“I would rather sit on a pumpkin and have it all to myself, than be crowded on a velvet cushion.”

- Henry David Thoreau

As we finish the first month of the new year, I can’t help but think of my favorite holiday of the year, Thanksgiving. Is it too soon to be talking about Thanksgiving? Or maybe too late? I like Thanksgiving for a bunch of reasons, but mostly because I am fascinated by Black Friday. Highly entertaining. Who hasn’t watched a news report on Thanksgiving Day as a reporter breathlessly described the scene outside a Best Buy, detailing how our friends and neighbors have pitched tents and begun to line up, waiting to storm the doors once they open so they can save 15% off at giant TV? Or better yet, the battle for a position like a power forward in the NBA hunting for rebounds outside a Walmart so they can get this year’s version of the Tickling Elmo? Sometimes I watch the videos of when those doors open, and it reminds me that maybe we really aren’t that advanced as a society—still just hunter-gatherers, albeit with more supportive footwear.

I bring this up because I was getting Black Friday vibes in the fixed-income market in January. The overall fixed-income market, primary and secondary, pretty much slowed down at the end of last year. While we witnessed a massive rate rally heading into the year’s end, we didn’t see a robust amount of primary issuance, and secondary trading was limited to need only, not necessarily opportunistic buying and selling. Indeed, there was a fairly muted amount of trading as investors seem to prefer locking in performance and a “we’ll get them next year” approach to trading. So it was a bit of a surprise when the new year started, and it seemed like I was watching the doors at the Sarasota Pamida open on a Black Friday in the fixed-income arena. Not only have we seen a plethora of transactions hit the market, but we are seeing the issuance matched with a type of demand that can almost be described as a frenzy.

