“And when the night is cloudy,

there is still a light that shines on me

shine on until tomorrow

let it be”

- Paul McCartney

Not a big Beatles fan. I know you are supposed to love them, I just don’t. You might catch me singing along to one of their songs when it plays on the radio and I’m driving by myself, but I assure you it isn’t because I’m a huge fan. I’m just as likely to sing along to the Barry Manilow McDonald’s theme song; “You deserve a break today….” Doesn’t make me a fan. Just makes me another horrible singer eager to overcome boredom as I drive. Everyone tells me you’re supposed to be a fan. I even watched Peter Jackson’s Beatles documentary, truly appreciating the genius. How could you not be impressed by the creativeness? It doesn’t make me like their songs any more unfortunately; I’m just as happy when Jethro Tull hits the airwaves, maybe happier in fact. It does however remind me a great deal of how a herd mentality can develop and, in many cases, dominate an area of interest, even drive preferences.

There is a herd mentality pertaining to a lot of things around us. Music most definitely, financial markets as well. There is a sense that it is safer to be part of the herd than it is to step back and appreciate that maybe just perhaps we all don’t have to follow the same path. There are certainly other voices and a number of investment shops that don’t for sure, but the general investor (especially in times of distress) seems to default as a reflex to situations in a certain way….and that typically is one of follower. Of course, it’s easier to simply move with the herd. There can be a risk in being a lone voice against what seems an overwhelming sea of opposing thought. There are for sure going to be moments where that overwhelming majority is right. Being a contrarian for contrarian-sake can prove costly in many instances, but there are other moments when a simple step back and letting the parade ramble down the street without you is where value can be found.

Banks have been taking a beating over the past few months. Silicon Valley Bank (SVB) captured plenty of headlines, and there isn’t a whole lot to gain rehashing that failure. After they did fail, there was plenty of time to look for someone to blame; plenty of time to comb through the missed warning signs; and what becomes most important, assessing who might be next. Off we went. All over social media and the main street media were endless stories and speculation of not only who was next, but a rapid assumption that the whole sector was teetering. From there accumulated a barrage of targets that might be next. Short sellers came out in force and attacked, then came the ghosts of 2008.

The narrative started to become that we were revisiting the Great Financial Crisis (GFC) and were going to witness a parade of fallen banks. In 2008, it was a story of liquidity, or lack thereof, and credit. Broker dealers like Merrill Lynch, Bear Stearns and Lehman gorged themselves on short-term financing markets and claimed to have balance sheets filled with liquid assets. When the short-term markets stopped funding them, and their balance sheets turned out to not be so liquid, well that was that. Most notable was that that crisis became a top-down event. That is, we started at the bigger banks and slowly made our way down in size, stopping far above regional and community bank level. This was because it was the community banks, the regional banks, who didn’t have balance sheets filled with exotic failed assets like CDOs or over-exposure to sub-prime loans. At that level, they had clean balance sheets filled only with local lending exposures. It was the large banks with a bad mix of assets on their balance sheet and a wobbly capital base. This time around we are seeing the opposite; this time it is a bottom-up issue. This is a very important distinction that seems to be getting lost.

