“Let me in, I’m starving.”

- Augustus Gloop

My wife’s grandmother used to complain about, well, a lot of things. It seems part of the package as you age. You complain. It used to bother me when I was younger. Now I’m older and it seems perfectly reasonable to complain about everything. The biggest complaint my wife’s grandmother had was how no one ever called her. The phone never rang. She was homebound mostly at that point, so every phone call meant a chance to greet the outside world. A ringing phone meant opportunity. I think about that a lot these days. I cringe every time my landline rings. My phone rings too much. Too much “opportunity.” Honestly, am I really the perfect house for solar panels? How much can I really save by utilizing an energy company that isn’t my local energy company but is technically an energy company, located in Saskatoon, and due to regulatory reasons can try now and be my energy company in New Jersey? And just what are the odds that I really am that easy to enroll in medicare a and b? I have the exact opposite complaint of my wife’s grandmother. Indeed, my cup runneth over when it comes to phone calls. Getting too much of anything never quite seems to be what you really want.

Over the past few years, with low rates, money market funds (MMFs) struggled. There was not much to offer in terms of yield out there, especially considering how short the paper they buy had to be due to regulatory constraints. As a result, assets under management (AUM) fell quite a bit. Oh how the investment firms that offered and managed these MMFs wanted rising rates. Higher rates would mean they could offer a more competitive return and attract more assets. Well when the Fed started their aggressive rate hiking campaign, MMFs cheered. They seemingly got their wish. And then they got Silicon Valley Bank (SVB); the added bonus of a bank scare, which meant a “flight to safety” amount of assets. So they should be happy, no? No. MMFs still have some complaining to do, and a little bit of worry. Because what managers of MMFs fear the most are: 1) a contagion run on MMFs which would result in massive outflows; and 2) massive inflows as a result of a market “flight to safety.”

The regulatory/governing rules for MMFs in addition to the industry consolidation, resulting in fewer and fewer managers, over the years has made it so most of the funds pretty much invest in a similar manner. Regulatory responses to previous crises have boxed these funds in. What that tends to mean is that in the wrong moment, especially if it involves a large bank having issues, they all run to sell the same things. The problem of course is that if they all are buyers of the same thing and then suddenly sellers of the same thing, who is left to buy that thing? Thus, if there is a run on MMFs they all tend to get caught up in the contagion. If one has a problem, it can become a problem for all of them.

But at this moment, those funds aren’t necessarily worried about contagion from a credit event. What they are concerned about is too many inflows too fast. Why would a heavy inflow of assets be such an issue? First thing we should consider is why the inflows are happening.

