“It is amazing what you can accomplish if you do not care who gets the credit.”

-Harry S. Truman

Several years ago I had to succumb to a root canal. It is one of those scary things that seems to get scarier when you hear other people talking. Surely something to avoid. Up to that point, I only could imagine what a horror awaited me by the countless jokes I had seen over the years on every sitcom I grew up watching on TV. It took an ex-dentist’s mistake, but my mess to clean up, with the dentist only there for moral support and a “see you at your cleaning six months from now” send-off. But my moment came. I had a root canal. Was it pleasant? Not really. Was it one of the worst things I’d sat through? Not even close. I had managed to make it through 3 hours of the movie Titanic. This didn’t seem so bad. To be honest, I listened to the piped-in to soft rock, and sometime after Steely Dan’s Hey Nineteen, it was over. I chatted with the endodontist and I was on my way. It wasn’t fun. But it was over. And that is kinda the way I’d look at the last month of 2022. It wasn’t great. It wasn’t fun. But it’s over. We finally got into the new year. And since then? The markets have roared back to life. There has been a sharp rally in rates, robust issuance and heavy demand. Suddenly everyone has forgotten the misery and is embracing what the new year might mean in possibilities.

The new year certainly seems to show promise. The prior six months were a moment to be conservative but selectively opportunistic. More importantly, to pounce on opportunities when they presented themselves to build a foundation for future over-performance. So does the new year show that much more promise that a more aggressive attitude is needed? Maybe not. For we continue to see opportunity, but in some cases, prefer to look at it not so much as some of our competitors seem to be doing, as a moment to get grabby with credit and risk, but rather stay on a course closer to what might on the outside seem boring. Because in this case, there is opportunity to be found in the boring. Sometimes the best investments are the ones that just get the job done with little fanfare. Indeed, in this case, boring, may be the next wave to catch.

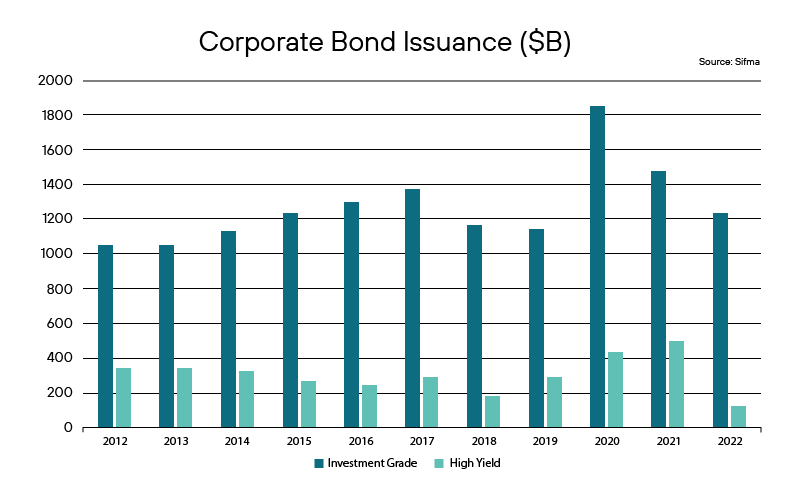

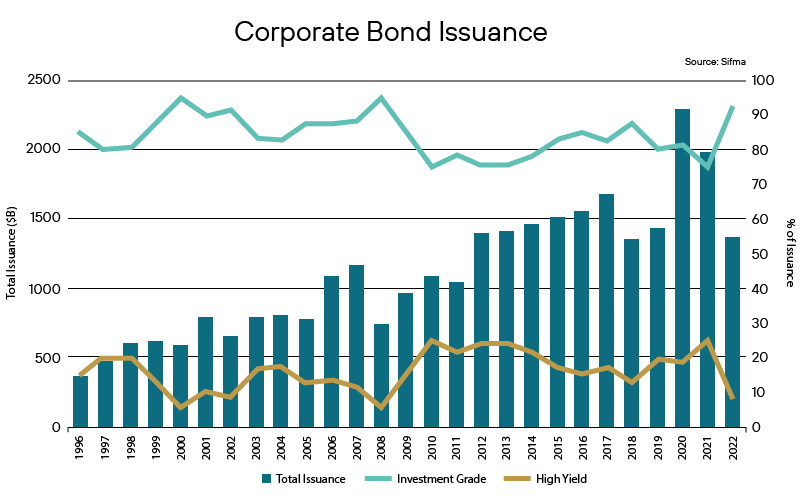

Investment grade corporates aren’t always the sexiest of trades. Especially if an investment manager has a wide set of guidelines. High yield tends to get a lot more attention. Sometimes it has to do with a simple commentary on the health of the credit markets, and other times it is simply an explanation of how aggressive one can get to capture outside returns. But who doesn’t love to go to a cocktail party and discuss the outsized return one made in a Party City bond? The fact is investment grade credits don’t capture the imagination. But there sure is a lot of it and maybe that is one of the reasons it seems so boring. Over the past few years, overall corporate bond issuance has been noteworthy in size. We have commented on the historical amount of issuance that came to market, juiced by a low interest rate environment that stimulated outsized supply and demand. Not discussed so much? Just how much more investment grade issuance is out there versus high yield.

