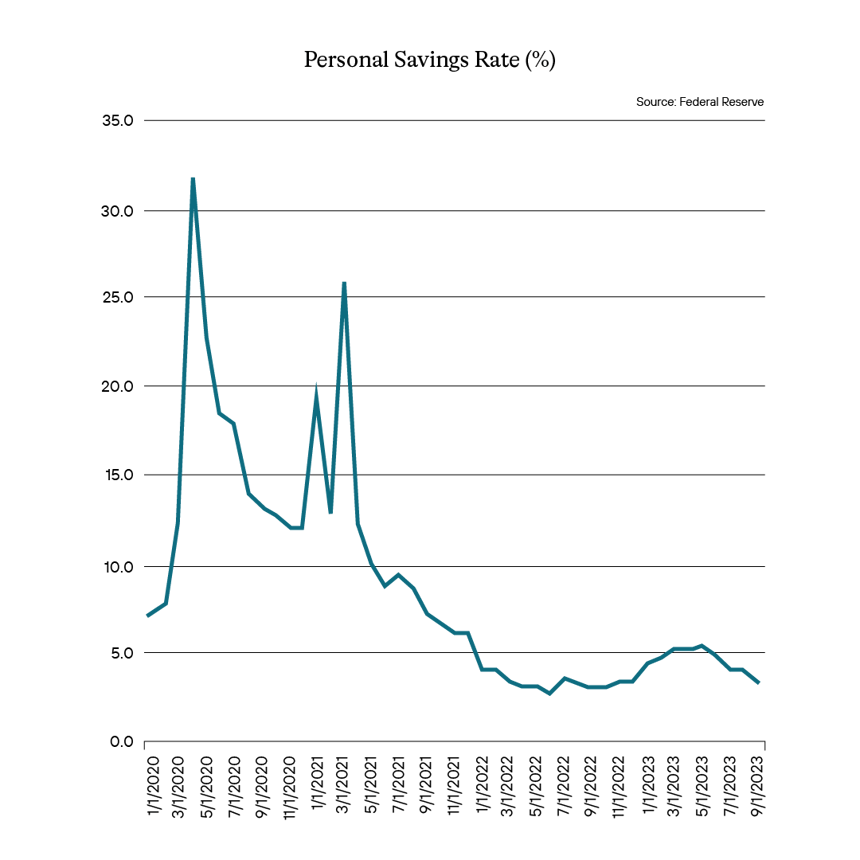

Should we be concerned? Higher rates should be, in theory, slowing us down, but they’re not. So just how are we paying for this? As we have pointed out in the past, and as illustrated below, we have already raided the rainy-day fund and our cookie jars. Our savings have been steadily extinguished. Gone are the pandemic days of a personal savings rate of 32%, and even a year into the pandemic, the personal savings rate, according to the Fed, hit around 26%. In fact, since that 26% mark, it has been a steady march down, and as of the end of September 2023, the Fed is reporting a 3.4% personal savings rate. So that seems less and less likely as a place we can tap going forward.