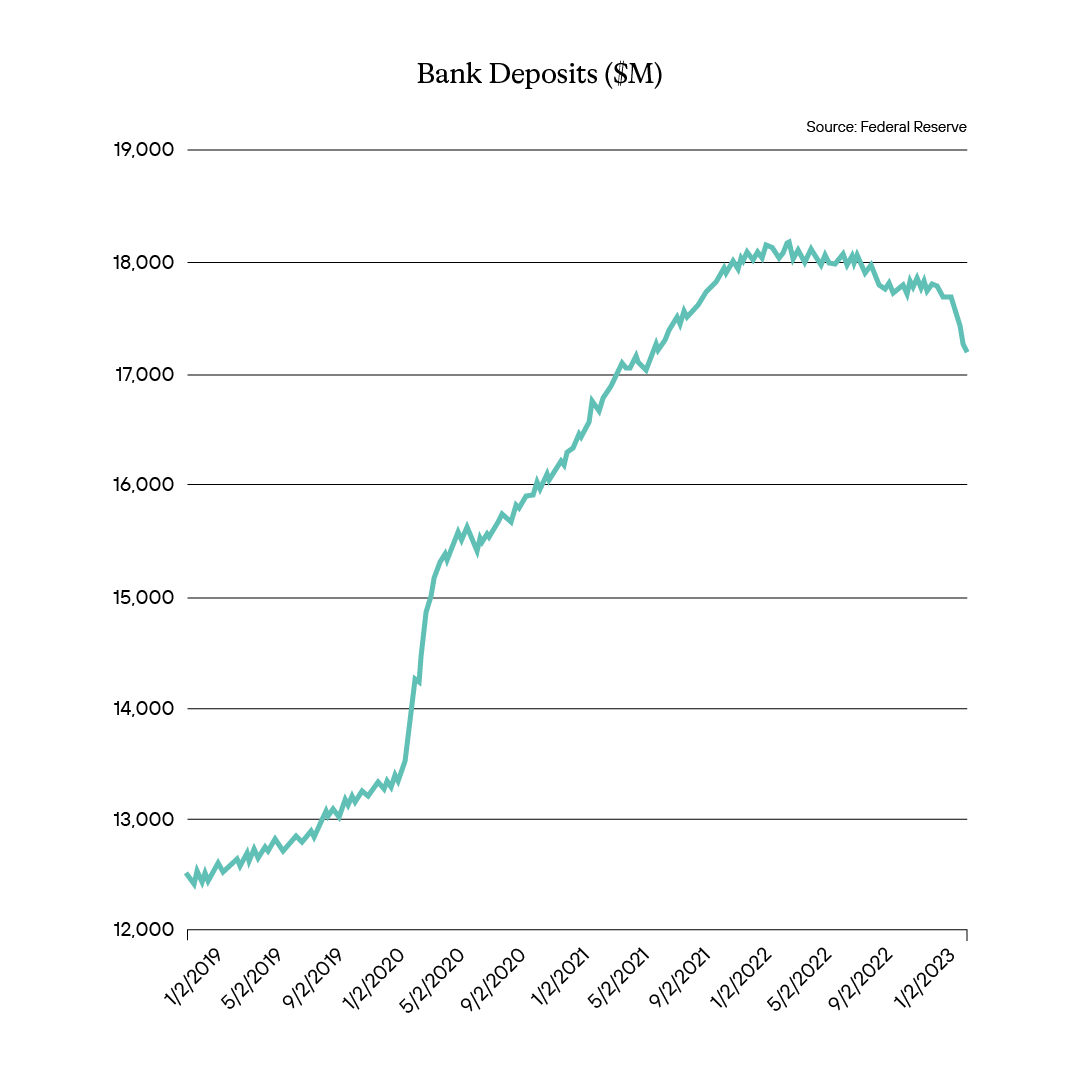

The sudden inflow of assets is a direct response to the banking sector being under stress. Not only were MMFs seeing heavy inflow from shareholders cashing out of positions in other types of funds due to concern about credit, they saw them from people pulling money out of the banks themselves. As can be seen below, there has been a noticeable decline in bank deposits overall, which has obviously accelerated into March with the pressures of the banking sector seeing concerns over the strength of those banks and questions surrounding whether deposits will be guaranteed above the 250k cap.

