“I’ve had a lot of worries in my life, most of which never happened.” -Mark Twain

Halloween has come and gone. It’s a lot of build-up around where we are; lots of lawn ornaments, a few haunted houses, a lot of candy. It seemed creepier when I was younger and the streets were definitely darker; we didn’t go out until dark. Now I get the doorbell rung in the afternoon. The costumes in the past seemed more homemade, more basic, and maybe that’s why they seemed more macabre. Costumes today seem more elaborate with a Disney bias. Maybe it’s just my age. When you are younger, every sound in the house, especially this time of year, would raise a few hairs on the back of your neck. You didn’t know what the sound was, but it surely wasn’t good news. As an adult these days, I’m fairly certain the sound is either the washing machine downstairs; an acorn falling off a tree, hitting my house and mocking me for attempting to rake up their leaf brethren; or a maniac coming through a window I left open. Frankly none of those are getting me to leave my chair these days. It’s that type of realization that makes me wonder how much are we missing simply because we think we have heard or seen it all? And yet, these days in the market, there are plenty of noises and bumps in the night we should probably pay a little bit more attention to. In fixed income, we tend to worry more about the noises because it means we are potentially missing something bad, but it doesn’t have to be. And indeed, opportunity doesn’t always knock, sometimes it simply makes a noise in the attic.

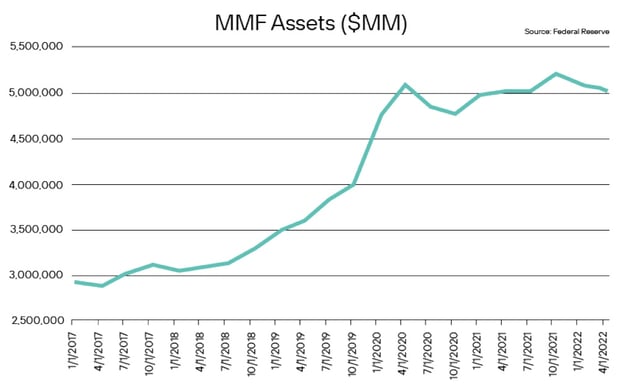

The short end of the market is where most of the noise has been the past 15 months with most of the pain of the rate hikes having settled there. The hikes have obviously played havoc with bond valuations for most of the fixed income world. For those of us holding floating rate securities, the rate hikes have been an opportunity for those securities to reset at higher coupons, with future higher yields to be captured as the lag between resets is caught up with. There is also supposed to be one large group of investors who would or should benefit more from this than others, money market funds (MMFs). MMFs are typically a place where cash is drawn to during times of crisis and as a resting spot for future investment endeavors during periods of volatility such as these. And this time around, MMFs are certainly seeing the asset flows in with MMF assets, including prime funds (credit funds) and government MMFs, which, as an industry, are now well over $5.0 trillion in size. This is a dramatic increase from 5 years ago when total assets in MMF were less than $3.0 trillion. One would think these should be salad days for the industry; large asset in-flows and spiking rates. And yet, as we shall see, this is a moment MMFs don’t really love. These are not the sounds they like to hear.

The only thing MMFs dislike more than periods of large unplanned out-flows, is short, dramatic periods of massive in-flows. We’ll circle back to the reason for that shortly.