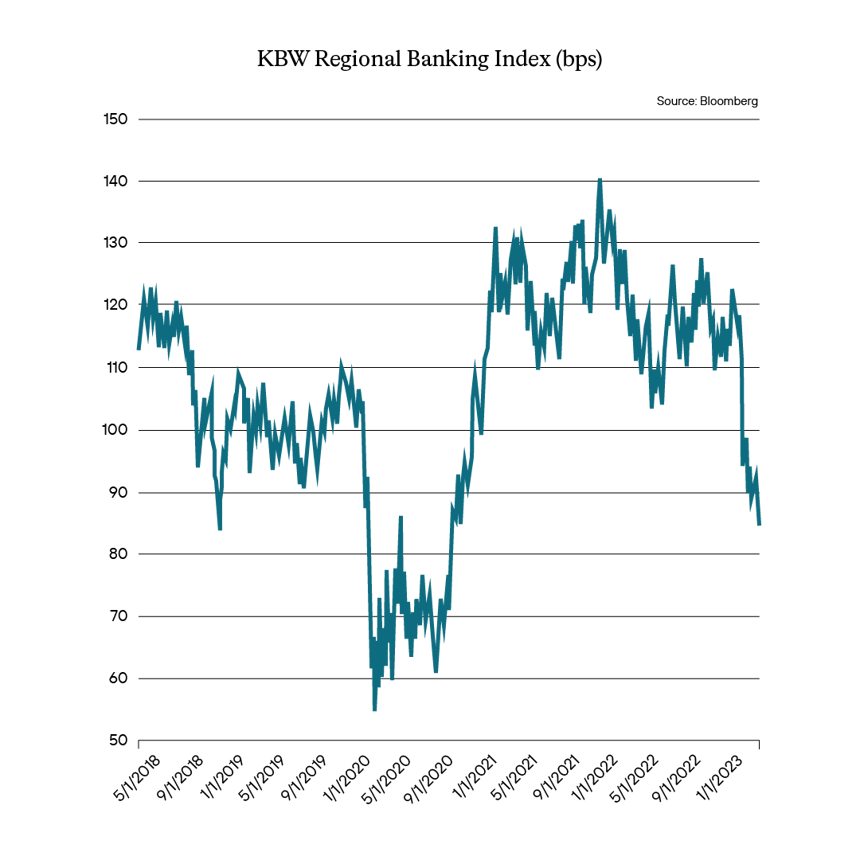

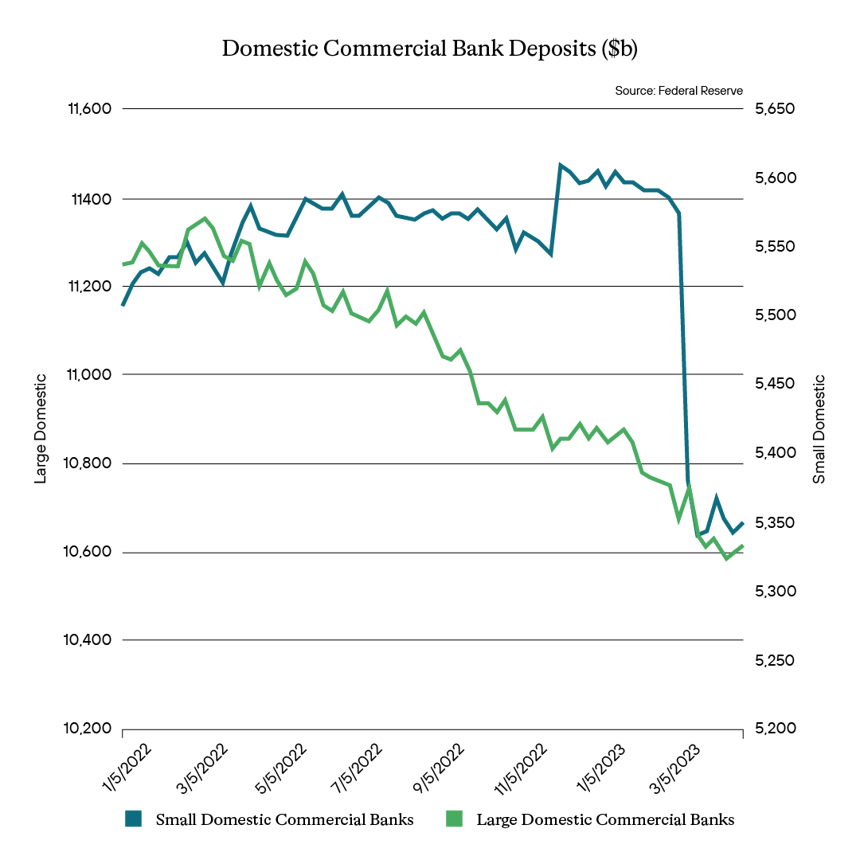

It's been quite a ride: Credit spreads blowing out, Short sellers armed with credit default swaps (CDS), routinely attacking one target after another. The result of the pressure and short sellers has been immediate and consequential. As illustrated by the KBW regional banking index, not since the early salad days of the pandemic have we seen quite a drop-off as we are witnessing now.  One of the data points paid attention to the most, especially with SVB, was the exodus of deposits which would signify a run on the bank. We are in the age of technology, so no longer do we get the video of people waiting in line for a week to withdraw their money. Now most can do so on their phone with the touch of a button. It’s instantaneous, making the speed of a run on a bank breathtaking in terms of velocity. Certainly, we saw that with SVB, and given their health in comparison, one would’ve expected to see smaller banks vulnerable to more deposits leaving than the big boy banks, such as Citi, JP Morgan and Bank of America. We looked at the deposits last month, and the deposits leakage at the smaller banks with some small amount of leakage at large banks is kind of what we saw. No real surprise.