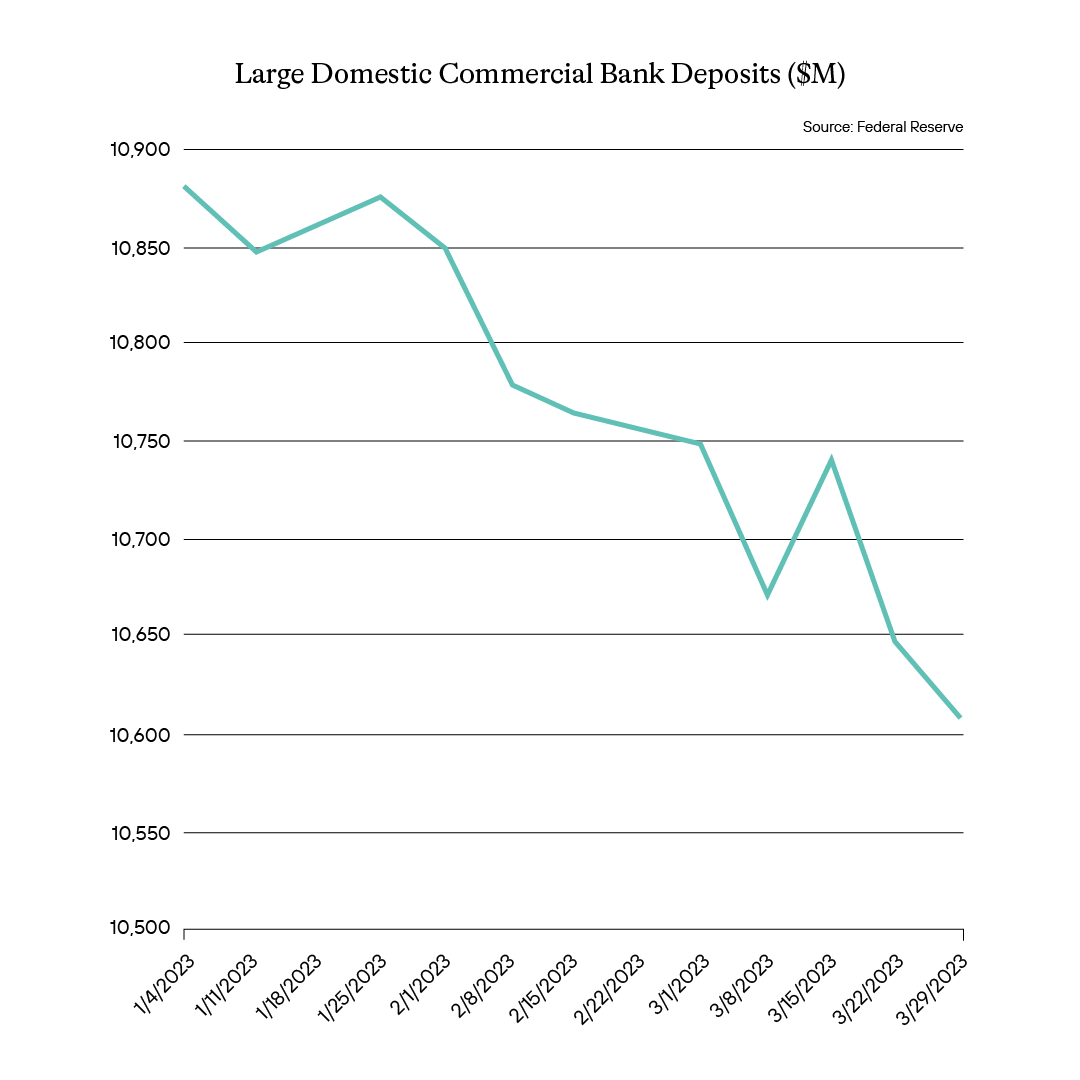

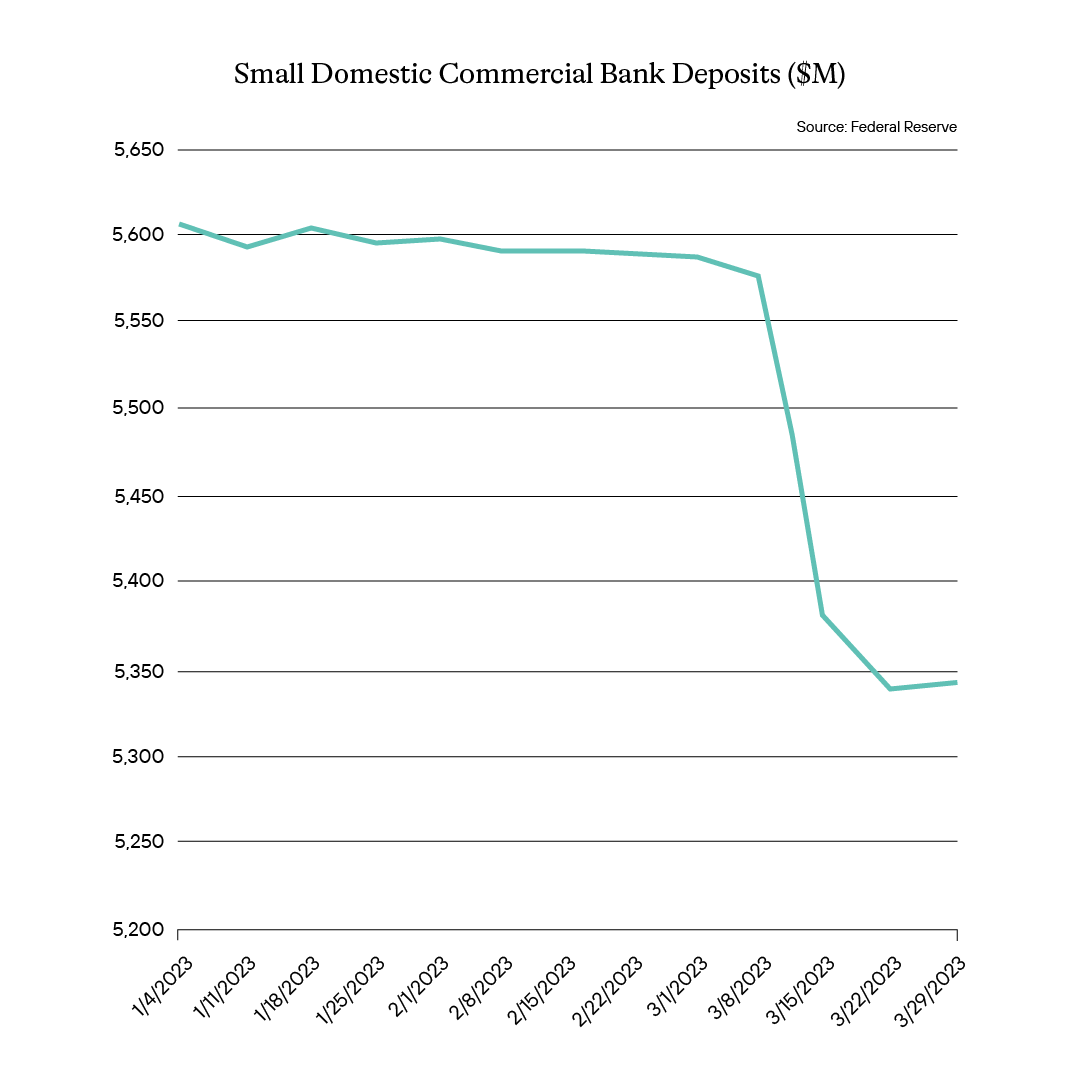

Interestingly enough there was some expectation it would be the smaller banking sector which would see outflows of deposits most and larger banks would seem more likely the landing spot. But as illustrated below that doesn’t quite seem how it worked out. Indeed while an initial knee-jerk reaction seemed to confirm that, with a large spike in large commercial bank deposits at around the time smaller commercial bank deposits fell. Shortly after that we still see some leakage of deposits at the larger banks.

The beneficiary seemed to be the MMFs.