And maybe that is what to initially blame. Part of what makes investment grade so boring is that there is plenty of it in comparison to high yield. On a percentile basis, investment grade is historically a much larger portion of whatever total issuance pie there is. This becomes especially obvious in darker times like 2008 or even more recently in 2022 in the midst of a historic rate hike cycle. So no one really likes talking about investment grade until they need shelter. Shelter from credit, but also the warm embrace of liquidity. The sheer size of that market, especially in comparison to high yield, would lead one to believe that it is obviously more liquid than the high yield market when things get tough, but then again so does the actual amount of trading.

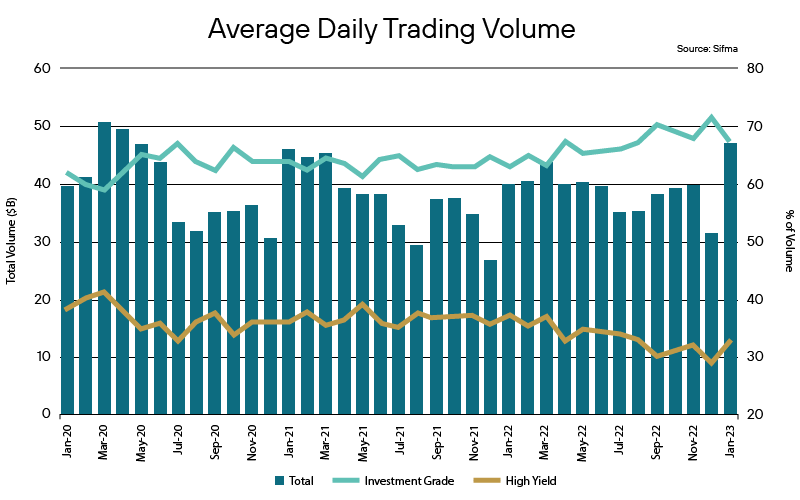

As illustrated below, and an important point, the liquidity of investment grade is obvious when simply looking at trading volume. There is more of it, sure. But it also changes hands a great deal more as well. As can be seen below, the average trading volume, on a percent basis, is skewed to investment grade. Again, hammering home the point that in more trying times, this is especially true, such as can be seen in the months from March 2022 to end of year 2022, during the time the Fed started its tightening. The most obvious indications when that gap closed? March 2020, when the Fed rushed in to lower rates and backstop credit in the early days of the pandemic and….the first month of the new year, 2023, when everyone was feeling exuberant at the thought that the Fed might be nearing the end of its campaign to raise rates.

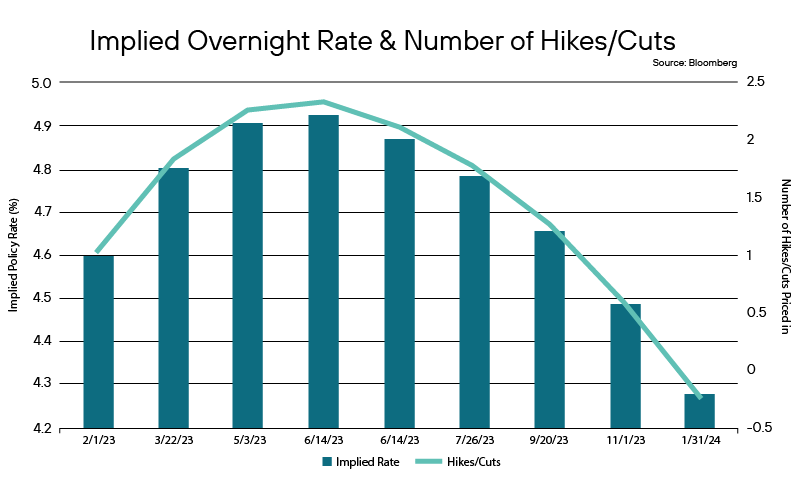

Rates obviously have been the majority of focus of recent headlines. But what sometimes gets lost when looking at current Fed actions and how many near-term rate hikes are left is what the market anticipates once this is over. Market sentiment debates a Fed pivot and whether past rate hikes have a tail risk to them, that is, have they overshot and will they push us into a recession. The soft landing discussion and concern is out there, but it seemingly takes a back seat to current rate volatility concerns. Nevertheless, when one takes a look at rate expectations several meetings out, maybe even mid-year, we might, based on these expectations, start seeing…rate cuts. Hard as that can be to think of right now, given we still are expecting more rate hikes, there is a market expectation that rate cuts aren’t that far off.