One of the data points paid attention to the most, especially with SVB, was the exodus of deposits which would signify a run on the bank. We are in the age of technology, so no longer do we get the video of people waiting in line for a week to withdraw their money. Now most can do so on their phone with the touch of a button. It’s instantaneous, making the speed of a run on a bank breathtaking in terms of velocity. Certainly, we saw that with SVB, and given their health in comparison, one would’ve expected to see smaller banks vulnerable to more deposits leaving than the big boy banks, such as Citi, JP Morgan and Bank of America. We looked at the deposits last month, and the deposits leakage at the smaller banks with some small amount of leakage at large banks is kind of what we saw. No real surprise.

And yet, despite the current conditions indicating that we are in a moment of almost the exact opposite of what we witnessed in the GFC (where it was a top-down issue and this is more a bottom-up issue), what we are seeing is a general attack on the banking sector overall. That is, there is a herd mentality that all banks need to be victims to a credit spread widening. There is no selectivity, it’s an attack on the bank populace. Not only is it very important to take the time to differentiate the moment, but also to understand the reason for the moment. There is a very important lesson to glean from the deposits illustrated above. The smaller the bank, the more limited its funding options, the more it is reliant on deposits for a funding or lending base. A drop in deposits as seen above is devastating for small banks. But the larger banks have other avenues to fund themselves and their operations. The ability to tap other funding sources, and ultimately be a safe haven for depositors fleeing the smaller weaker banks, by itself should create a tier of comfort. That isn’t what we are seeing.