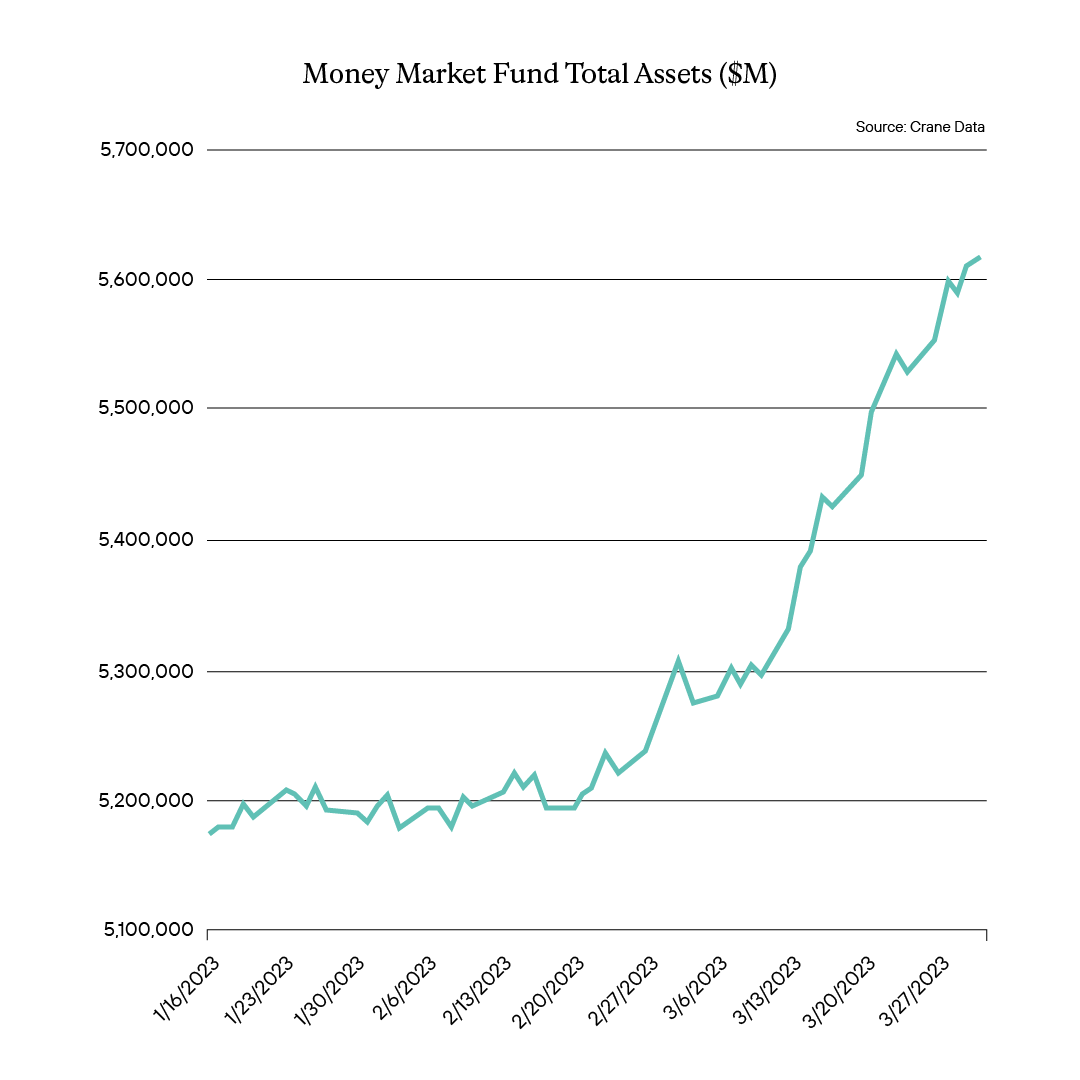

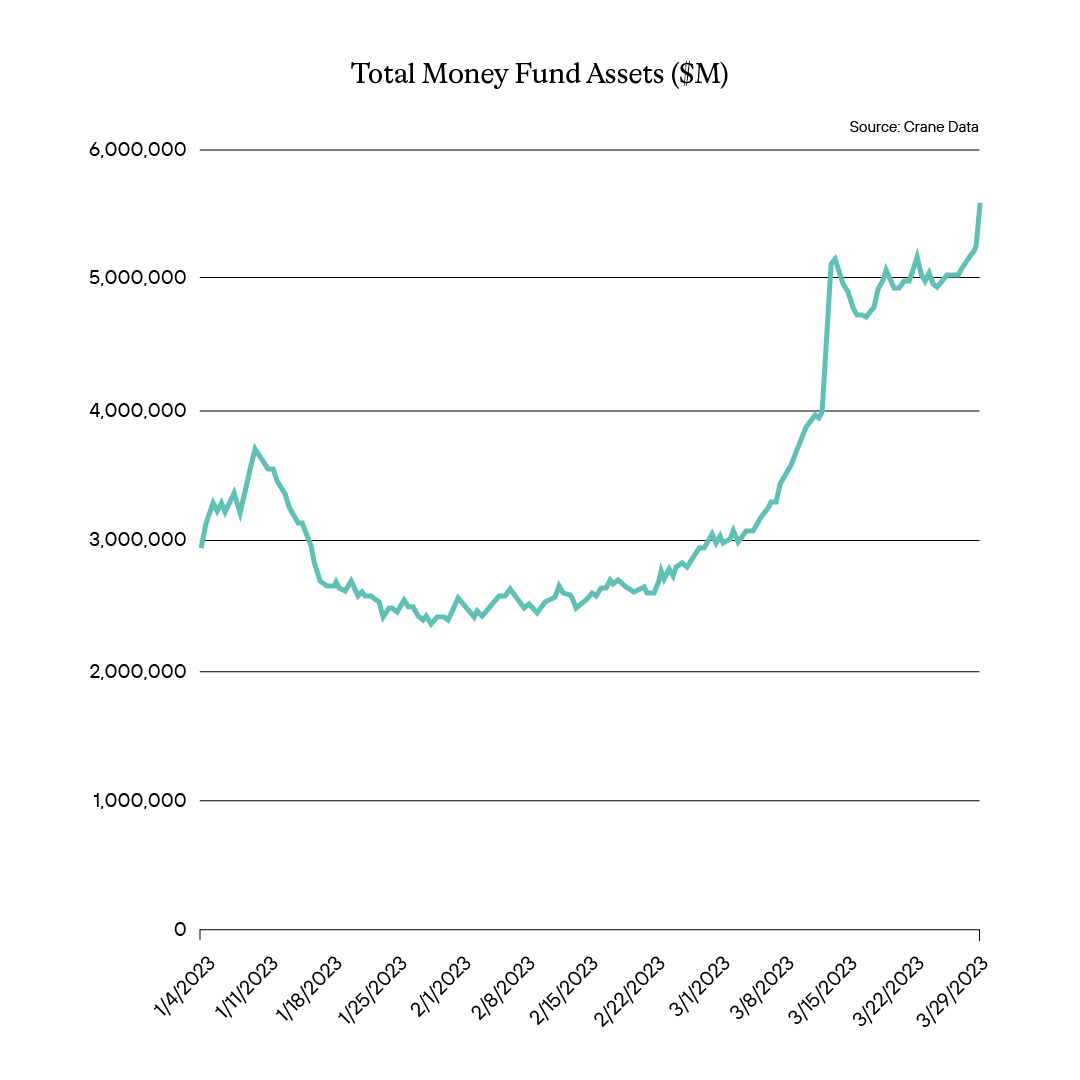

From a historical standpoint, MMFs total assets, which is comprised of retail and institutional money market treasury, government agency and prime (or credit) funds have never seen more AUM than right now.

So the moment they have all hoped for, heavy inflows have happened. But MMF managers start to worry because deep down they know that in moments like this, this type of inflow means that just as fast as the money came in, the money could leave. Fear and a flight to perceived safety means that a very large percentage will leave once the “all clear” horn sounds. Leading to them potentially having to sell all at once with their seemingly structured brethren.

