“It’s always consoling to know that today’s Christmas gifts are tomorrow’s garage sales.” - Milton Berle

We have officially entered the holiday season. I know this because all I have to do is walk my local supermarket’s aisles to see the staff frantically putting up Santa cut-outs right next to the display case of Butterball frozen turkeys they were frantically still trying to move days before Thanksgiving. “Santa prefers Butterball, accept no substitutes.” We are an impatient group to begin with, and the holidays seem to make it worse. I tend to blame technology. We don’t just want goods delivered faster; our expectation is that we will be told the news they’re being delivered sooner. Certainly, the financial markets are a prime example of that. We have noted over the recent past the almost daily flip-flopping in the market between inflation worries and recession. I was reminded further of that recently with the Fed formally completing its most recent and expected 75 bps hike. We are now seeing expectations for the December hike to be in the 50-bps range. More importantly, the market is expecting not only for the Fed to slow down its hiking campaign, but for language to be a bit more dovish. So, give me the rate hike, the goods, and then give me the news we need to retreat at the same time. Yeesh, it’s like the market treats the economy like a bag of jiffy pop microwave popcorn. Nevertheless, what did occur in the midst of all this rush was a risk asset rally, and that gave me a little bit of a pause.

As stated, we have seen some of this daily waffling between inflation/rate worries and recession/credit spread movement. But recently, it seemed the market had begun to embrace an economic slowdown expectation. While that doesn’t necessarily mean a full-blown recession, it had been enough to push market participants to ease off high yield, especially the deep junk area of CCC rated assets. Then, suddenly, out of the blue, toward the end of the month we witness an aggressive one-day breather from that and a screaming demand for risk assets noticeably rose again. Dealers were actively engaged in reverse inquiry, reaching out to accounts and asking about specific risk bonds. The instant chats on Bloomberg were more alive with bids than had been recently noted. For at least a day, the market seemed to have a totally different vibe than it had just 12 hours earlier. But one day was all it lasted. Just as quickly, we reverted back to smaller rate rallies and credit spread widening again. For a day, though, at least that day, the market suddenly found CCC to be a bargain again before just as quickly tossing them all back into the clearance rack.

High yield overall has had quite a run over the past few years, especially during the beginning of the pandemic; once government support got involved, that rally continued right up until the rate hike cycle began. The combination of the appearance of government support and historically low rates, proved too tempting for investors to ignore, and they eagerly plowed into high yield. Enough so that credit spreads compressed to historic tights. However, once the rate hiking cycle began, the shine came off the sector. Higher rates meant investors didn’t need to reach that deep into the credit stack to make targeted returns. One could step up in credit quality, make significant returns, and better yet, not worry that higher rates might impact these junk issuers’ credit profiles.

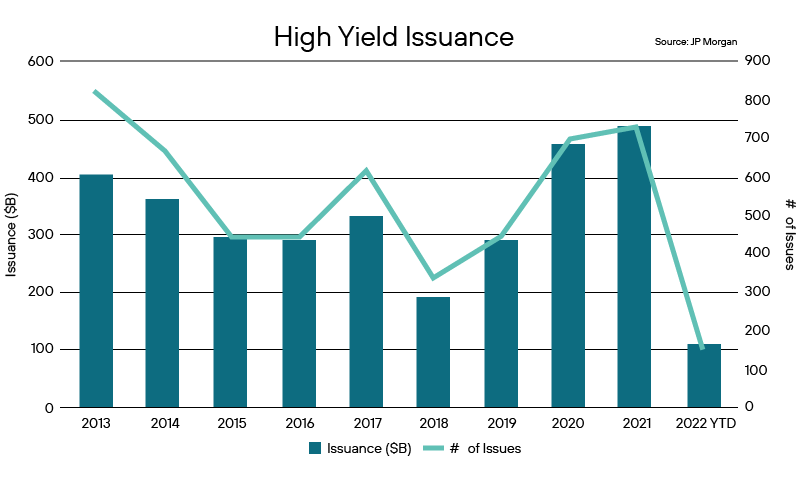

As illustrated in the chart below, for 2020 and 2021, the sheer amount of high yield issuance climbed to levels not seen in the last decade, not only in terms of absolute issuance but also in number of issues hitting the markets. A clear example of demand being met by supply. However, once 2022 rolled around, and we began to bear witness to an aggressive Fed hiking rates, demand for new issue paper evaporated. Not only were investors not so interested in high yield new issuance, but the issuers themselves, due to the higher rates, began to step back.

