“The only thing worse than being talked about is not being talked about.”

- Oscar Wilde

Another year in the book. The year closed as most do in the investment arena with a busy first half of the month, followed by two weeks of a lack of urgency to do anything as managers try to lock down performance. Plenty of time to revisit strategies, review results, and, worse, perhaps, self-reflect. It’s at that moment when it dawns on you that there are but a few days left in the year to make last year’s New Year’s resolutions a reality. It’s a quick calculation revolving around motivation and time. How much time do I actually need to train for and run a marathon? Do I actually have the right shoes to hike up the side of Everest? Will Lowe’s have the necessary materials to finish that giant home improvement project? And if I do all that, will I still have time to lay on the couch and complain about a holding call between two collegiate teams in a bowl game I’ve never heard of and whose teams I have zero connection to? As it turned out, sadly, I only had time to really focus on the last one. Ah, well, there is always next year.

One thing that has changed over the years with regards to New Year’s is we don’t seem to see lists anymore. When I was younger, they seemed everywhere. A year in review, top 10 things we should look for, etc. One of my favorites growing up was getting lists of people’s predictions of what was going to occur over the next year. I don’t see those anymore. The goal, it seemed back then, was to be as outlandish as possible in the hope that something obscure would occur and you could take credit. No one remembers the practical as much as they do the obscure. But times are different. These days we are far more fascinated with today. Who needs to think about what might occur a year from now when social media oozes with the bizarre and outrageous happening right this very second? Tough to compete.

For better or worse, or it is more of a statement about my age, below is a list of things we are looking at. A focus list of some of the ongoing themes for us. There doesn’t seem to be anything quirky about what we are seeing. Indeed, the current market seems to be one where you don’t have to be overly aggressive. Instead, it is an environment where you can be rewarded simply by taking what the market will give you. It strikes us as a market where there is no particular need or reward for being aggressive or reaching for the obscure. In fact, if we had to label it somehow, it would be: let’s focus on the obvious.