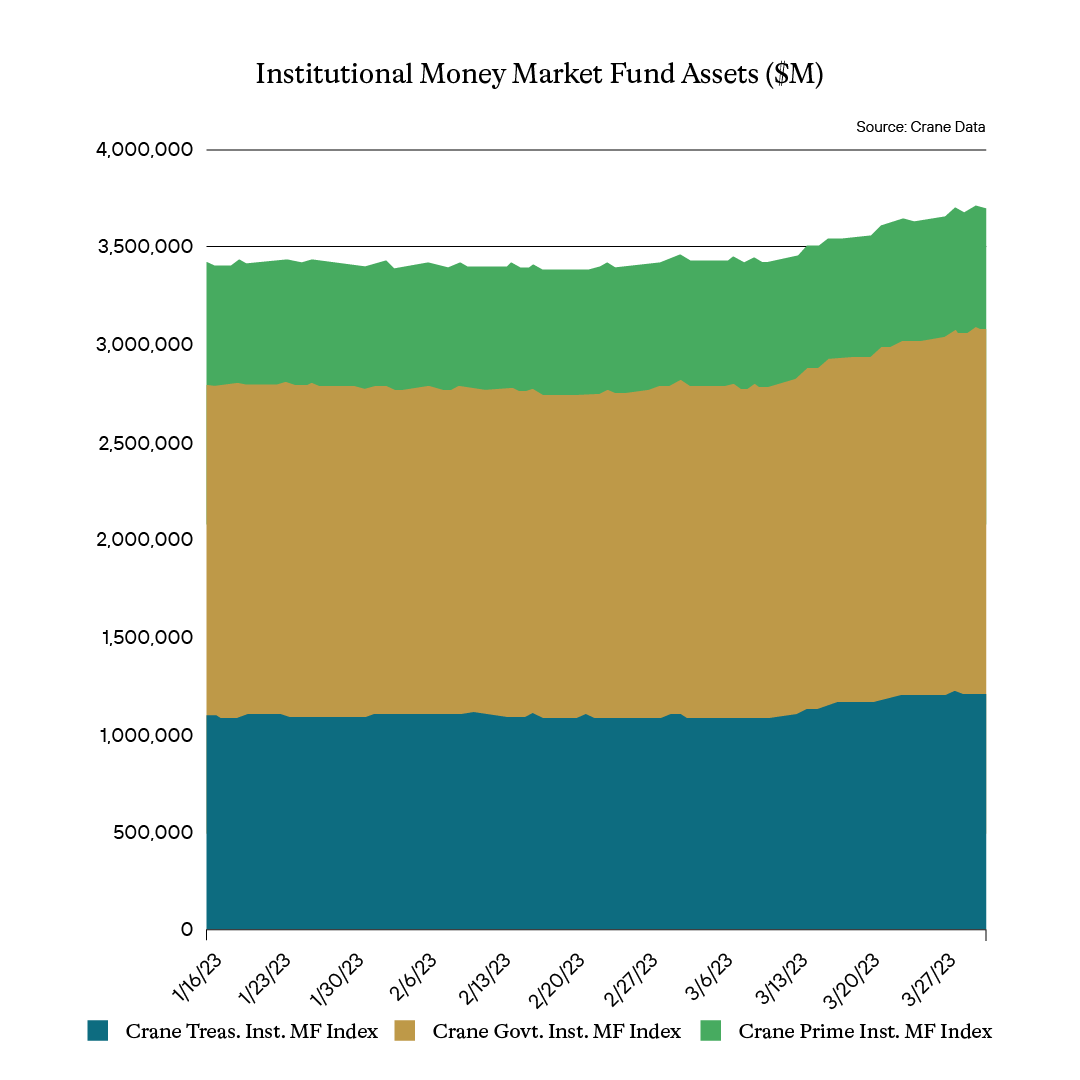

Some of their concern has to do with the MMFs shareholder composition. As illustrated below, the bulk of MMF assets are concentrated in institutional money market funds. Institutional money in MMF is typically considered less sticky than that of retail funds. Worse, institutional money is generally larger in size. That is, if a corporate treasurer were to deposit money in a money market fund it could be in sizes of like $25 million, $100 million or $500 million. While retail, of course, tends to be a lot of much smaller accounts. Those funds can be heavily populated with individuals with $500 in their accounts. That means that once those institutional accounts feel that the worries are behind them they are just as likely to pull those large amounts out to go invest elsewhere. As such, investment managers are fearful to invest recent inflows too aggressively because they assume the money will be leaving quickly and they don’t want to have to sell at a moment when everyone else is selling for the same reason.

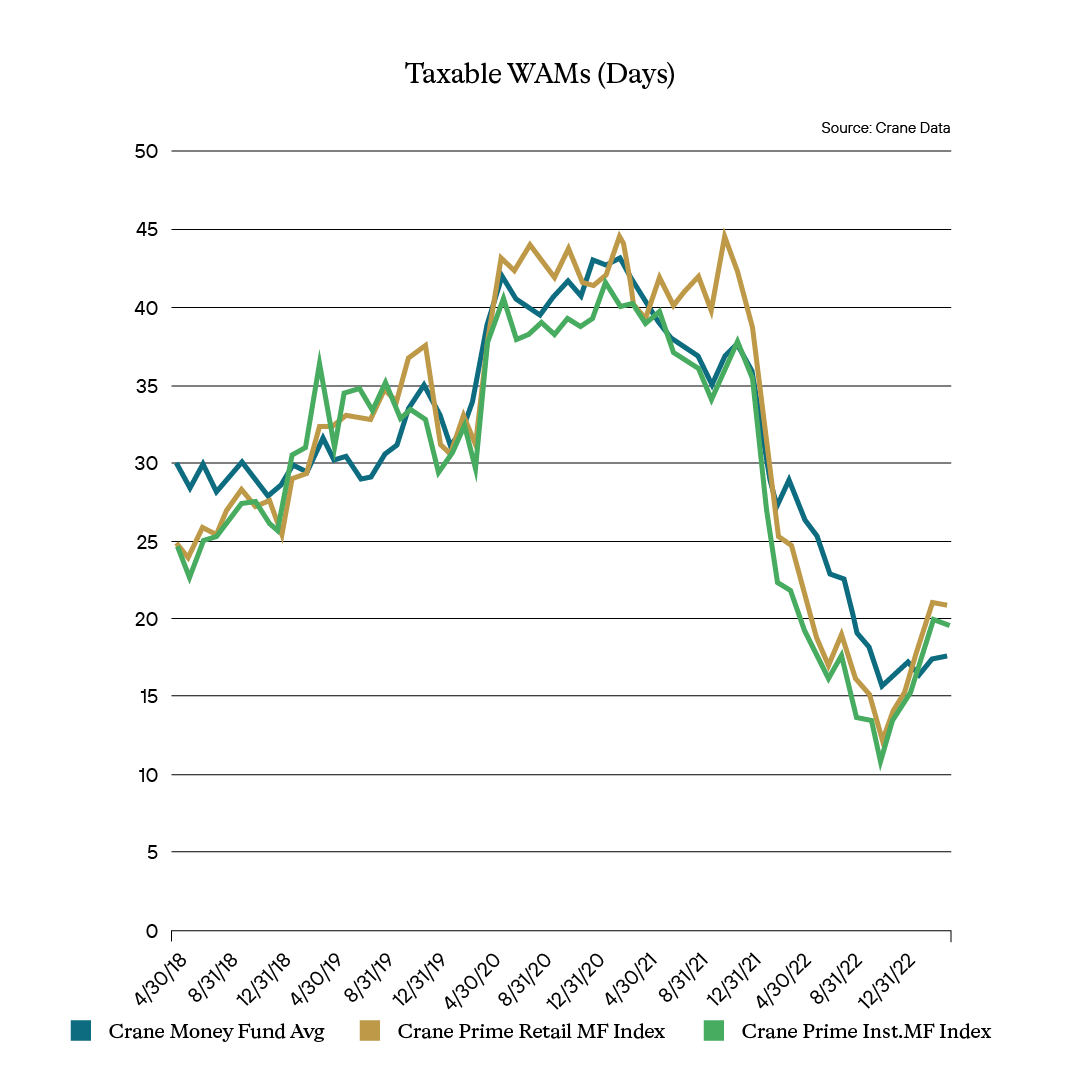

So they would most likely all invest short. Not that they don’t do that mostly now. Over the years, after the Great Financial Crisis and even most recently, the pandemic, regulators noticed strains in the money market fund sector and in typical fashion responded to that by placing additional burdens on these funds further limiting their investment options. The governing rule, Rule 2a-7, has multiple restrictions which tend to make the funds invest in a similar fashion. One of the biggest ones has to do with weighted average maturities. Overall the prime money market funds, or credit funds, must make sure that 10% of their total assets are held in daily liquid assets, at least 30% of the assets are in weekly liquid assets, and the weighted average maturity (WAM) doesn’t breach the maximum of 60 days. As illustrated below, WAMs for the taxable money market funds are less than 20 days currently, as reported by Crane Data. Part of that current industry WAM of course is the overall requirements, but a great deal of that right now is fear that what assets came in will soon leave. That of course limits what you can invest in, meaning that what yield you can generate is limited due to maturity restrictions, and ultimately does mean once rates begin to get cut, which market expectations currently indicate as soon as July, will see definitely a quick drop in yields for these funds. The fact that the fear of massive outflows is on the horizon and they are forced even shorter means it could happen even faster.