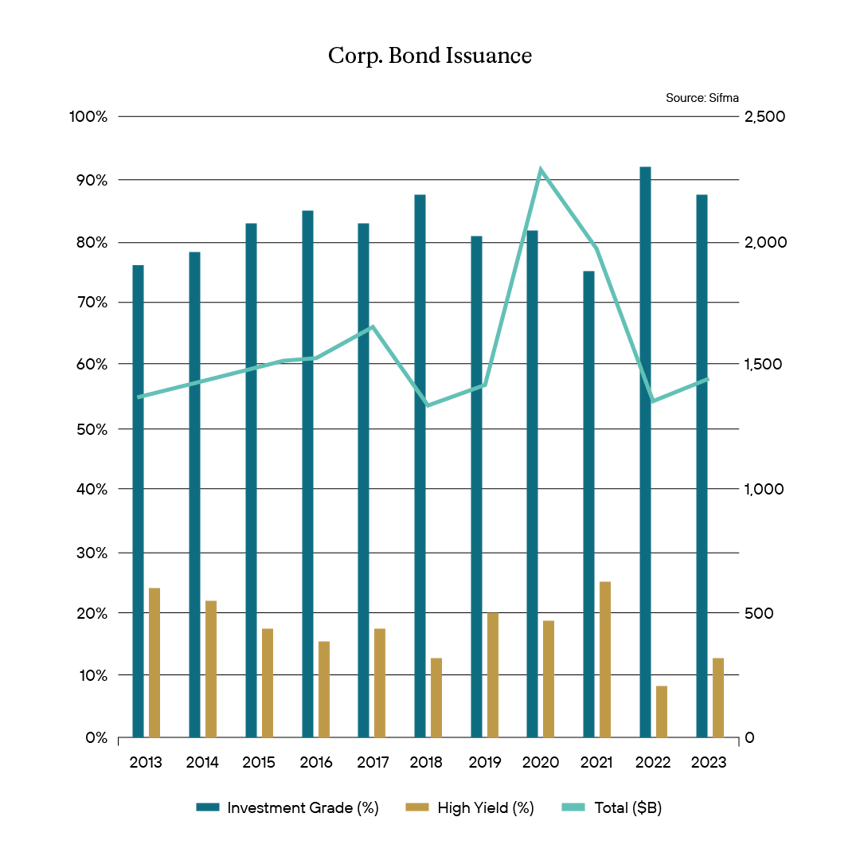

For corporate bonds, issuance in 2023 continued to be a far cry from the historic highs seen in 2020. Instead, it was just a continuation of the drab results of 2022, which itself was hampered by the initial foray of the Fed embarking on its rate hiking mission. As illustrated below, there was little difference between 2022 and 2023, as the total amount of issuance was at or near the ten-year lows last seen in 2018. In 2023, total corporate issuance, as reported by Sifma, was $1.4 trillion, which is far closer to the ten-year low of $1.3 trillion reported in 2018 than the 10-year high of $2.3 trillion reported in 2020.

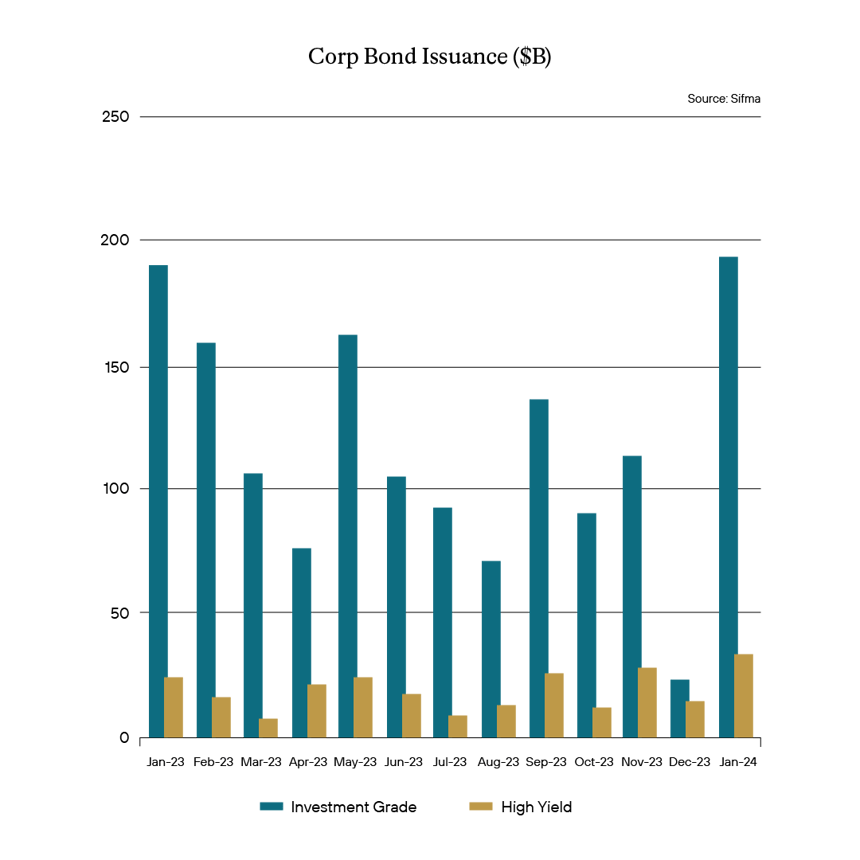

However, the doors have been open since the beginning of this new year! Doesn’t matter either what is on the shelves, with both investment grade and high yield issuers taking part and total issuance reported at some $223 billion. In fact, the $191.3 billion and $31.4 billion amount of issuance for January, for investment grade and high yield, respectively, were 13 months highs.