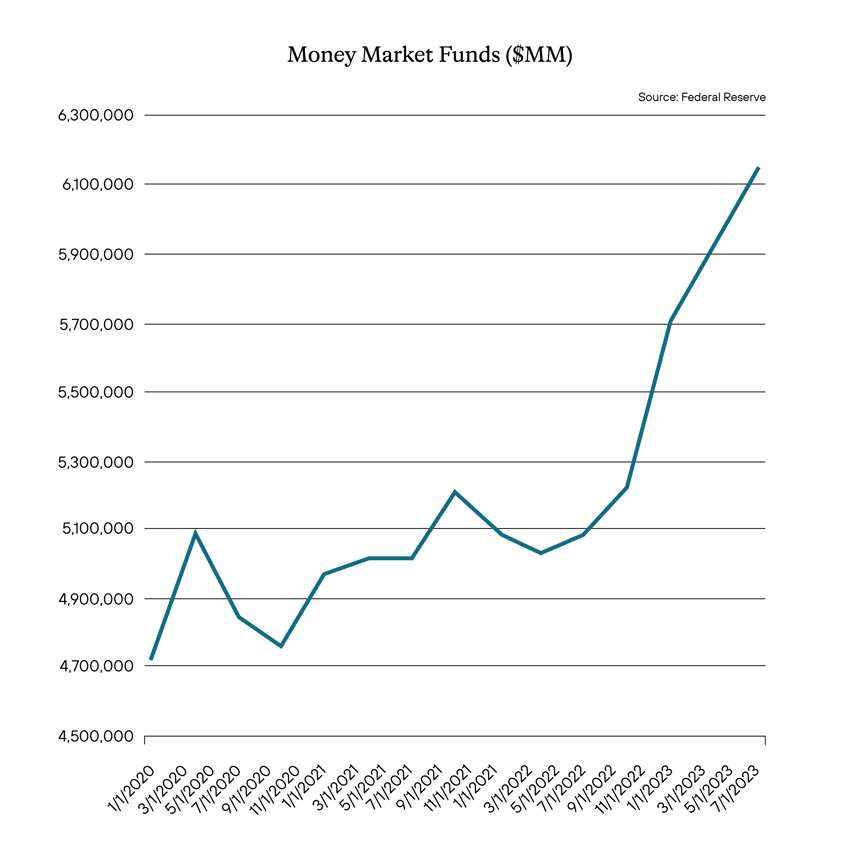

Money Market Funds AUM

The collective marketplace, at some point during the year, fully embraced money market funds (MMF) as if they were a long-lost cousin. Assets under management (AUM) for these funds have never been higher. Total AUM, when considering the credit funds, government, and treasury, topped $6.1 trillion. The MMF industry is rejoicing. Well, kind of. They certainly like the fees they are generating. But MMF managers are equally on edge. MMFs are not typically a place you park money in as a long-term investment strategy. It’s usually a rest stop, a place to hang out and wait to redeploy monies later for more lucrative strategies. And it’s not like the industry doesn’t know that. And that is a concern for the industry. Investment shops that have large MMFs love it when the AUM grows but are wary that as fast it comes in, it can leave just as fast. That should be a concern for everyone. Given those funds more or less all invest in similar securities and tenors, it can be a tough market to have to sell into if you are in a hurry because you will likely find everyone else in the space is selling at the same time. And as we have seen, any sort of liquidity ripple in this arena can cause larger waves in other areas.

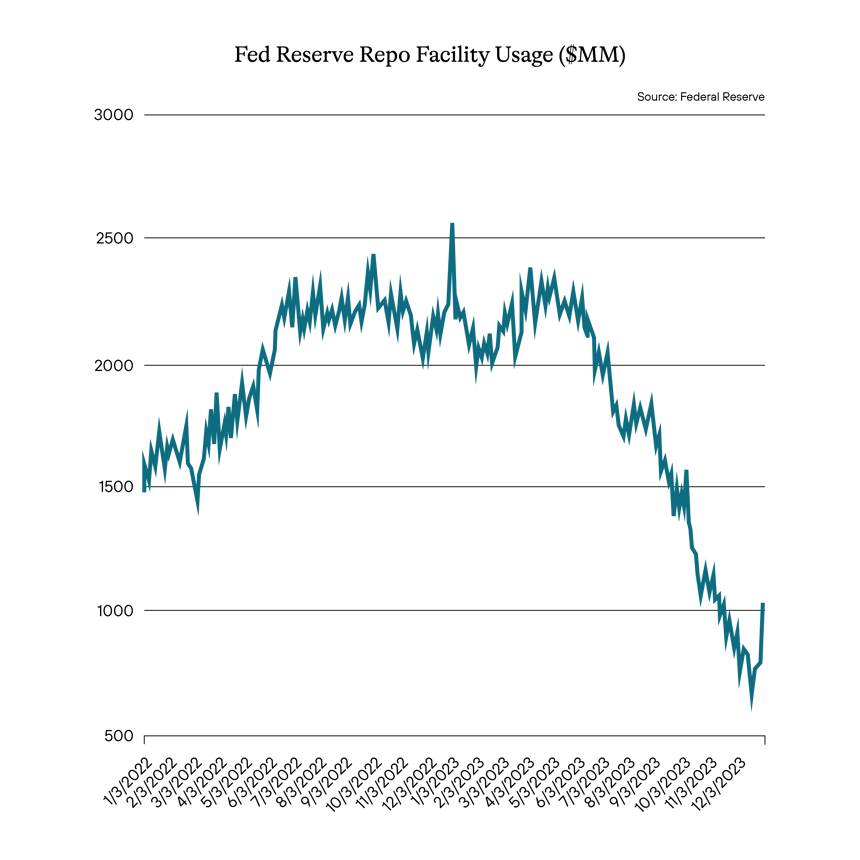

Right now, MMF managers are living in the moment. Furthermore, they seem to be trying to hold onto that AUM as long as they can. Below is a chart for the usage of the Fed’s reverse repo facility. One can see usage has continued to drop. MMFs have historically been big users of the facility as it allows them to park cash and meet the onerous investment requirements as spelled out in the governing rules for MMFs. The drop in usage most likely means that MMFs are reallocating the money to other instruments.

