“I've been drivin' all night, my hands wet on the wheel

There's a voice in my head that drives my heel

It's my baby callin', sayin', "I need you here"

And it's a half past four and I'm shiftin' gear”

- Golden Earring

Everyone in the financial markets seemed eager for a roadside rest area by the end of the year. Eager enough that the landscape looked like a small town in a sci-fi movie: desolate, empty streets; an eerie breeze kicking up dust; and a decrepit motel with a vacancy light flickering before going completely dark. Indeed, by mid-month it seemed most participants simply threw their hands up, turned the office lights off, and went home to enjoy the holidays. But enjoying the holidays isn’t quite what it used to be. More and more, enjoying the holidays means spending. Apparently, based on every commercial I see, you aren’t in the holiday spirit if you aren’t doing two things: straining your credit limit and decorating your house with cinematic-level pyrotechnics and accompanying surround sound special effects. Gonna be tough to look the kids in the face if you don’t; failure is not an option.

All of this is being executed under the cloud of the Fed’s rate hiking program. The relative good news is the Fed seems to be winding down its efforts, and so many in the financial markets are already eagerly looking forward to the pivot to rate cuts. Nevertheless, we still had another hike or two to take into account as well as the seemingly endless barrage of Fed speakers who seemed quite eager to spread their hawkish cheer into the new year. Some leading voices in the financial markets have questioned whether or not it might be a good idea to step back and see just how impactful the previous Fed hikes have been, but at least up to this point, the Fed doesn’t seem eager to do that. That doesn’t mean we can’t. Because, on the surface, the economy continues to hum along at a pace considered a bit too hot by the Fed, and while they seem to be the ones with their hands on the wheel, determining the exact right time to find an exit ramp, as we will see, it is the consumer/borrower who is starting to sweat a little bit under the possibility that we already passed it.

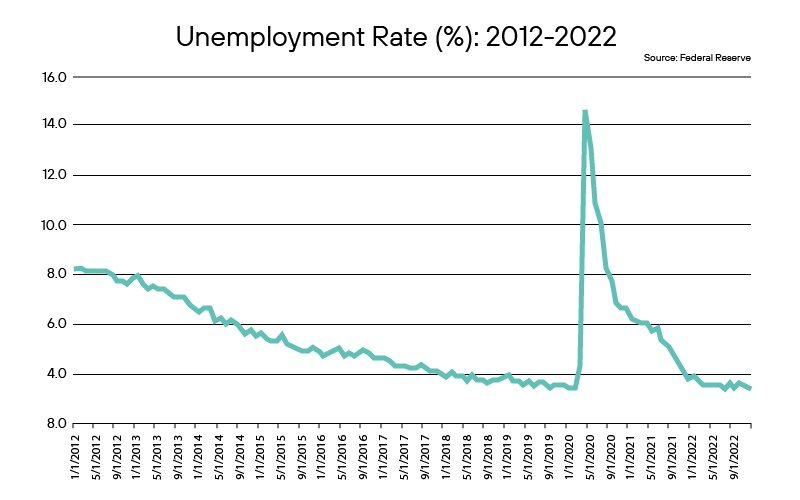

Inflation has shown some signs of abating, but the Fed, and notable industry voices have seconded, that there is still much to be worried about with inflation. More recently, and more loudly of late however, the Fed seems focused on the job market, which, much to its dismay, continues to show data-wise surprising strength. The unemployment rate in particular continues to hover around historically low levels.

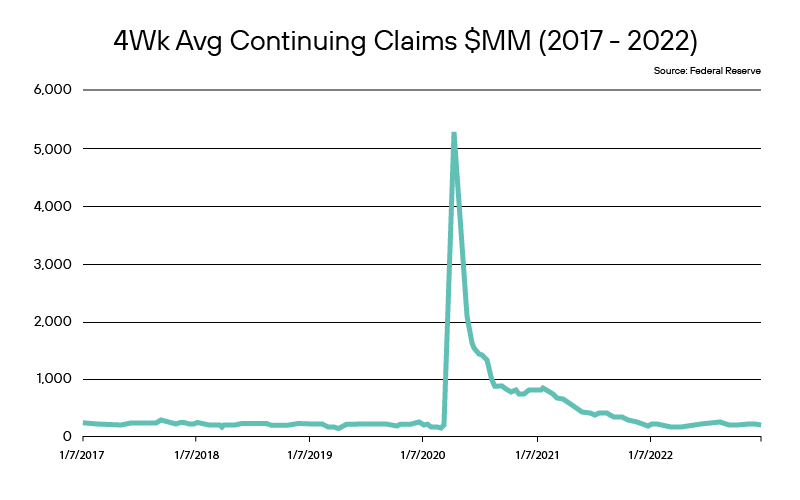

And continuing claims projects a similar story, with the four week moving average confirming that employment and the jobs market seems resilient in the midst of the historic rate hike cycle.