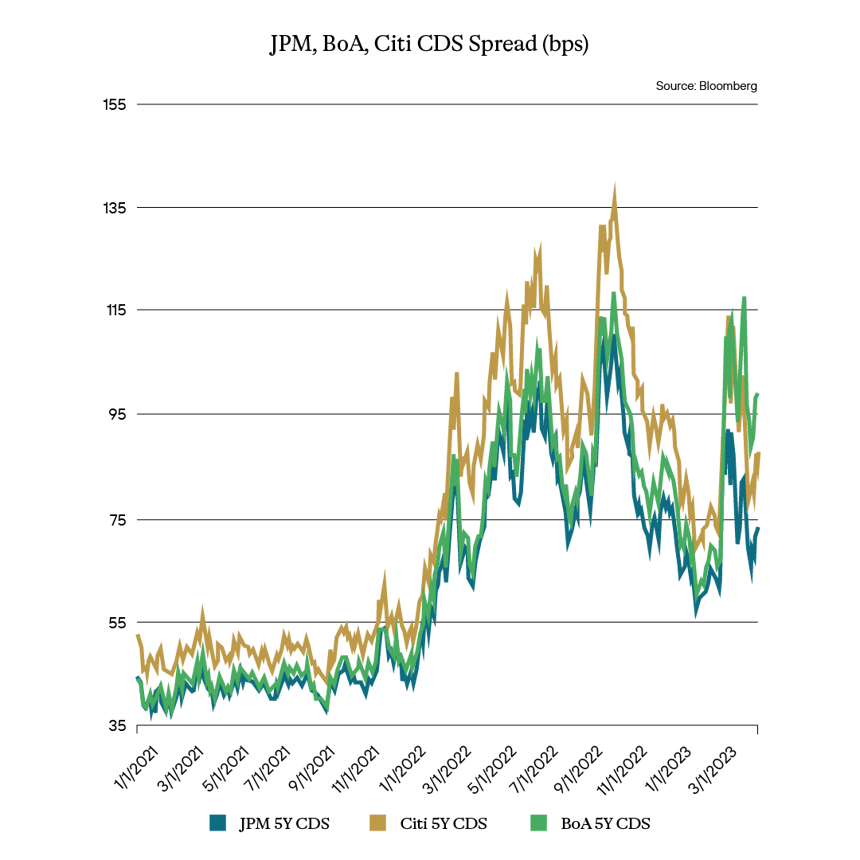

Below is a chart which illustrates how even the largest of the large, three of the biggest domestic banks and those considered systemically important, couldn’t avoid being dragged into the banking sector group-think. The CDS for all three banks, JP Morgan, Citigroup and Bank of America all not only spiked but continue to be at historically elevated levels.