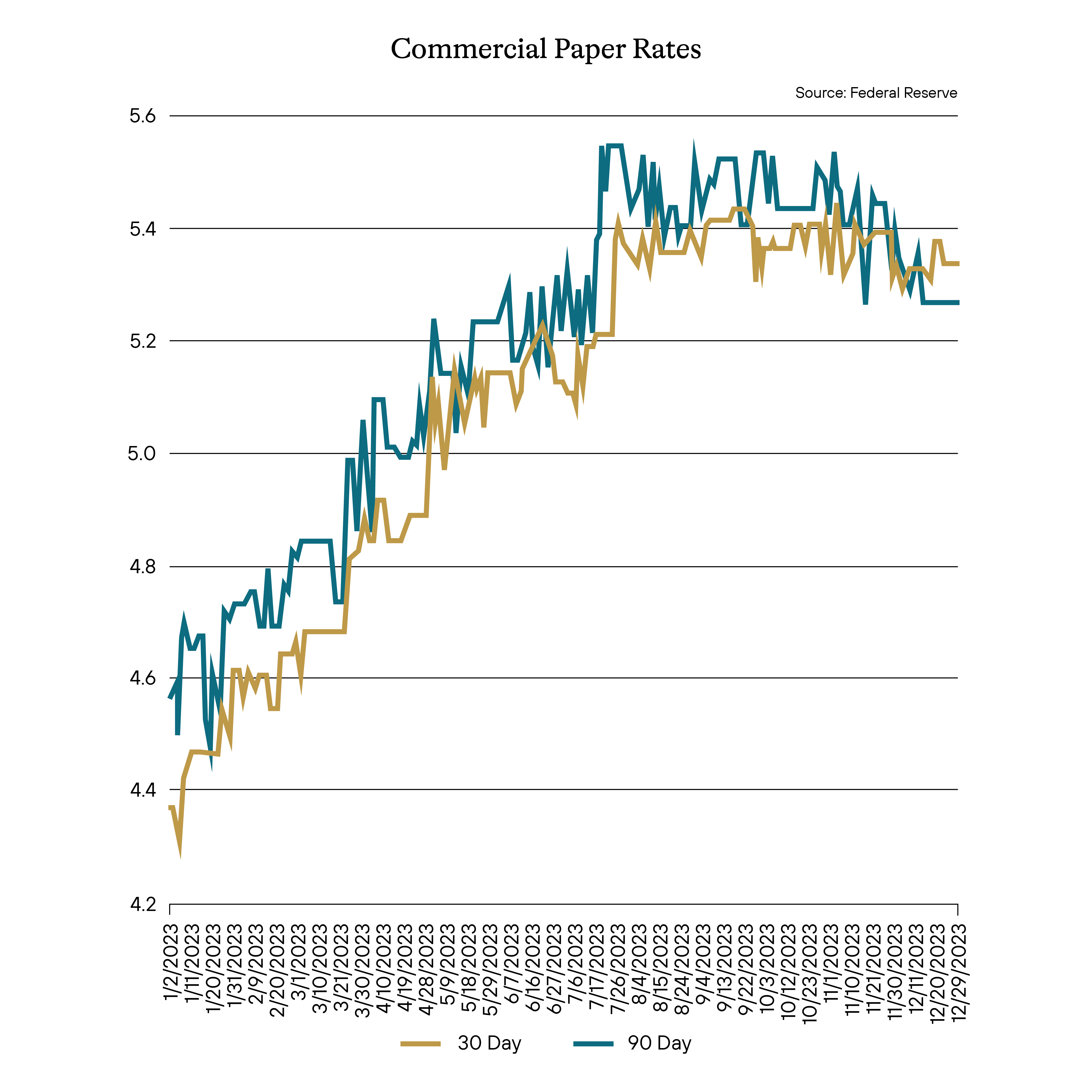

Why would they do that? To attempt to appear to be attractive to investors for as long as possible. The reverse repo facility is, for the most part, a place for overnight risk. And if rates start to get cut, it will be the first place to feel it. So, assuming one can navigate around some of the boxes the investment guidelines require, you push the money into other areas. One area is commercial paper (CP). Below is a chart illustrating the yield difference between investing in 30-day CP and 90-day CP. As of year-end, the 90-day CP rate is now less than that of 30-day CP. Most likely, a good part of that is that managers who still have some room to do so are attempting to invest further out in an effort to lock in a higher yield for longer. The demand, thus, is pushing rates lower further out. And as meaningless as it can be to managers who invest in longer tenor securities, for MMFs, 90 days is a lifetime, so the ability to lock in a higher yield for 90 days is worth it. It also reveals just how fast the yield on MMFs can drop once the cuts start coming and the incentive for managers to keep pushing out 60 days. All in an effort to keep that yield for just a little bit longer, appear to be that much more attractive to investors for a little bit longer, and keep the AUM for just a little bit longer.