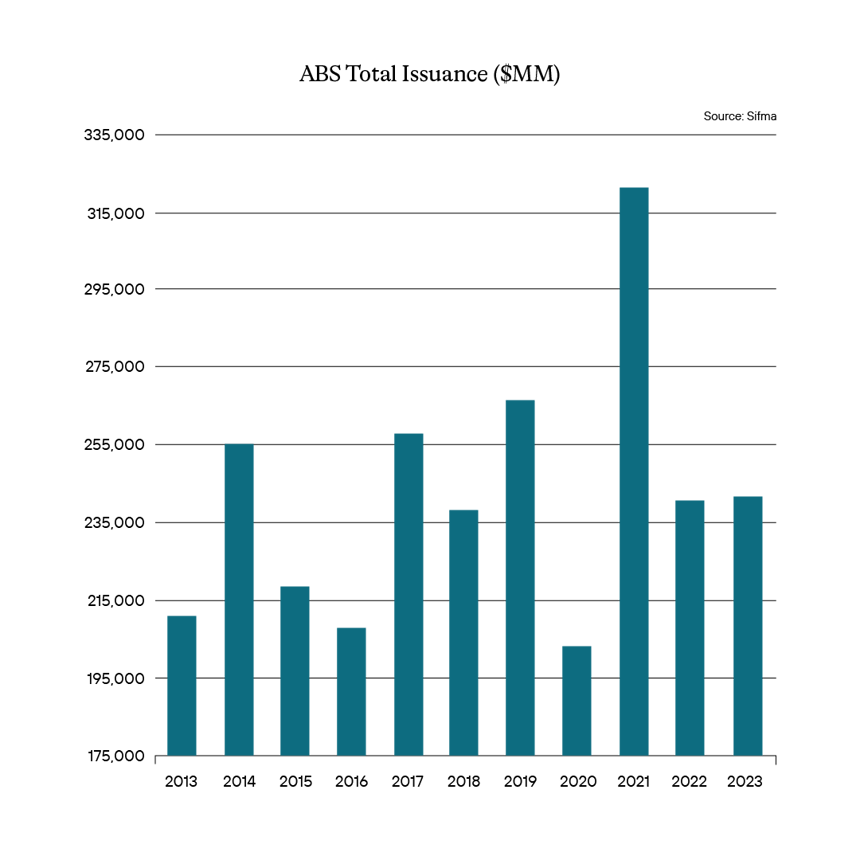

For the asset-backed securities (ABS) market, the story was similar. Total ABS issuance for 2023 was reported by Sifma as $239.3 billion, which was far closer to last year’s dismal $238.7 billion than the salad days of 2021, when $319.4 billion was recorded.