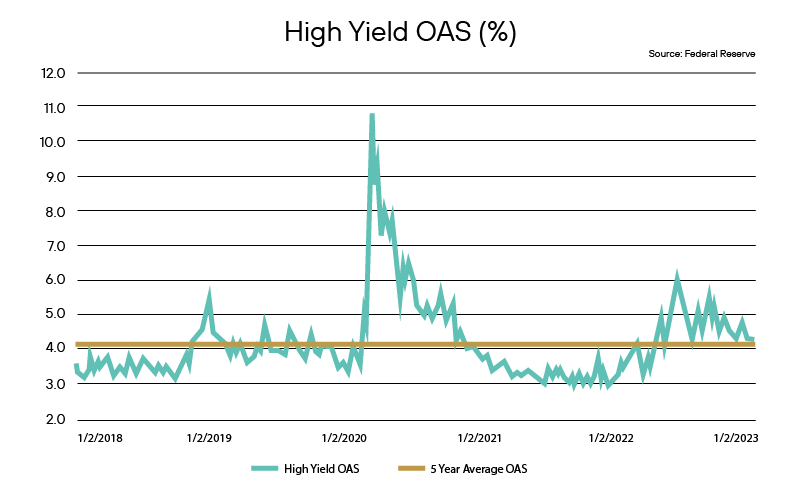

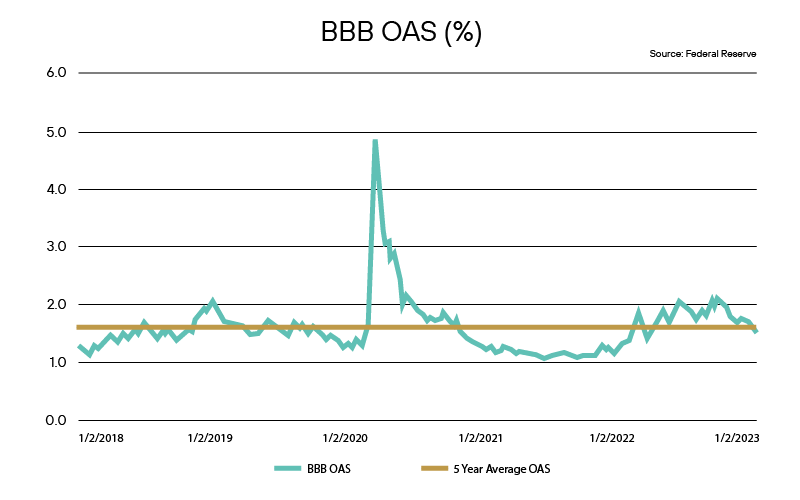

Maybe the Fed gets its desired soft landing, but right now it is hard to ascertain whether that will or won’t happen. We are still not where we want to be inflation-wise. Not yet. And there is still a chance that the landing doesn’t turn out to be so comfortable, as the weight of the rapid rise in rates could’ve overshot the mark. If that is the case, then we tip into a more recessionary climate. Just like that. Credit spreads are not so sure. One look at them would indicate that things are what they seem. Both the High Yield OAS (encompassing all bonds rated BB+ and lower) and the BBB OAS seem kind of where you would expect them, right around their 5 year average OAS.

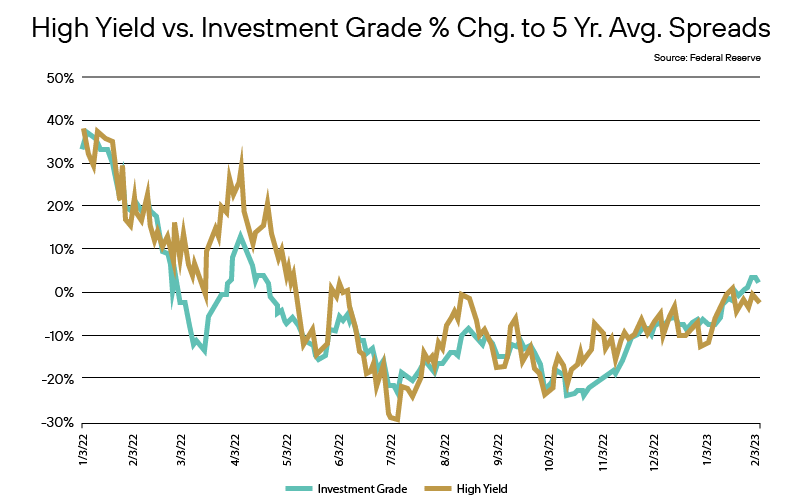

But that is a bit misleading, given that high yield has had quite a run, not only in terms of issuance levels but on providing weaker credit firms a platform to feast on low rates to meet historic demand from a larger than typical investor base desperate for yield in the recent low rate environment. Indeed, if we just compare High Yield to IG credit as a % of change to their respective 5 year average spreads, one can see that investment grade, well, it looks comparatively cheap. That is right now it looks cheap. Rightly so, given the conditions mentioned above. But surprising nonetheless. Huh. Maybe not so boring.