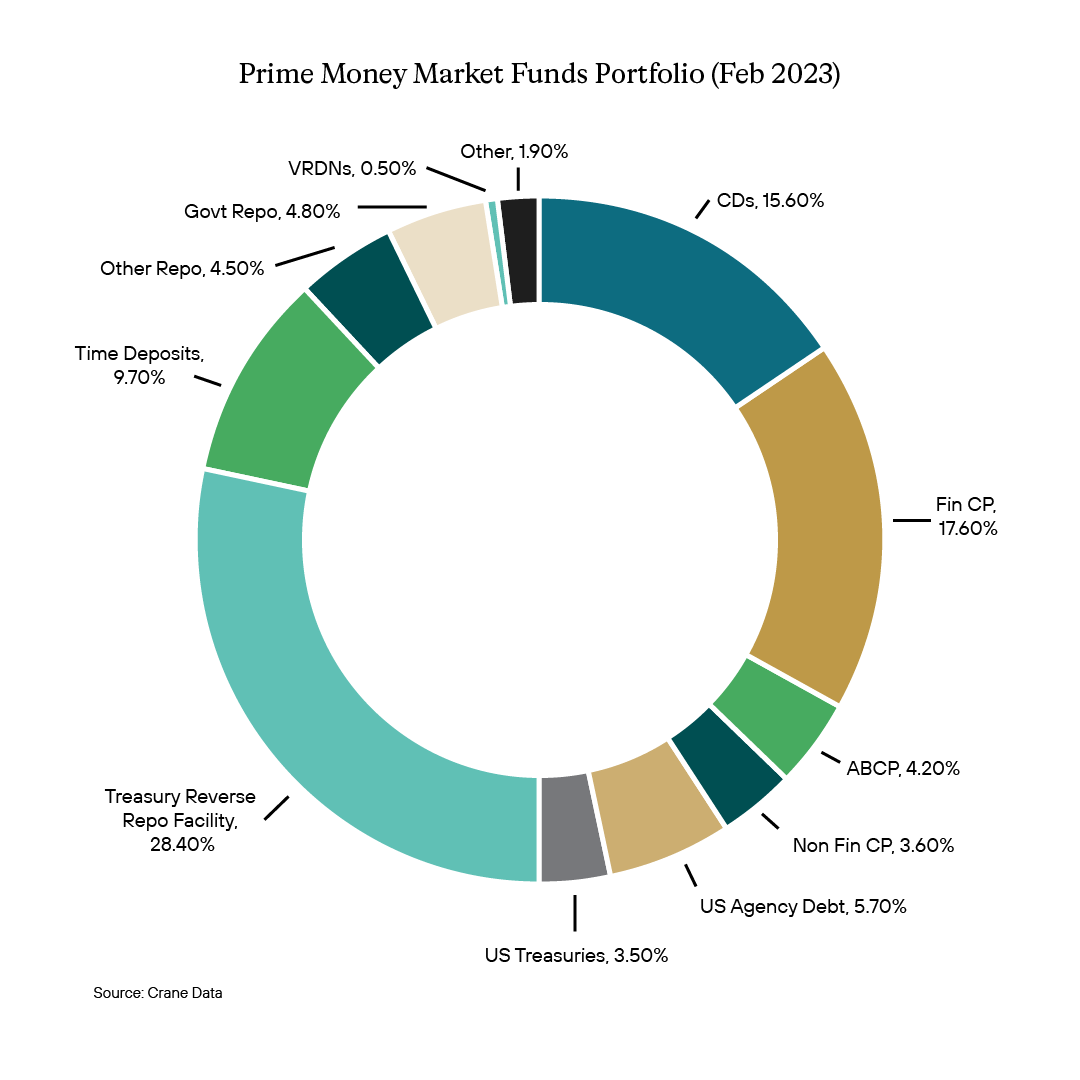

Prior to the bank stress, MMF portfolios were typically considered pretty diverse. But again, regulatory requirements made that less than one would assume, and market participation, just who does the short market to fund themselves, made it even less so. And so what that means is what most investors miss is just how heavy the bank exposure can be in MMFs. The reason is that banks tend to be some of the biggest issuers of things like commercial paper (CP) in the short end, and once you factor in certificates of deposit (CDs), Time Deposits, variable rate demand notes (VRDNs), bank sponsored asset-backed commercial paper programs (ABCP), and even non-government repurchase agreements (repo) due to counterparty risk, MMFs actually have a great deal of bank exposure.