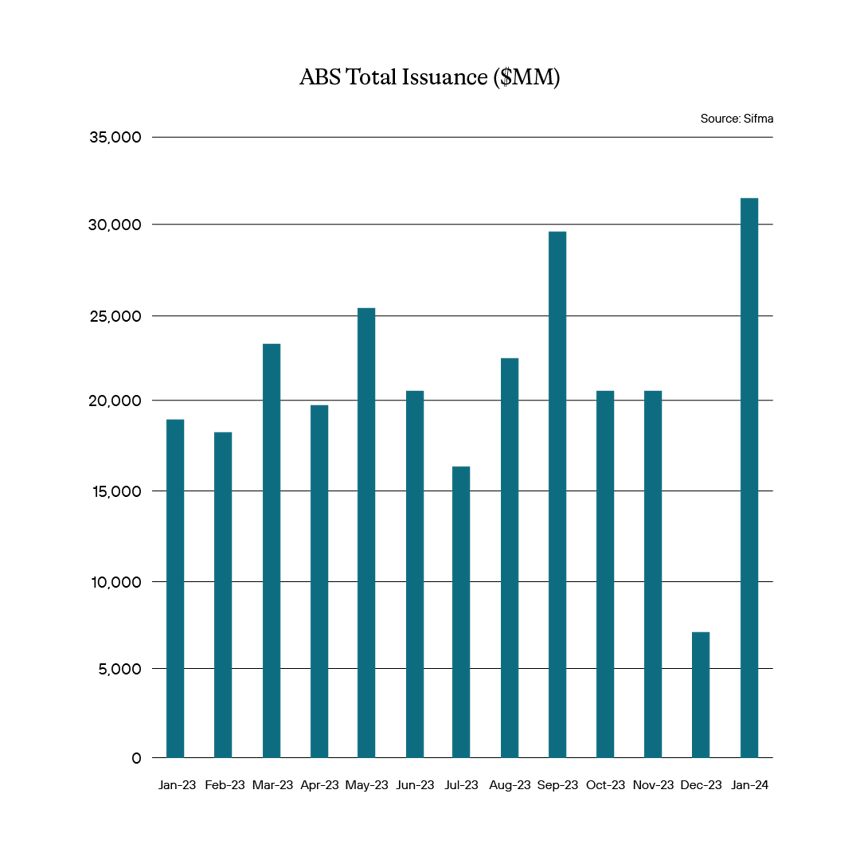

But that shifted dramatically once the calendar turned over, and suddenly, we were exposed to numerous deals of all different asset classes, including the plain vanilla of auto ABS and equipment leasing and the unusual, such as music royalties and rate reduction. And the $31.2 billion reported in January of 2024? Well, that too was a 13-month high in terms of issuance.

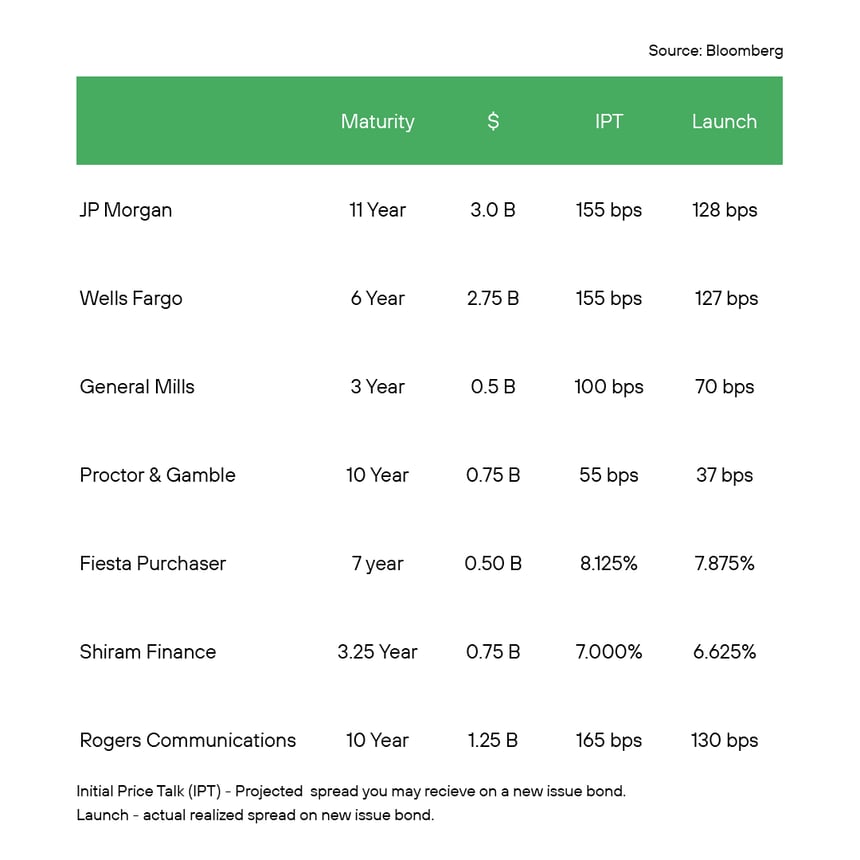

As heavy the issuance was, apparently, it wasn’t enough. The investor base that had sat on the sidelines going into the end of last year suddenly couldn’t wait to spend some money. There was seemingly insatiable demand, with deals oversubscribed, sometimes massively so. Routinely the market would see books for $1.0 billion deals being over eight times oversubscribed. On the ABS side, tranches or classes in each deal routinely were eight times to 16 times oversubscribed. The massive demand meant dealers and issuers were in the driver’s seat. Dealers were able to drive spreads in and launch deals at much tighter levels than they were announced at, meaning investors were constantly giving up pricing concessions just to get allocations at a percent of their initial orders and allowing issuers to price tighter, saving themselves significantly on funding costs. Below are just a few samples of what we have witnessed during January.