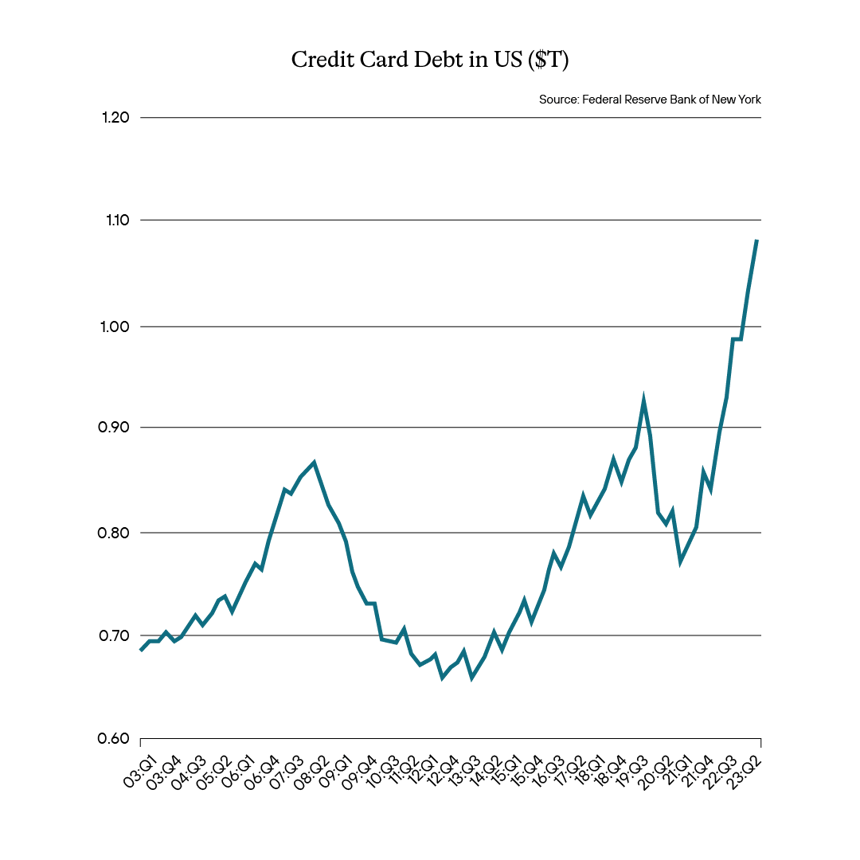

But we always have a credit card, and we apparently do love to charge it. That isn’t necessarily a secret. It has recently captured more than a few headlines. As a nation, we know what’s in our wallet and have apparently been using it to keep the good times rolling. As detailed below, as of the end of the third quarter of 2023, credit card debt, according to the Federal Reserve of New York, was reported to be over $1.0 trillion. Rarefied air, to be sure.

With usage of the card at highs and outstanding credit card debt as a result at highs (at a time that rates on outstanding balances have spiked), the cost of the debt to consumers is quite burdensome. And if you consider the fact that we are spending at elevated levels, there is real concern that if the economy slows down, or the jobs market softens, there could be plenty of pain coming our way.