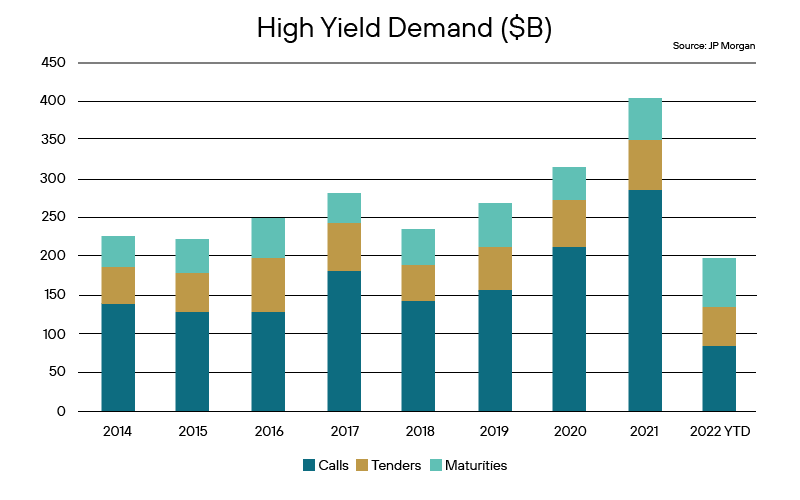

And in fact, the majority of new issuance in high yield for 2022, muted as it is, was mostly accomplished to roll whatever maturities were upcoming. A departure from the previous go-go years, where issuers rightfully took advantage of the low-rate environment to aggressively refinance debt by utilizing call provisions and offering tender options.

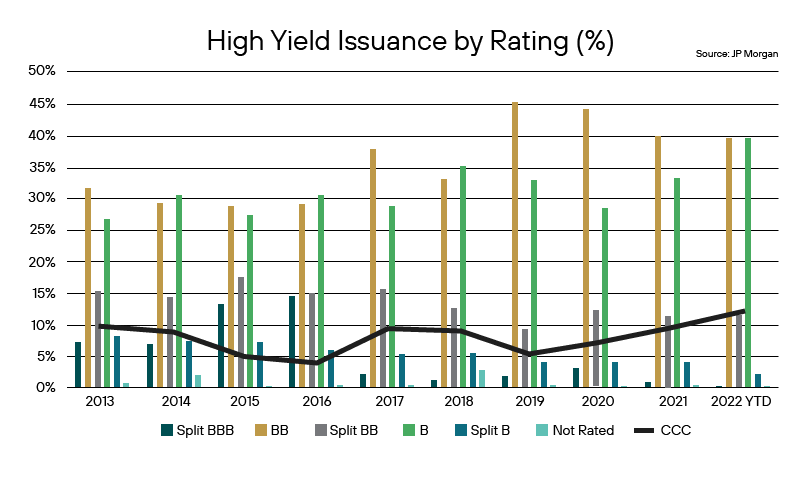

This is especially true in the lower depths of high yield. Illustrated below, issuance is broken out in various categories in high yield. Those with CCC ratings over the past 10 years or so have averaged slightly under 9% historically from the standpoint of market share of high yield issuance. For CCC, year-to-date numbers look strong at over 12%. However, that number is quite misleading, and was all front loaded at the beginning of the calendar year 2022. Since June, in fact, CCC credits have 0.0% new issuance, according to JP Morgan. A number most likely to be repeated over the near-term, given where rates are.

With demand slowing, that in itself would make the CCC credit outlook not so palatable from a new issue standpoint. However, as we slowly roll toward what most market participants anticipate being a slower growing economy, and potential of some version of a recession, there is also the added risk of credit deterioration for these credits to deal with. That concern is already quite evident in the data. In October of 2022, Standard & Poor’s reported that the number of CCC+ and below corporate issuers increased to 148 from the 140 reported in September 2022, meaning downgrades continue to increase. Since the beginning of 2022, there have been many familiar names hitting the downgrade list into CCC territory, including Carvana, Bausch Health Companies, Talen Energy, Rite Aid, Bed Bath and Beyond, National CineMedia, and Party City, to name but a few. This has resulted, according to S&P, in total debt outstanding of CCC+ and below issuers to now have reached a 17-month high of $230 billion in October 2022, up from $134 billion at end of September 2022. There is certainly the potential for more, given that outstanding debt rated B- with a negative outlook increased to $77 billion from $68 billion in the same time period.