It has been a noticeable pivot by the Fed, as it still harps on about inflation but certainly has been more and more focused on the job market, highlighting it as potentially being too hot. So jobs have certainly moved up in terms of important data points for the Fed. And that would make sense, as the ability of the consumer to spend and drive excessive demand leading to supply shortfalls and rising prices certainly is a big reason for inflation. And yet, the Fed actions have begun to take some toll on the consumer, in their borrower role, in a number of ways, some which might turn out to be more damaging than being given credit for.

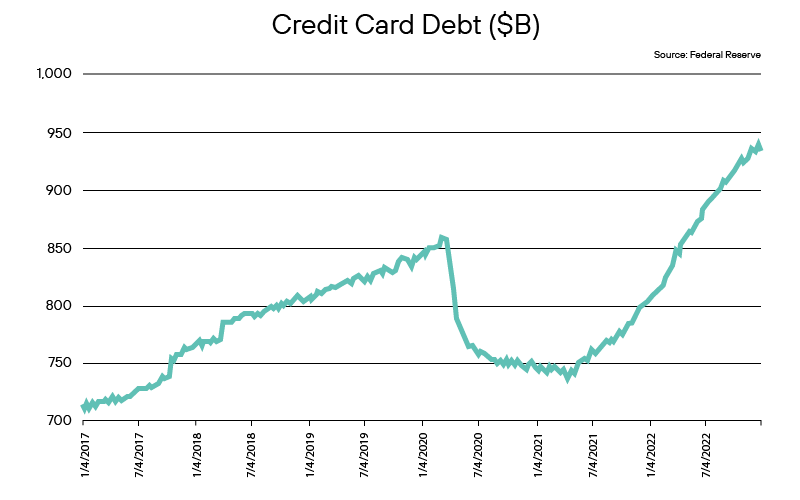

Indeed, while Fed has been the one driving the car, it seems that the consumer’s sweaty hands are now on the wheel. For one thing we are historically good at as a country is borrowing. And boy do we love to use our credit cards, which these more modern technological times demand we use more and more. It isn’t enough that you want to use it for the miles or ease of use, its now demanded we do so. For not only do we have a growing penchant and love for on-line shopping, but the pandemic also introduced us to the impersonal wonders of “contactless” transactions. Combine the modern demands for credit card use, with a consumer enjoying job security, and it’s not surprising we have been witness to credit card debt reaching historically high levels.

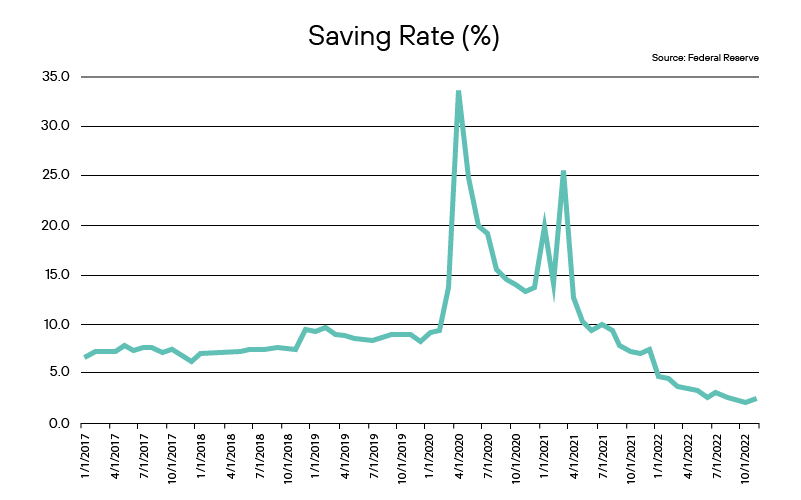

By itself, maybe that wouldn’t be that concerning. We have those great employment numbers, so everyone is working, right? And sure it is higher than previous years, but during the pandemic, because we had nowhere to go and nothing to spend on, we were all saving. So we had built a cushion for when we could spend again. Well, with inflation taking a bite and with an unleashing of a frustrated consumer, that cushion is long gone. As illustrated below, the saving rate has plummeted with our spending and borrowing. In other words, our cushion is gone.