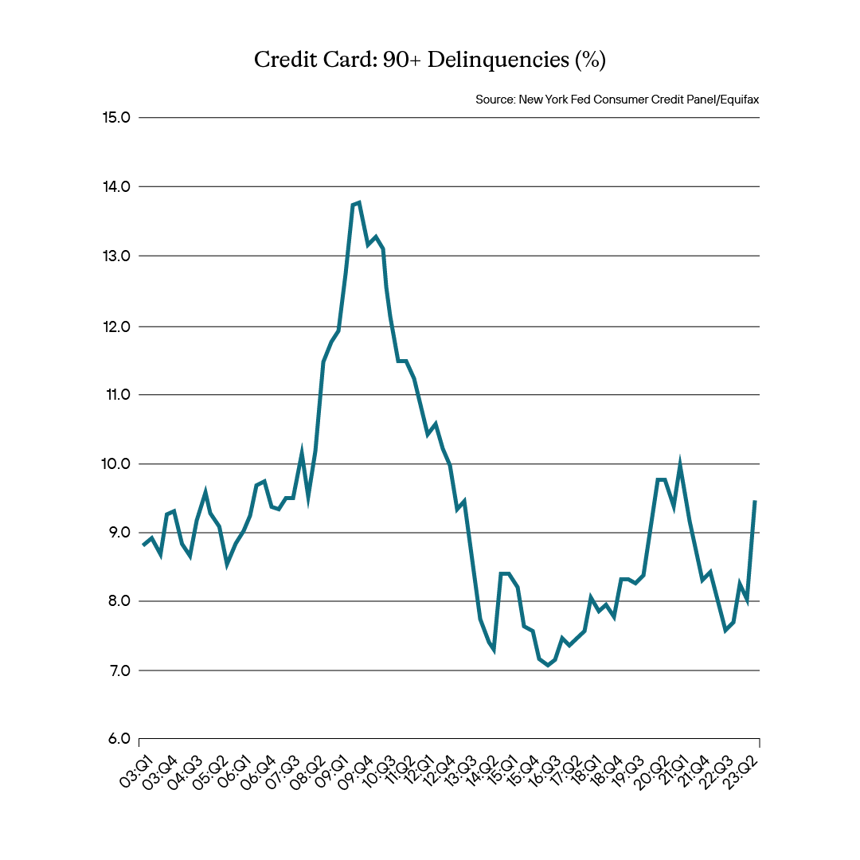

Some are downplaying the concern of delinquencies in consumer credit. That is understandable. After all, if we simply look at the chart below, one can see that current 90+ delinquencies are being reported at 9.43%, and while that certainly is elevated, it is still far below the peak during the Great Financial Crisis (GFC) which was reported then at around 13% in 2010. And so there are those who take comfort in that cushion. However, the 9.43% being reported today is pretty much the same as we saw being reported in the third quarter of 2008 (9.48%), or the beginning of the GFC. Perhaps that doesn’t quite bring the same amount of comfort. It probably shouldn’t.

We might be right at the tipping point for consumer credit. Even at this elevated level, it isn’t comfortable, but if we were to see a step back in the economy, we could see those delinquencies spike further. That would send us right toward what we witnessed during the GFC. On the other hand, if rates rally, maybe it pulls us back from that cliff. Certainly for the next few months, it’s something to pay attention to.

We continue to monitor parts of the economy for areas of concern. Indeed, consumer spending is a big one. The health of the consumer is of import for many reasons and any stumbling could cause severe ripples across the economy. The rise in 90+ delinquencies in credit cards and the high usage of credit cards as a means of payment in this higher rate environment is an important metric to be sure of and one we continue to track. Where this moves from here should provide clues as to what path we are headed down economically. We continue to feel a slowdown in the economy is a near-term issue and have positioned ourselves in a manner to mitigate some of what we feel will ripple from it. That outlook presupposes that while we expect some credit market missteps and credit widening, the downturn will not be a full-blown meltdown. Nevertheless, any indication of a change in this near-term expectation will provide us insight into just how detrimental it will be.

We continue to take the viewpoint that near-term credit deterioration is a possibility and, as such, continue to be conservative in our outlook on credit, preferring to be in higher credit quality names, which also exhibit high degrees of liquidity and provide diversification benefits within the overall portfolio. Situations, measurements, and data like the above provide us further evidence to that effect and reinforce our need to remain nimble and focused on the investment thesis. Of course, if the situation worsens, there is a probability that this also will lead to opportunities down the road to be taken advantage of to lock in overperformance once the moment of credit stress begins to fade. And that, too, requires us to position ourselves with enough dry powder to move on that opportunity. The consumer has undoubtedly spent the last year plus during this rate hike cycle gorging and spending like a first-time trick-or-treater. The question is, have they done so much that it might cause a stomachache for the overall market?

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

Home Equity Line of Credit (HELOC) - A home equity line of credit (HELOC) is a line of credit that uses the equity you have in your home as collateral.

Government-Sponsored Enterprise (GSE) - A government-sponsored enterprise (GSE) is a quasi-governmental entity established to enhance the flow of credit to specific sectors of the U.S. economy. Created by acts of Congress, these agencies—although they are privately held—provide public financial services.

Qualified Mortgage (QM) - A qualified mortgage is a mortgage that meets certain requirements for lender protection and secondary market trading under the Dodd-Frank Wall Street Reform and Consumer Protection Act, a significant piece of financial reform legislation passed in 2010.

Trust Preferred Securities (TruPS) - hybrid securities issued by large banks and bank holding companies (BHCs) included in regulatory tier 1 capital and whose dividend payments were tax deductible for the issuer.

Control #: 17614091-UFD-11/16/2023