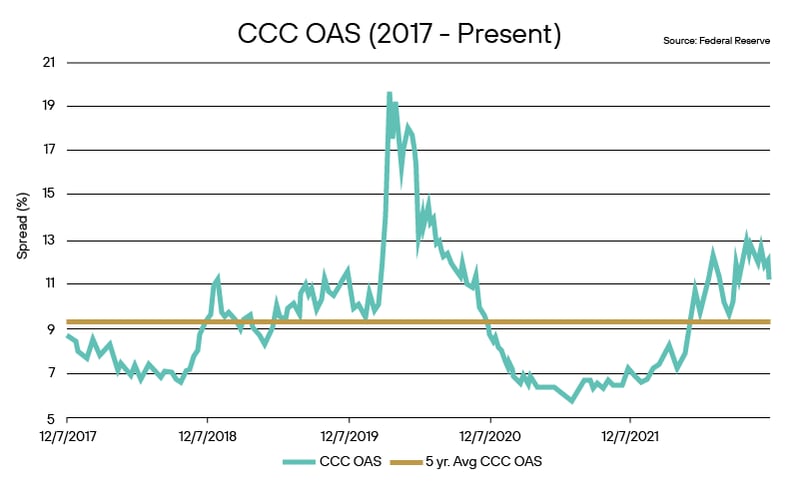

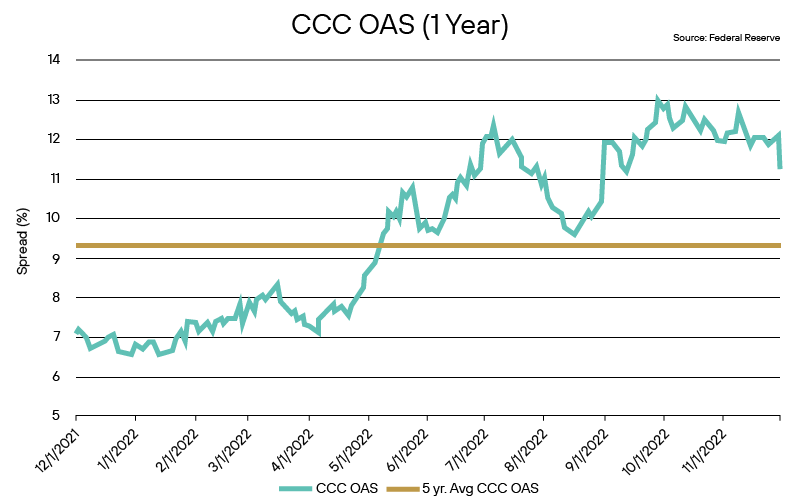

Furthermore, with demand evaporating and concerns of credit risk rising, credit spreads are widening at an ever quickening pace. Simply put, the risk is rising, and investors are demanding wider and wider spreads in order for whatever limited amount of CCC credit does trade in the secondary market to compensate them for that risk more and more. Indeed, as is clear in the chart below, during 2020 and into the end of 2021, one can see that the CCC Option-Adjusted Spread (OAS) is far below the 5-year average of 931 bps. But since that time, spreads widened out well over the 5-year average and at one point approached nearly 400 bps wider. While certainly spreads were wider in the early part of the pandemic, it is important to note that the recent credit spread widening isn’t due to a current crisis, but rather in anticipation of something stirring.

Certainly, that is obvious when comparing spreads over the past 5 years. Likewise, it’s even more notable when one looks at those spreads over the past year, where concerns become more amplified during rate hikes that captured investor attention and allowed them to shun excessive credit risk, move into less risk, and still pick up yield.

As one contemplates what is to come in the new year, there is an expectation that the economy will slow. A slowing economy does not in itself indicate a full blow recession, and so perhaps the credit carnage some are calling for will not manifest itself. Nevertheless, the question higher rates allow all investors to ask is: why risk the chance? If a slowing economy is the outcome of what is to come, however, it would make sense that while some credit slippage is to occur, it will not be a full meltdown. But what does that really mean? Most likely that means that while high grade credit should be relatively stable, as you move down the credit stack you will be witness to increasing volatility. As such, one should consider that the very bottom of the credit stack is the most to be concerned with. That should mean the CCC will be the most vulnerable, with some risk that the downturn will reach slightly upwards from there into the single B part of the stack and certain weaker issuers in the space. As a result, we would continue to expect not only further credit spread widening but an increasing number of credit defaults and bankruptcies.

As we have discussed over the past 9 months, we have found far more value in the more conservative part of the credit stack. We feel high grade, highly liquid investment grade credits, are preferable as we await not only the end of the rate hike cycle but also the ripple effects and full impact of the Fed rate hikes already accomplished. We believe CCC credit spreads will continue to widen, and the limited issuance, with a limited demand to meet it, means there is little means to reset the message in that part of the credit stack any time soon, and it certainly won’t be able to buttress against the expected additional negative headlines to come from more fallen angels. Simply put, it’ll be difficult for CCC’s to regain their footing for a while.

|

|

Definition of Terms

Basis Points (bps) – refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature – A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) – A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) – A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) – A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO – The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) – An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) – The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) – One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) – A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) – a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) – a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta – the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) – fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) – a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) – a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Net Asset Value (NAV) – represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 – The Standard and Poor’s 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX – The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ – The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index – The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei – The Nikkei is short for Japan’s Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan’s top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite – is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

MOVE Index – The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index – The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average – The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng – The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 – The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 – The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) – is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk – the name economists give to the risk associated with the sensitivity of a bond’s price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) – the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) – the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) – high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) – an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) – an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) – a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) – an organization that invests in small- and medium-sized companies as well as distressed companies.

Control #: 16116734-UFD-12/13/2022