Rest assured, the AUM on MMFs is due to drop and most likely pretty quickly once the rate cuts commence and yields on the funds fall as a result. We are paying attention to that for a few reasons. The speed of the AUM shifting could cause a near-term shortage in supply for longer-term investment options. When that shift into longer-term securities occurs, it could cause spreads to tighten, which would create a short-term lift in asset valuations. However, that also typically includes lower credit assets and tightening spreads, and it leads to some pain when or if credit later in the year suffers a hiccup. We also want to ensure that if the AUM drops too rapidly and creates an environment for selling for those funds, it doesn’t cause any sort of stress on the MMFs themselves. As we said, any sort of liquidity ripple on the front end tends to impact the shores of other areas later.

Short End Rates

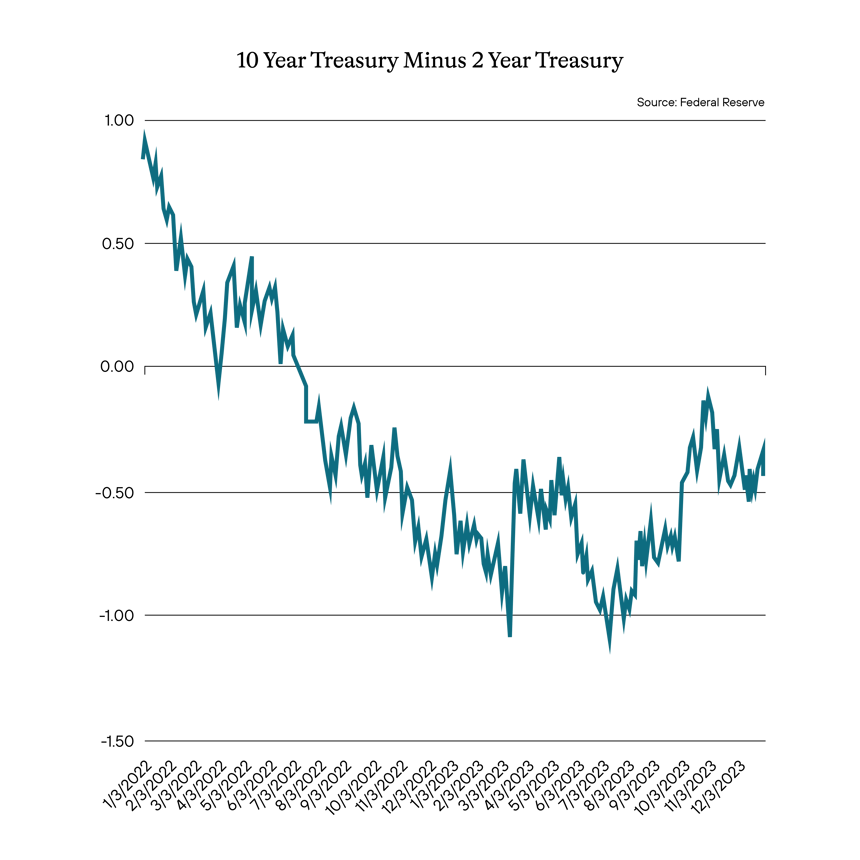

It’s been quite a rally for the 2-year treasury. In October 2023, it hit a 5.22% yield. By year-end, the 2-year treasury had rallied nearly 100 bps. The 10-year treasury yield moved in a similar fashion, if not more, rallying some 111 bps from its high in October 2023. There is still plenty of upside left in rates as we begin the countdown to the Fed pivoting from their aggressive rate hike program to rate cuts. Just as important, though, is where the upside is. Because as much as the 10-year treasury rallied, it hasn’t been enough to change the fact that the yield curve remains inverted between the 10-year and the 2-year. And because of that, in this particular instance, it would appear that while there does seem to be plenty of upside in rates overall, perhaps there is more upside in the 2-year.

We like the overall outlook for rates in terms of upside. But we are particularly intrigued by the value the short end of the curve seems to offer.