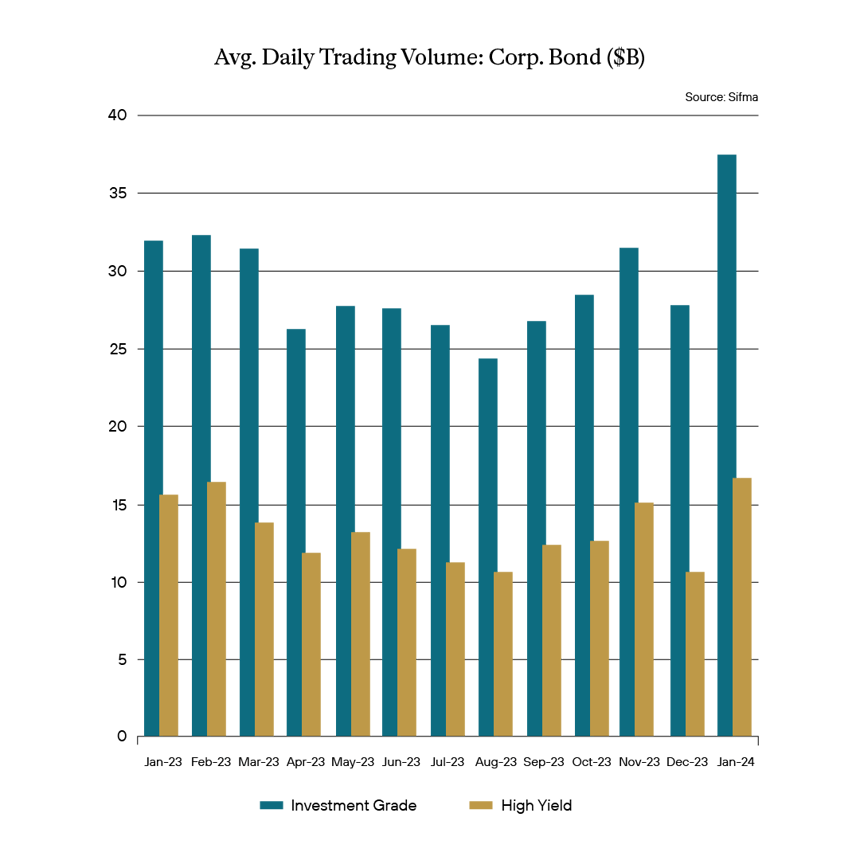

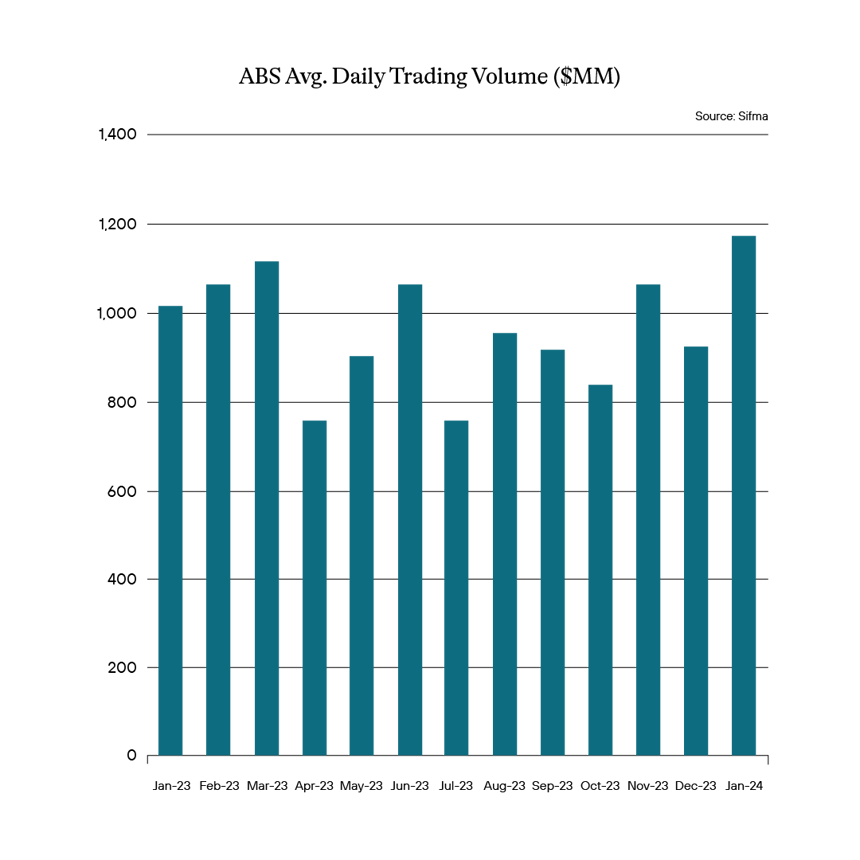

The explosive issuance in the face of this heavy investor demand in the primary market created a renewed interest in the secondary market. Investors who got shut out of new deals or simply had muted allocations turned to the secondary market to trade into the newer deals or perhaps looked for older, more vintage deals to get the same issuer exposure. That included both the corporate market and the ABS market. As a result, corporate bond trading in the secondary market in January 2024 dwarfed what was witnessed in the previous 12 months, coming in at $53.1 in average daily trading volume (ADV), according to Sifma. For ABS, the ADV for January 2024 was reported as $1.2 billion, the highest for the past 13 months.

The heavy issuance met by excessive demand is certainly something to ponder. The market is certainly feeling pretty grabby. The inclination is to join the hoard, but there is something to be said for walking around the pile of bodies at the just-opened doors. The danger in a moment like this is to get too aggressive and get caught up in the moment. Worse, these are the moments that can lead to investors reaching further down the credit stack as they try to get fully invested. And as we have seen, reaching never turns out the way you imagine it will. As we have noted, Spreads on the corporate side seem pretty tight already. On the other hand, ABS remains a bit wide but is tightening more and more through each deal cycle. Nevertheless, overall yields remain high, given that although the Fed has paused, we still are waiting on our first rate cut. All of that means there is value to be had if one can be discerning and not just reach for anything and everything on the shelves.

