“Sittin' in the mornin' sun

I'll be sittin' when the evenin' comes

Watching the ships roll in

Then I watch 'em roll away again, yeah”

- Otis Redding

The end of summer seemed to come at us pretty fast. Maybe it’s wishful thinking that it will slow so I can enjoy it more. But end it did. During this past month, the markets were quiet as vacation mode settled in. There was limited primary activity, and the secondary markets seemed subdued. Everyone seemed to put an “out fishing” sign on the door and hit the beach. Sitting on the beach promises all sorts of relaxation. It doesn’t seem hard to forget about things as one sits in the sand and watches the waves roll in. This year, though, there was a slight departure from what I remember from years past. There was a bout of strange weather all around us. In the far west, Hawaii, we had the headline-grabbing fires. On the East Coast, the end of Summer seemed more like Fall. Distorted by the tail end of some tropical storms, the weather was cool and windy, and the ocean loudly dangerous. Dangerous enough that rip tides and lost swimmers became a topic of conversation. It struck me that it was a quick reminder that sometimes you can stare out at something seemingly quite soothing, but underneath the surface lurks something so perilous.

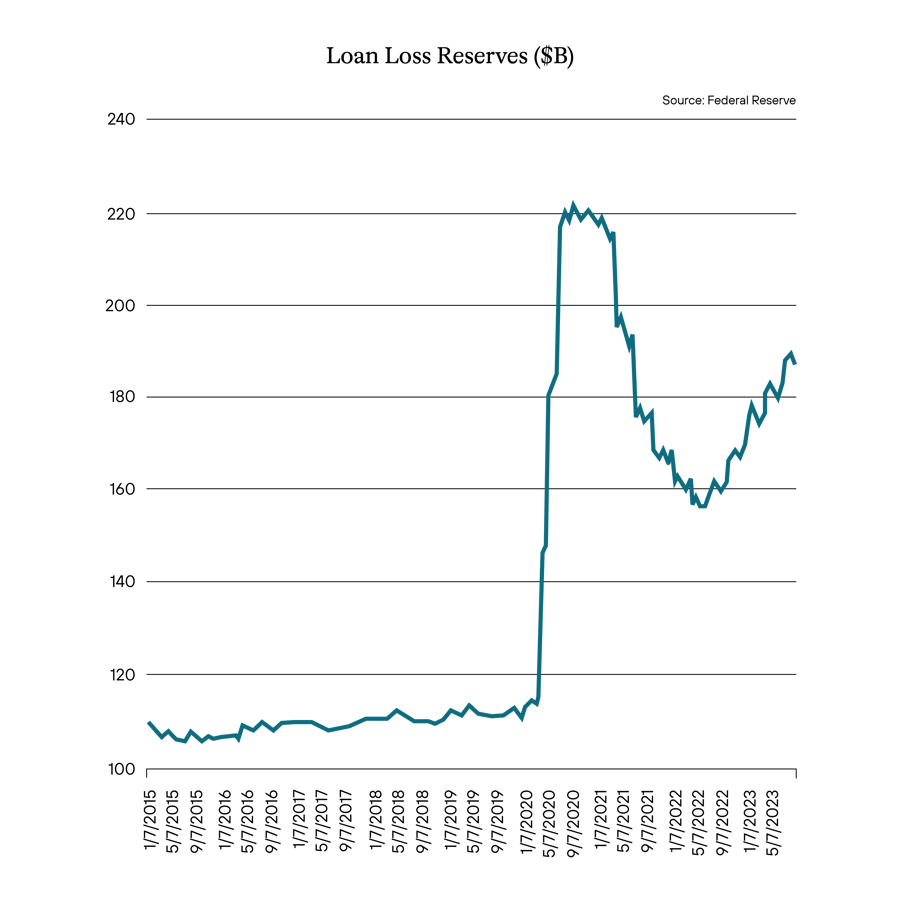

We are waiting for low tide, so to speak, for corporations, especially those that are sub-investment grade in terms of credit quality. There are examples all around us. Many noteworthy headlines hit the summer months, and maybe many didn’t notice them at the time, but they are piling up. Numerous articles are swirling about detailing how many defaults globally we’ve been seeing. Indeed, we apparently have witnessed in the first six months of 2023 as many defaults as the total number we saw for all of 2022. And there are less than subtle signs that many banks expect things to worsen. The Financial Times mentioned that domestically, six of the largest banks, such as JP Morgan, Bank of America, Citigroup, Wells Fargo, Goldman Sachs, and Morgan Stanley, are expected to have written off a collective $5 billion in defaulted loans. Those same banks are setting aside an additional $7-plus billion in terms of loan loss provisions. Indeed, as illustrated below, as per the Federal Reserve, loan loss reserves have been steadily climbing since the beginning of the year, an indication of expected losses and a future environment defined by weak performance and credit.