Credit Spreads

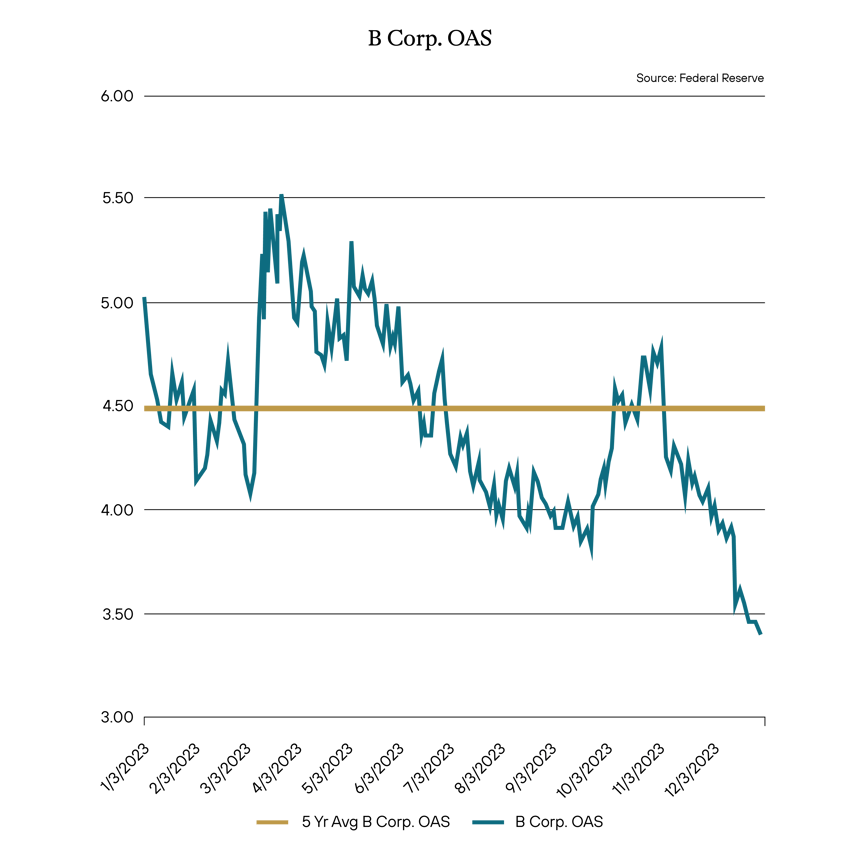

We discuss credit spreads a great deal for good reason. We continue to focus on whatever slowdown may occur in the economic environment as we go further into the year. Despite all the talk about a soft landing or a semi-soft one, the fallout from the higher rates over the past 2 years seems to us to have a significant tail risk attached to it, and we still are waiting to see full evidence of what that means structurally to the credit market. Additionally, based on the above, the sudden reversal in rates and reallocation of money market fund AUM and other cash equivalents could flood corporate risk markets with enough cash where yield will be chased at whatever level of credit one can talk themselves into. And yet, it is worth noting that corporate credit risk is already comparatively expensive.

As illustrated below, credit, in this case, single B corporate credit spreads are at recent tights and far below the level of spreads when compared to the 5-year average. This is true up and down the credit stack, although less egregious at the higher end. Indeed, it seems when compared to five-year averages, the further one goes down in credit, the tighter the spreads seem. If money floods this area, this will continue to tighten, making credit even more expensive. And that creates a dangerous condition in the marketplace where a lot of cash chases lower credit. In other words, getting paid far less for the risk taken than should be demanded, which history has shown us usually ends in pain.

We continue to prefer the higher ground. Over the past few months, we have stressed our outlook and preference for better credit and more liquid names. We continue to stay the course on this and remain focused on watching how the spreads move into the coming year.

We expect to see ample opportunities for overperformance over the next year. There are some concerns to remain vigilant about, chiefly the large amount of cash sitting on the sidelines waiting to be redeployed and what that ultimately means to asset prices and pressure on credit. Nevertheless, opportunities come in many packages, and even anticipating some bumps in credit markets will ultimately prove to create opportunities for targeted sectors and names. At the same time, current market conditions provide ample opportunities to create a foundation for future performance. We, therefore, remain focused on the obvious: take what the market is offering.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

Home Equity Line of Credit (HELOC) - A home equity line of credit (HELOC) is a line of credit that uses the equity you have in your home as collateral.

Government-Sponsored Enterprise (GSE) - A government-sponsored enterprise (GSE) is a quasi-governmental entity established to enhance the flow of credit to specific sectors of the U.S. economy. Created by acts of Congress, these agencies—although they are privately held—provide public financial services.

Qualified Mortgage (QM) - A qualified mortgage is a mortgage that meets certain requirements for lender protection and secondary market trading under the Dodd-Frank Wall Street Reform and Consumer Protection Act, a significant piece of financial reform legislation passed in 2010.

Trust Preferred Securities (TruPS) - hybrid securities issued by large banks and bank holding companies (BHCs) included in regulatory tier 1 capital and whose dividend payments were tax deductible for the issuer.

Control #: 17801469-UFD-01162024