But what happens if we do slip into a slowing economy or even a recession?

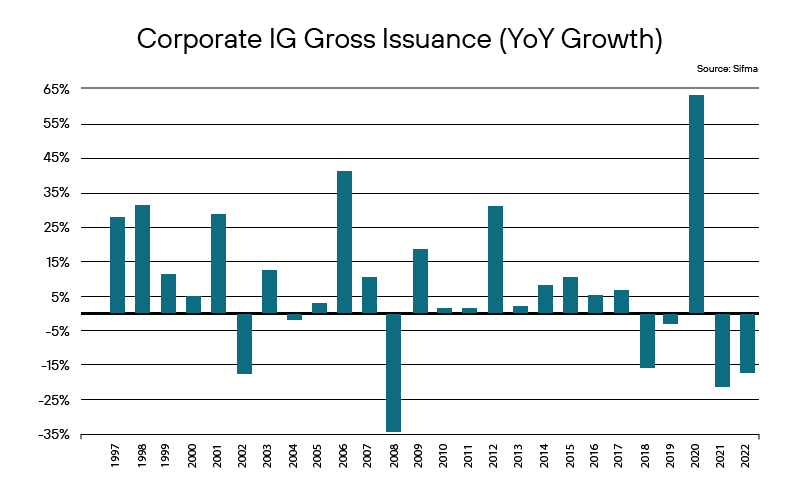

In a recently released Bank of America fund manager survey, some 55% of respondents indicated that in a slowing economy, the one thing they hoped corporations would do with their cash flow is improve their balance sheet. In other words, stronger credit. And it isn’t just what investors want, it is what stronger credits do. As can be seen below, in times of slowing economic conditions, IG issuers tend to slow issuance down in response. Indeed, they retreat to protect their balance sheets and credit ratings. And investors reward them for that in times of stress, as they flock to those investment grade credits for shelter. Given that, demand would be increasing at a time issuance is shrinking. The result? It should mean spreads compress with the excessive demand, and with it, over-performance is available to those who grasp this ahead of time.

Current conditions indicate to us that investment grade credit is comparatively cheap to high yield right now. If we consider that economic conditions shift to the downside, data and anecdotal evidence seemingly indicate that there will be a demand shift away from high yield toward IG. This at a time that issuance, as a result of economic conditions, would shrink. And as this shift occurs, one certainly would rather already be positioned in the more liquid area of the fixed income markets, simply to avoid having to sell less liquid exposures at the same time most decide to move. All of which would seem to lead one to conclude that if IG was comparatively cheap now, it is even more so when one considers what may be in store in the near term.

One positive outcome of the Fed’s aggressive attack on rates has been that yields across the credit stack, but especially in the high grade area, have risen. That has led to conditions in the marketplace for investors to move up in credit and not have to reach down in credit to capture solid returns. We have spent a great deal of time targeting preferred sectors and issuers in this manner, seeing value in moving into the more liquid, stronger credit area of the marketplace in anticipation of what we see amongst the data. We expect in the near term that taking advantage of these conditions now will not only help build the credit strength and liquidity of the portfolios up, but once a shift in demand happens and spreads tighten, be able to benefit from the potential over-performance this foundation is creating.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage - Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Gross Domestic Product (GDP) - one of the most widely used measures of an economy's output or production. It is defined as the total value of goods and services produced within a country's borders in a specific time period—monthly, quarterly, or annually.

Perp - A perpetual bond, also known as a "consol bond" or "perp," is a fixed income security with no maturity date.

Nonfarm payrolls (NFPs) - the measure of the number of workers in the United States excluding farm workers and workers in a handful of other job classifications. This is measured by the federal Bureau of Labor Statistics (BLS), which surveys private and government entities throughout the U.S. about their payrolls.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

Job Opening and Labor Turnover Survey (JOLTS) Report - is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

Sifma - The Securities Industry and Financial Markets Association (SIFMA) is a not-for-profit trade association that represents securities brokerage firms, investment banking institutions, and other investment firms.

Control #: 16437225-UFD-2/15/2023