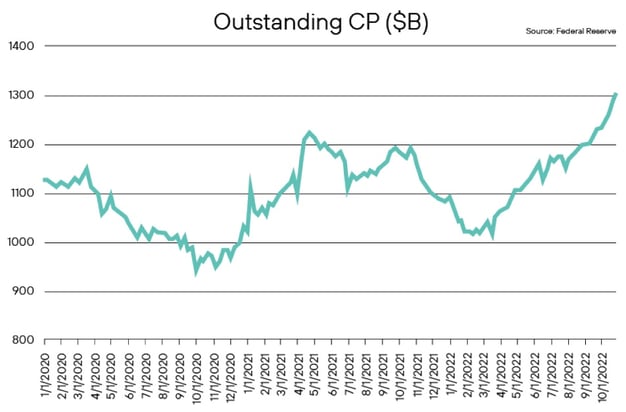

Opportunity should also be by-product for corporate borrowers. With large balances in MMFs and higher rates, one would expect corporate issuers to once again flock to the cheaper Commercial Paper (CP) market to get funding. Over the past few years, with low rates, corporate borrowers eschewed the CP market to lock in longer term debt and advantageous levels. With rising rates over the past 15 months, and large MMF asset balances, we would expect supply and demand to find a happy marriage. And we are seeing a large increase in CP issuance.

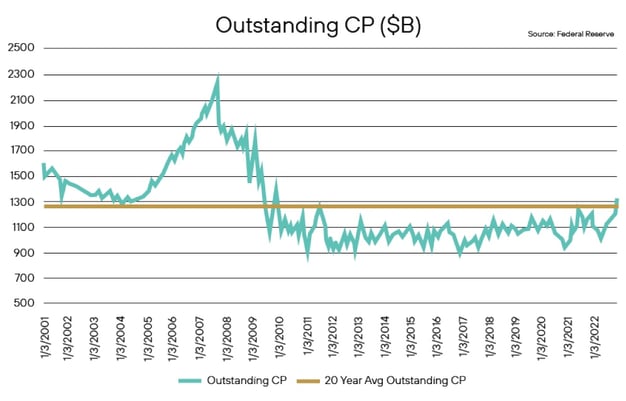

It’s important to put that into perspective. Certainly, CP would seem to be at a 3 year high of around $1.3 trillion, but when we look back 20 years, the current high is around the average we have seen over a 20 year period and far below the nearly $2.3 trillion in 2007.

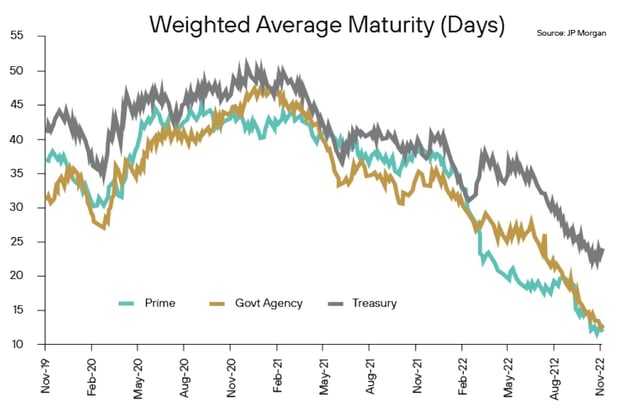

So the question would present itself, “why aren’t we seeing this increased supply being gobbled up at higher rates by MMFs? Why aren’t they taking advantage and causing even more supply to be issued?” Because the biggest fear, as alluded to above, for MMFs is getting too much money too fast. Managers of MMFs know that large unexpected in-flows of money coming in at high velocity are very likely to leave at just as fast a pace. So the first thing MMFs do is make sure, if they do invest in something, to not do so too far out maturity-wise. That is what they are doing, making it very difficult for corporations and banks to properly ladder the front end of their liability structure or fully take advantage of the shorter, cheaper debt they’d like to issue. In fact, JP Morgan is reporting that as of the first week of November banks have secured only about 64% of their CP/Certificates of Deposit (CD) funding needs over year-end. That compares to 62% at this time in 2020 and 60% in 2021. Another example? Below is a chart from JP Morgan highlighting the shrinking weighted average maturity in terms of days for the money market fund universe. As more and more cash has hit these funds, the less and less they want to invest it further out than a few days.