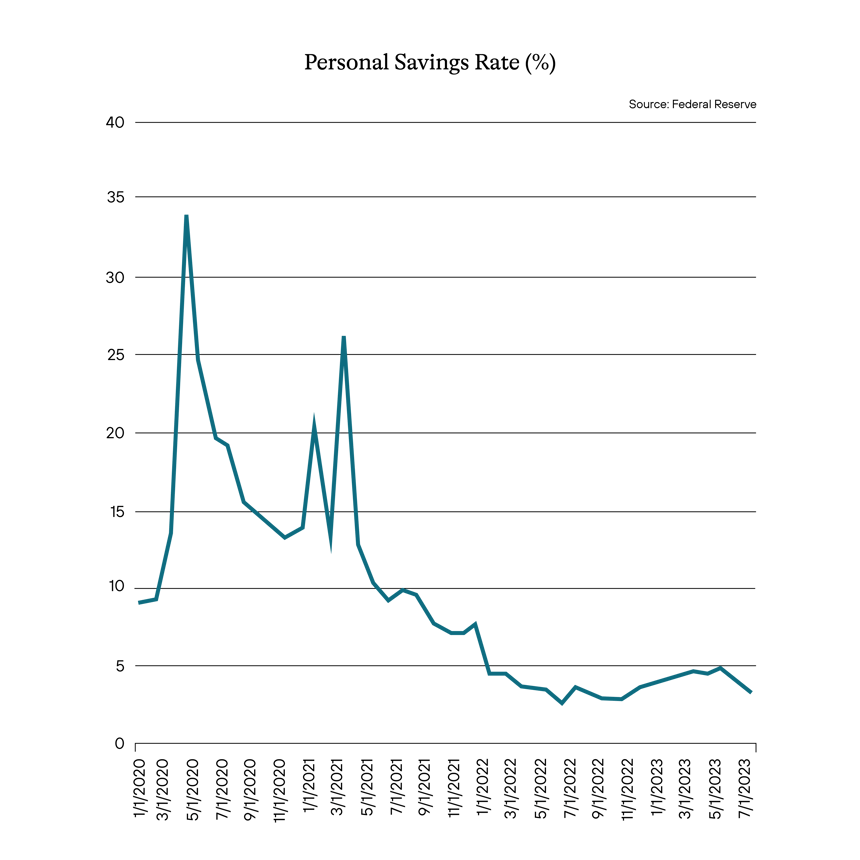

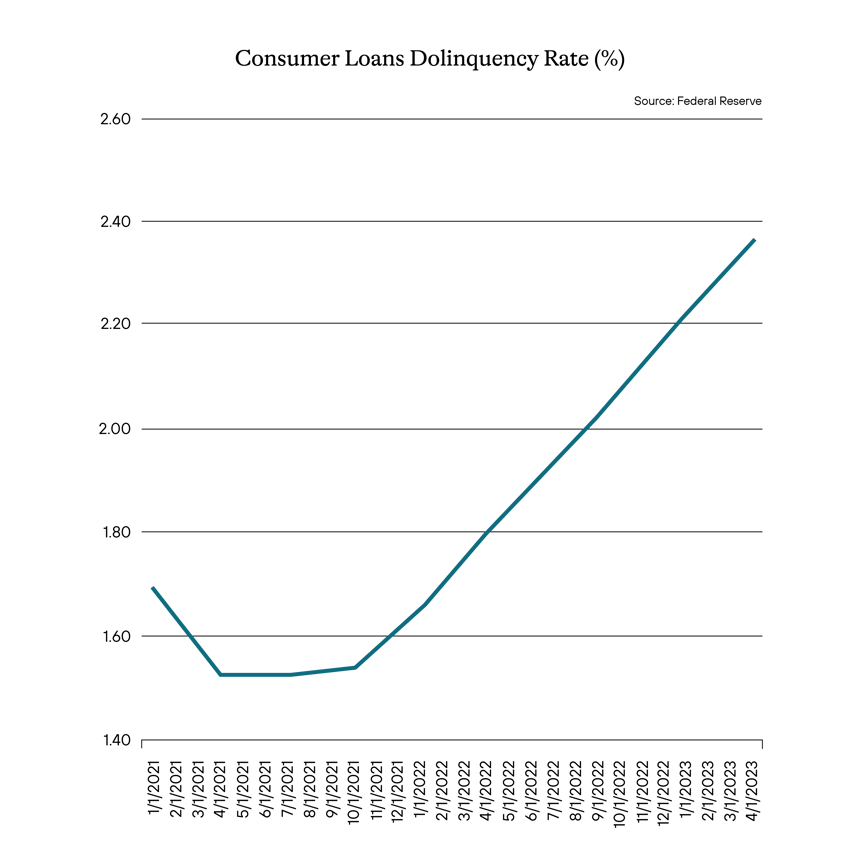

Much of the pressure building in businesses can be attributed to rising interest rates. Incremental increases in financing costs can lead to credit strains, especially for firms at the lower end of the credit spectrum. These firms don’t typically have a great deal of flexibility and funding options, so for the few opportunities they have, pressure in terms of increased funding costs can lead quickly to their inability to be an ongoing concern. The increased rates can also ultimately have a bottom-up approach regarding credit issues as the consumer starts to falter. We have touched upon it recently, but the consumer does appear to be having some problems. There is anecdotal evidence the consumer, while not slowing down just yet in terms of spending, is tapping other sources of liquidity to continue to do so and has sourced these alternatives given that they have now depleted the savings they built up during the pandemic.