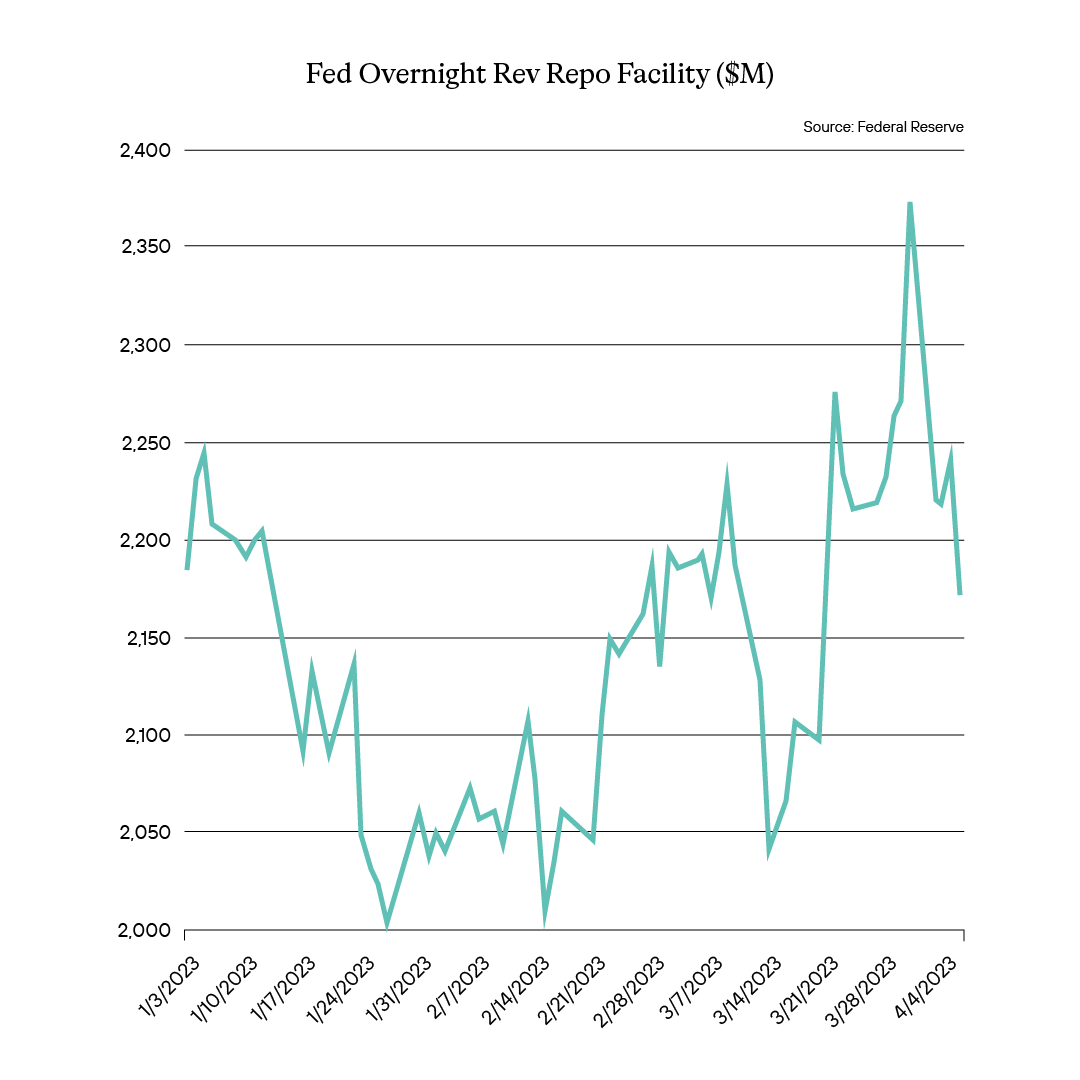

In the wrong moment, like the Great Financial Crisis, the heavy bank exposure across the board for the money market fund universe proves problematic. Today, if they invested the inflows in a similar fashion to that which they had done prior to the flight to safety, it could be just as problematic. Especially if the assets were to leave just as quickly and they all turned to sell those positions. So given the fear of exit velocity on the inflows and the regulatory burdens, what are they doing with those flows? Well, turning to the Fed and its overnight reverse repo facility. As illustrated below, and as expected, that facility got heavy usage by MMFs. And while the usage of that facility provides MMFs with an outlet for their cash, it obviously ultimately hurts their yield today and limits just how much those shareholders in the fund can benefit down the road.

Money Market Funds serve an important role in the capital markets. But at certain times there is an expectation or a misunderstanding of not only what type of credit risks they can and do take, but also what regulatory regulations and their own fear mean to future returns. And furthermore, as the rate cycle and the hiking cycle comes to an end, what that might mean in terms of future yield.

Getting a large inflows in a short period of time isn’t what dreams are made of for these types of funds. They simply won’t and can’t for a variety of reasons invest those assets in any sort of normal manner. Ultimately those flows lead to concerns about the velocity at which the funds will leave and making sure they avoid whatever contagion risk that might have sent the assets their way to begin with. The sudden influx of assets forces them to invest shorter and shorter knowing that assets will leave, and coupled with expected rate cuts which could come as soon as months away, we would expect yields on the funds to begin to drop. Interestingly enough, what they typically would want, the inflow of assets, is now something to complain about. They can’t invest like they’d want into higher rates and, worse, fear having to sell en masse as those assets leave. A simple case of too much, too soon.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage - Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

Bloomberg U.S. Agg - The Bloomberg Aggregate Bond Index or "the Agg" is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Control #: 16748656-UFD-4/17/2023