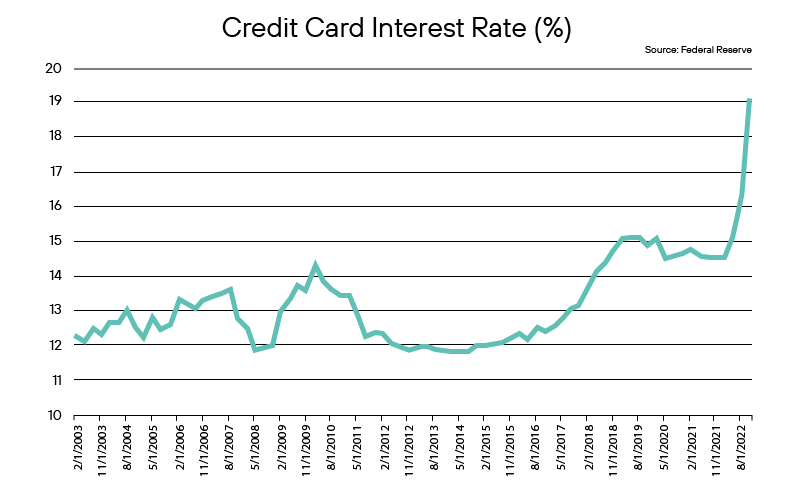

So with a plummeting saving rate and rising credit card debt, the Fed’s rate hikes become all the more important, given their impact on things such as the interest rate charged to that outstanding credit card debt. And as can be seen below, that impact is quite noticeable. The rate hikes have obviously translated into surging rate increases on the equally surging amount of outstanding credit card debt.

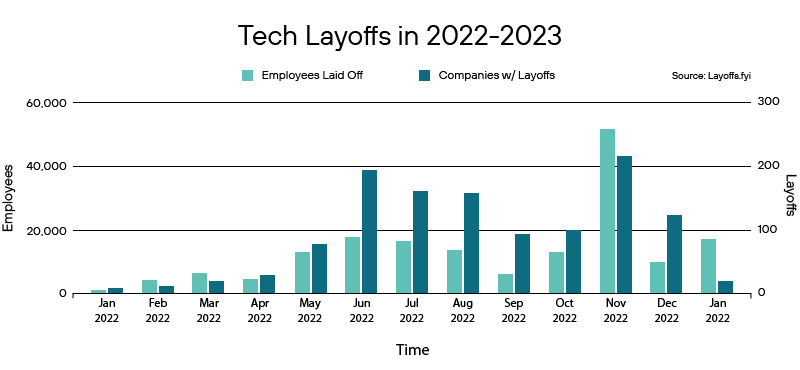

The current response is merely to shrug, and say the Fed is right to pursue its path, and given the jobs data remains strong, the drag of higher interest rates should only lead to a slowing economy. So a lot is riding on jobs maintaining strength to withstand this. And while current unemployment figures seem supportive, we see some weakness. Not loud trumpets yet, but sporadic. A headline here. A troubled company like Bed, Bath and Beyond there. In other words, spread out enough that they are almost treated as one-offs. But it seems more like an unrecognized trend. Over the past few months, here is a running total of a few notable names we have seen pop up with announced layoffs: Amazon, 18,000; Cisco, 4,000; Coinbase, 1,200; Doordash, 1,250; HP, 6,000; Meta, 11,000; Salesforce, 8,000; Twitter, 3,700; Goldman Sachs, 3,200; and Credit Suisse, 9,000. And if we just look at the tech sector, well, it doesn’t look great.