Investors seem like they are in a hurry all of a sudden. These are the moments to take a step back and remain true to your investment targets. There remains great value and opportunities in this market, but avoiding the masses and staying to the investment thesis may ultimately provide the overperformance you are seeking. The upside to this increased demand and activity is the level of liquidity afforded to those who want it. Thus, we find it an advantageous moment to sell into it, giving us an opportune time to prune exposures we feel have reached targeted values, and move into more favorable targeted sectors and issuers. We continue to stay focused on our targets and ignore the rush that some of our competitors seem to be embracing. Once the fever breaks, we feel there is a real concern that risk reprices in a negative fashion and as such prefer the higher ground. Slow, steady, and focused on our investment thesis is how you keep the noise out of the portfolio and use this moment to continue building selectively toward targets and potential future overperformance.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

Home Equity Line of Credit (HELOC) - A home equity line of credit (HELOC) is a line of credit that uses the equity you have in your home as collateral.

Government-Sponsored Enterprise (GSE) - A government-sponsored enterprise (GSE) is a quasi-governmental entity established to enhance the flow of credit to specific sectors of the U.S. economy. Created by acts of Congress, these agencies—although they are privately held—provide public financial services.

Qualified Mortgage (QM) - A qualified mortgage is a mortgage that meets certain requirements for lender protection and secondary market trading under the Dodd-Frank Wall Street Reform and Consumer Protection Act, a significant piece of financial reform legislation passed in 2010.

Trust Preferred Securities (TruPS) - hybrid securities issued by large banks and bank holding companies (BHCs) included in regulatory tier 1 capital and whose dividend payments were tax deductible for the issuer.

Control #: 17901686-UFD-02152024