This effort to keep spending is causing a strain on the consumer. A weak consumer and higher delinquencies at that level will ultimately funnel up to the business level in terms of operating strength or weakness, either through the direct consequence of loan losses or the indirect result of a consumer stepping back from spending, leading to a negative shift in those corporations’ health.

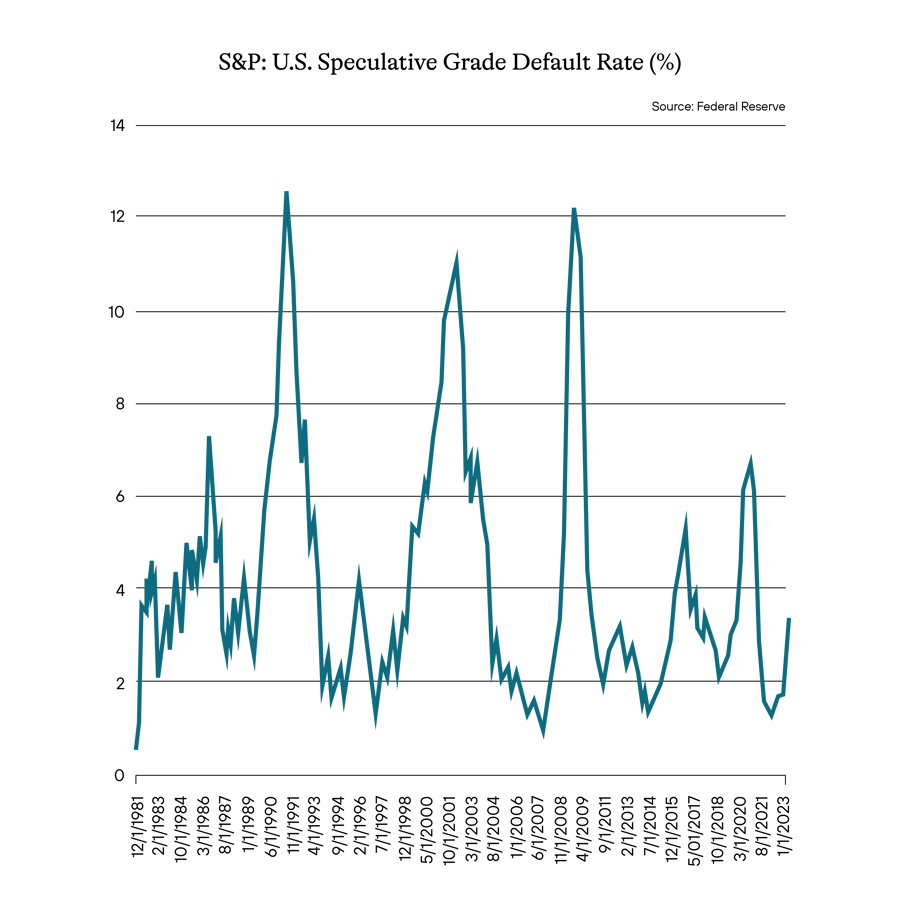

High-yield corporations are feeling the pinch. The default rate is climbing. With a historical average default rate considered to be around 4.1%, Fitch has indicated they expect the year-end default rate to approach about 5.0%. Moody’s has it at about 4.6%, but also considers 5.0% a likely landing spot, maybe around the first quarter of 2024. S&P, on the other hand, has published a report that indicates their base scenario is around 4.5%, with a pessimistic scenario or worst case of about 6.25%. However you stack it up, as illustrated below, defaults are rising and are expected to continue to do so. Given the data and in our opinion, we are not looking at solid near-term performance for sub-investment grade credits.