Not only are they unwilling to lend too far out, but they do so in a manner that isn’t necessarily taking full advantage of the spike in short term rates. For a reason. MMFs, after a few issues over the past few years, have seen their investment parameters and limits fall under tighter and tighter regulation, especially with regards to “liquidity buckets.” A dirty secret of the industry is that many of the things they do invest in tend to be illiquid. Commercial Paper and Certificates of Deposit are large investments for the sector, and they tend not to be so easily tradeable in the secondary market. The reason can be that some of those investments tend to be more one-off than you would think; CDs for instance. The other is that because it is a smaller universe than one would think, that if one large MMF has to liquidate a large exposure to a CP issuer, chances are they are all going to be doing it; thus, who would you sell to?

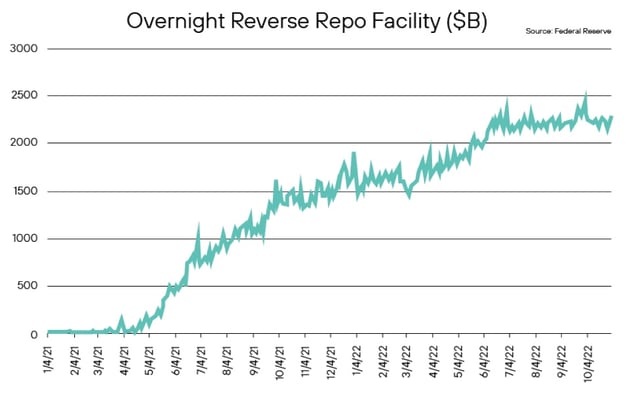

Some of these subjects we have broached before, and so no need to discuss too much further. With large flows of investible cash, MMFs are once again hitting a new favorite that has become an old favorite: the Federal Reserve Overnight Reverse Repo Facility (RRP). MMFs tend to shelter here in times of stress, even ones brought on by simply having too much cash to invest. The RRP has the advantage of offering a safe quiet place to hide with no real credit risk and is consistently available. As can be seen below, usage of the RRP has seemingly moved in lock-step with in-flows.

In fact, according to JP Morgan, the usage of the Facility now represents across the MMF sector the highest exposure across its prime MMF sub-sector. As seen below, the RRP now represents some 32% of the asset allocation in prime MMFs, the largest exposure.

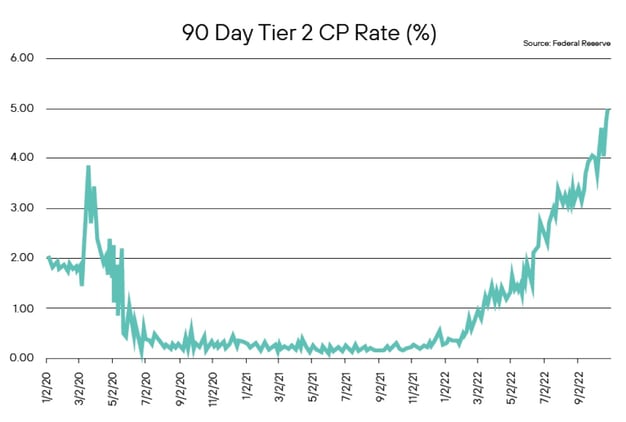

Thus at a time MMFs could finally be taking advantage of higher yields, they need to rightfully protect against large outflows and thus be far more conservative in response. How much yield are they leaving on the table? The current rate on the Federal Reverse Repo Facility is 3.80%, compared to the 90 day commercial paper rate of around 5.0%.

And so, the bump we hear in the attic is opportunity. The CP market and its issuers are in need of short-term funding, especially over year-end. Utilizing the short-end of the market to help capture robust yield in high credit quality issuers is an opportunity that is typically too crowded for other types of investors to participate in, with that overcrowded field normally pushing yields lower and lower due to the large prime MMFs muscling in. But that type of investor is busy dealing with concerns that the sudden influx of cash they received today will leave tomorrow. Given the state of MMF and the upcoming turn of the calendar, we expect spreads/yields to continue to widen as those corporations and banks desperate to get funding over the turn widen offerings out to get their funding needs met. Taking advantage of MMFs choosing to stay on the sideline is a means to take what the market is offering and build front-end liquidity for longer funds.