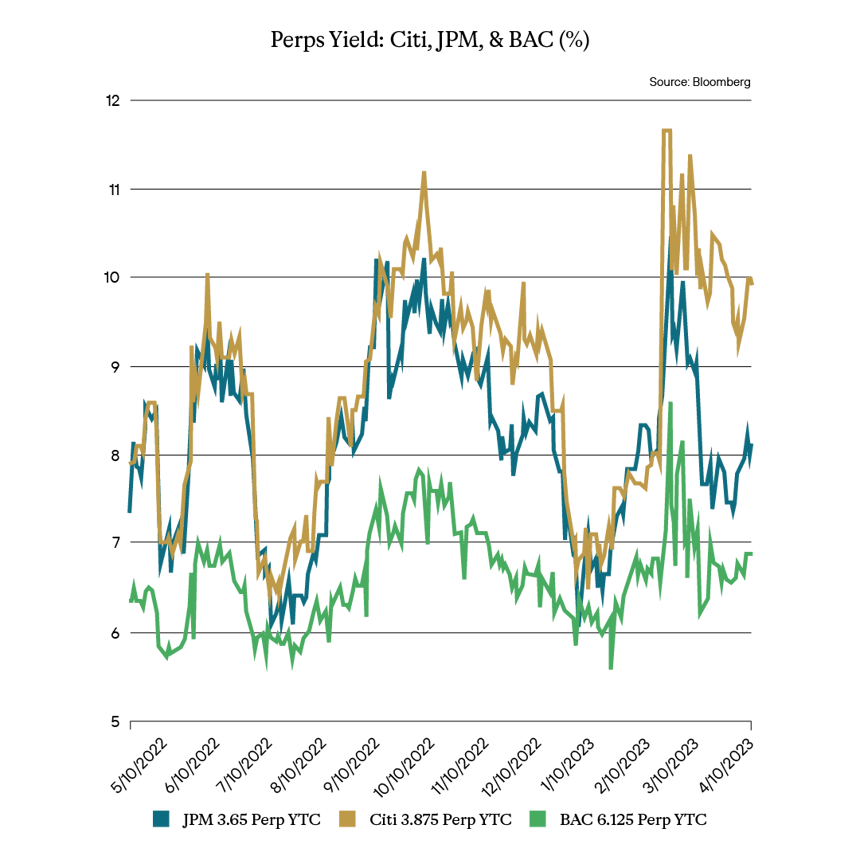

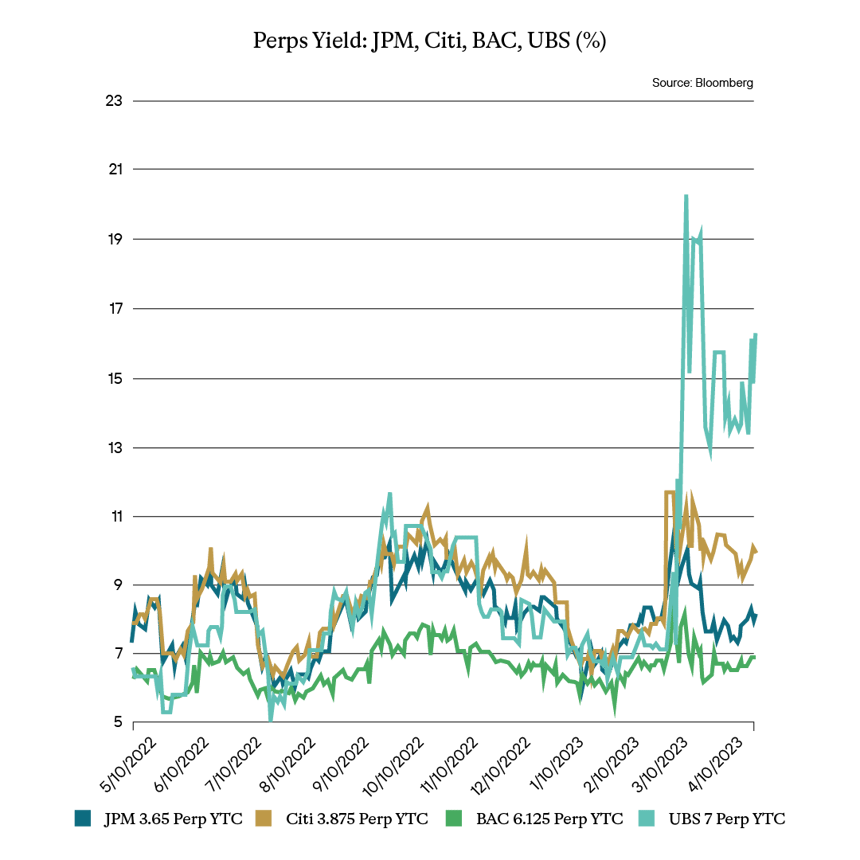

This widening in terms of CDS has translated into widening credit spreads, which in turn has resulted in every-increasing yield available to the investor. This is especially true when one looks at some of the more subordinated debt of these issuers. Perpetuals have long been a place where institutional investors found a steady, dependable income stream in exposures to some of the stronger credits. For even at this level of subordination, this debt for many banks still carries investment grade ratings. Furthermore, while this level of debt carries a name such as “perpetuals”, the majority of this type of instrument for capital ratios reasons etc. for these banks is generally considered likely to be called within 5 years. As such, the debt carries low duration risk and provides a desirable steady income stream. Nevertheless, with the “banking sector” under pressure, the yield on these instruments has risen to levels not seen in the past few decades.

In the example above, the JPM security carries a 2.74 duration; the Citi, 2.45; and the BAC, 3.4. Short duration risk and wide yields for three of the biggest banks in the market. In a vacuum, away from the noise of the market, that is obviously quite an opportunity. It’s a herd mentality that has made it possible.

UBS is one of the biggest global institutions in the banking industry, long considered an incredibly strong bank, and the bank regulators turned to for help when Credit Suisse started to crater. If a bank is on speed dial for regulators as one identified to help stem a banking crisis, then one should consider them pretty strong in terms of creditworthiness. And yet, the current market seems not to care. As detailed below, not only are their perpetuals wide like the domestic big 3 above; they are even wider based on current market pricing. The perpetual used in the chart below actually has a 0.71 duration, so even shorter than our examples above.

The danger of a herd mentality is that even in the best of times, it leads to a dangerous directional bet for the market. The herd moving in one direction means that if something bad happens to one, the majority are going to suffer. You don’t have to think totally outside the box, but sometimes opportunity and over-performance is available, simply by stepping back, looking around and recognizing that the herd is being led astray. Opportunities like the one above aren’t guaranteed success. There are market dynamics at play and in the short term, the market could move against you. But ultimate success and resolve ultimately leads to a successful response. We still remain concerned about the community bank sub-sector and are concerned about the tail risk of their commercial lending books, given how large an exposure that is for most of those banks. At the same time, it seems there is an opportunity to be had in the exposures of the largest, most important banks in the country.

We continue to be consistent in our outlook of issuers and sectors. Where value becomes available within those constraints and rules, is where we find potential out-performance and value. Certainly being able to make a distinction between what is troubling the smaller institutions in the sector and those of the three most systemically important banks in the country seems of value. The pull of the herd can be difficult to resist. Ultimately, value such as this is difficult to ignore, and often one you should be happy to embrace 8 days a week.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage - Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Duration - A calculation of the average life of a bond (or portfolio of bonds) that is a useful measure of the bond's price sensitivity to interest rate changes. The higher the duration number, the greater the risk and reward potential of the bond.

Control #: 16879464-UFD-5/15/2023