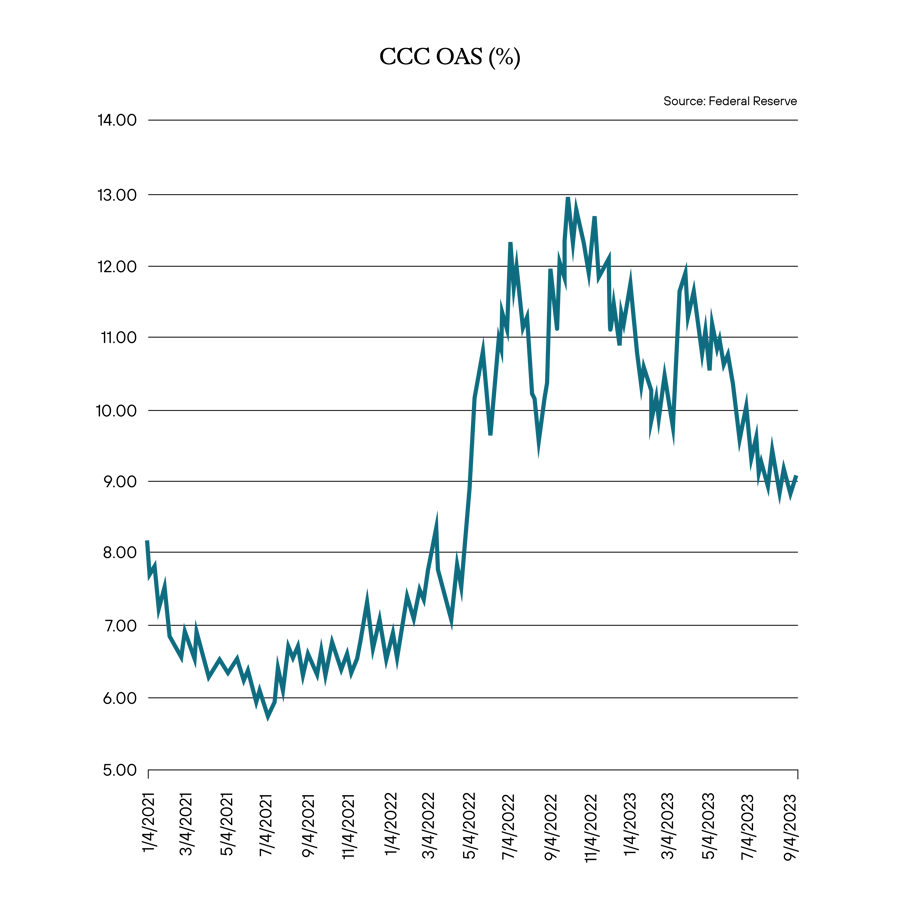

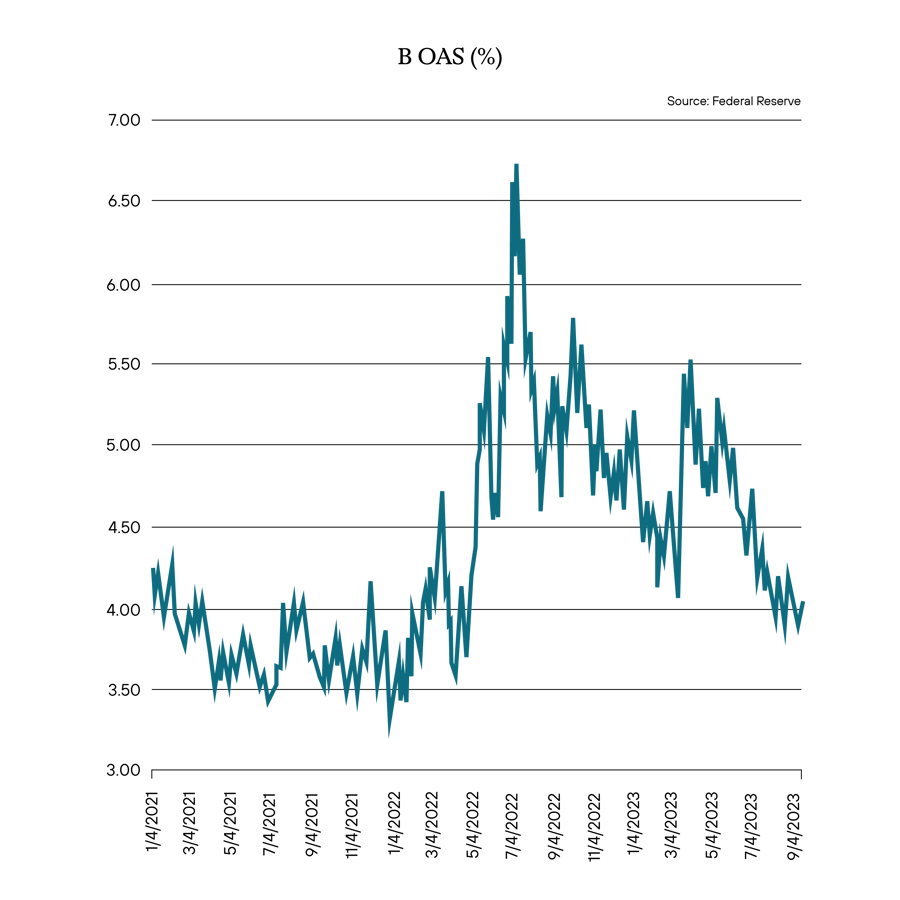

As of right now, the bond market seems to be shrugging all of this off. As a result, currently, credit spreads on the lower end of the sub-investment grade space would appear to be rich. That is, they seem not to be appropriately anticipating the near-term fallout of the credit issues seemingly building in the financial system. As illustrated below, the Option-Adjusted Spread (OAS) for CCC and single B credits, are going the exact opposite direction one would expect from the data above. And while credit spreads haven’t retraced back to the salad days of the post-pandemic environment, where capital and demand were cheap and abundant, credit spreads at the end of August 2023 continue to march in tighter. Indeed, they are now some 300 basis points (bps) tighter for CCC credits and around 150bps tighter for single B credits, respectively, than just a year prior.

The disjointed response of credit spreads to what is currently occurring in the financial markets – banks’ increasing loan loss reserves and the current rate market – would indicate that there will be some pain down the road for investors still buying into this level of credit. Simply put, it would seem the current reward is not correctly reflecting the expected ultimate risk. For us, it clearly indicates some tail risk is still buried in sub-investment grade corporate credit spreads. Furthermore, there is a possibility that given the compression going on at the lower end of the corporate credit food chain, even if you feel credit is reasonably priced at the higher ends of the credit spectrum, the widening that seems sure to occur at the lower end will ultimately create a ripple effect that potentially could reach the higher lots of the corporate credit sectors. Indeed, it’s a moment to take a step back and consider just how dangerous that riptide might be.