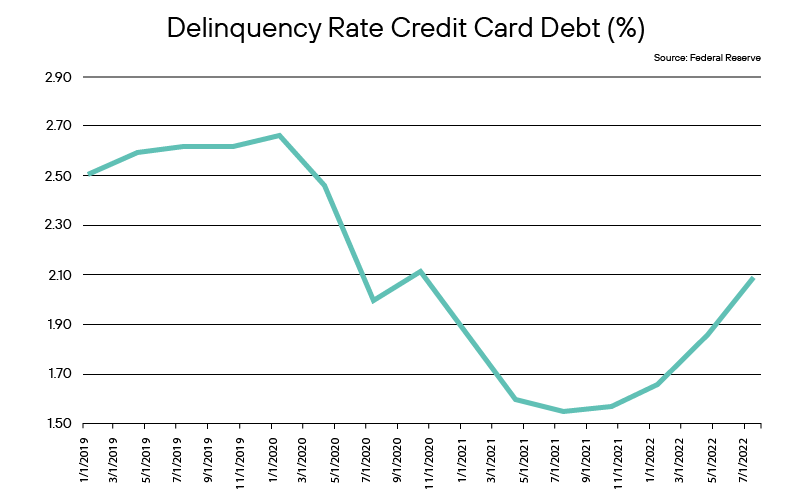

All of which would indicate that while current unemployment numbers seem strong, there is a wave of layoffs building and that obviously is going to translate into changing unemployment data points. So the strength of the job market may not be the backstop we have been counting on to ride out the rate hike cycle and smooth the edges of the economic pain the consumer/borrower has been able to withstand of late. And there is even a question of just how much the consumer really has been able to withstand. Because delinquencies have already started to rise in credit card debt.

The good news is that while delinquencies have started to rise, in comparison to the previous years, it still remains well below average. And that has kept most pundits and rating agencies relatively quiet. Indeed, the rating agencies in particular have pointed out that while they expect delinquencies and charge-offs to rise, banks are strong enough in terms of capital to handle that and most will prudently provision in expectation of that. And that seems all well and good, but what that doesn’t take into account is the future damage that will be done to corporations that suddenly see a drop in demand from a bruised consumer, rising defaults in asset backed deals, and how much it might hurt the overall economy which causes its own ripples throughout all the sectors and asset classes.

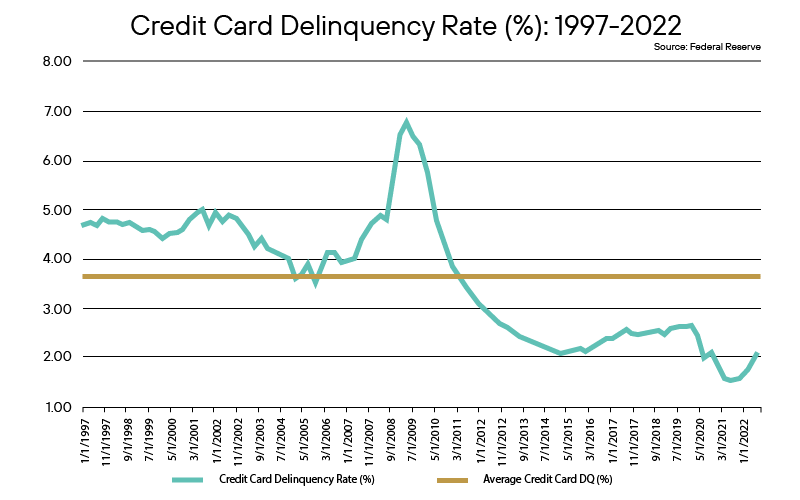

History tends to repeat itself. We’ve seen cycles such as this before. The credit card data is an early way to see just how cracks are beginning to manifest itself around us in terms of consumer credit and an early warning bell on some future stress in the overall economy. Long-term, we continue to expect fallout to be felt more at the lower end of the credit spectrum in terms of corporate credit, and as such, see more future spread widening in that area. Short-term, we would expect with investors sitting on cash an eagerness to re-engage in the market, and as such, we should see initial credit spread tightening as part of that exuberance. However, as more and more signs of weakness emerge, such as the credit card delinquencies, we would expect a market pull back in risk and some spread widening. With that as a backdrop, we continue to deploy a conservative approach, focusing on liquid, high quality corporate names able to withstand any credit turbulence and legacy issue ABS in order to avoid the pitfalls of more relaxed underwriting standards potentially found in newer issuance.

|

|

Definition of Terms

Basis Points (bps) – refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature – A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) – A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) – A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) – A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO – The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) – An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) – The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) – One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) – A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) – a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) – a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta – the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) – fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) – a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) – a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Net Asset Value (NAV) – represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 – The Standard and Poor’s 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX – The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ – The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index – The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei – The Nikkei is short for Japan’s Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan’s top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite – is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

MOVE Index – The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index – The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average – The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng – The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 – The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 – The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) – is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk – the name economists give to the risk associated with the sensitivity of a bond’s price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) – the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) – the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) – high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) – an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) – an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) – a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) – an organization that invests in small- and medium-sized companies as well as distressed companies.

Control #: 16279452-UFD-01/17/2023