We remain incredibly focused on segments, sectors, and issuers in the corporate space. Anticipating that there is sure to be some credit widening in the near term has us preferring specific segments and issuers over others and investment grade over sub-investment grade exposures, based on how we have historically seen those targets perform in similar stressed or at least strained credit environments previously. Having a consistent but persistent outlook in environments such as this and not falling into the habit of joining the herd will ultimately mean an opportunity to capture overperformance in the near term. Better yet, once the widening does occur, revisiting those sectors that felt the wrath of a sudden drop in investor participation and overcorrection also means future opportunities will be available in the space once expected scenarios play out. Consistency and patience in these types of moments can help build a foundation for overperformance in the future. The trick is to wait for the tide to go entirely out and see what is lurking below.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

Home Equity Line of Credit (HELOC) - A home equity line of credit (HELOC) is a line of credit that uses the equity you have in your home as collateral.

Government-Sponsored Enterprise (GSE) - A government-sponsored enterprise (GSE) is a quasi-governmental entity established to enhance the flow of credit to specific sectors of the U.S. economy. Created by acts of Congress, these agencies—although they are privately held—provide public financial services.

Qualified Mortgage (QM) - A qualified mortgage is a mortgage that meets certain requirements for lender protection and secondary market trading under the Dodd-Frank Wall Street Reform and Consumer Protection Act, a significant piece of financial reform legislation passed in 2010.

Trust Preferred Securities (TruPS) - hybrid securities issued by large banks and bank holding companies (BHCs) included in regulatory tier 1 capital and whose dividend payments were tax deductible for the issuer.

Control #: 17385017-UFD-9/14/2023