Keeping an open mind and realizing that opportunities exist across markets allows us to keep our powder dry for potentially bigger total return type opportunities, especially once the calendar enters the new year. Understanding that future yield widening will be available allows us to lock in solid current value and keep powder dry and liquid for near term opportunities that offer total return value. The goal continues to be to focus on creating future overperformance, and keeping the funds in highly liquid, high quality exposures. This type of trade gives us the flexibility to accomplish just that.

|

|

Definition of Terms

Basis Points (bps) - refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Curvature - A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

Mortgage-Backed Security (MBS) - A mortgage-backed security is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them.

Collateralized Loan Obligation (CLO) - A collateralized loan obligation is a single security backed by a pool of debt.

Commercial Real Estate Loan (CRE) - A mortgage secured by a lien on commercial property as opposed to residential property.

CRE CLO - The underlying assets of a CRE CLO are short-term floating rate loans collateralized by transitional properties.

Asset-Backed Security (ABS) - An asset-backed security is an investment security—a bond or note—which is collateralized by a pool of assets, such as loans, leases, credit card debt, royalties, or receivables.

Option-Adjusted Spread (OAS) - The measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option.

Enhanced Equipment Trust Certificate (EETC) - One form of equipment trust certificate that is issued and managed through special purpose vehicles known as pass-through trusts. These special purpose vehicles (SPEs) allow borrowers to aggregate multiple equipment purchases into one debt security

Real Estate Investment Trust (REIT) - A company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors.

London InterBank Offered Rate (LIBOR) - a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

Secured Overnight Financing Rate (SOFR) - a benchmark interest rate for dollar-denominated derivatives and loans that is replacing the London interbank offered rate (LIBOR).

Delta - the ratio that compares the change in the price of an asset, usually marketable securities, to the corresponding change in the price of its derivative.

Commercial Mortgage-Backed Security (CMBS) - fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

Floating-Rate Note (FRN) - a bond with a variable interest rate that allows investors to benefit from rising interest rates.

Consumer Price Index (CPI) - a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them.

Net Asset Value (NAV) - represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities.

S&P 500 - The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 large companies listed on exchanges in the United States.

German DAX - The DAX—also known as the Deutscher Aktien Index or the GER40—is a stock index that represents 40 of the largest and most liquid German companies that trade on the Frankfurt Exchange. The prices used to calculate the DAX Index come through Xetra, an electronic trading system.

NASDAQ - The Nasdaq Stock Market (National Association of Securities Dealers Automated Quotations Stock Market) is an American stock exchange based in New York City. It is ranked second on the list of stock exchanges by market capitalization of shares traded, behind the New York Stock Exchange.

MSCI EM Index - The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,382 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Nikkei - The Nikkei is short for Japan's Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan's top 225 blue-chip companies traded on the Tokyo Stock Exchange.

Shanghai Composite - is a stock market index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange.

MOVE Index - The ICE BofA MOVE Index (MOVE) measures Treasury rate volatility through options pricing.

VIX Index - The Cboe Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX).

Dow Jones Industrial Average - The Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Hang Seng - The Hang Seng Index is a free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong.

STOXX Europe 600 - The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Euro STOXX 50 - The EURO STOXX 50 Index is a market capitalization weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

CAC (France) - is a benchmark French stock market index. The index represents a capitalization-weighted measure of the 40 most significant stocks among the 100 largest market caps on the Euronext Paris (formerly the Paris Bourse).

Duration Risk - the name economists give to the risk associated with the sensitivity of a bond's price to a one percent change in interest rates.

Federal Open Market Committee (FOMC) - the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy specifically by directing open market operations (OMO).

United States Treasury (UST) - the national treasury of the federal government of the United States where it serves as an executive department. The Treasury manages all of the money coming into the government and paid out by it.

High Yield (HY) - high-yield bonds (also called junk bonds) are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they must pay a higher yield than investment-grade bonds to compensate investors.

Investment Grade (IG) - an investment grade is a rating that signifies that a municipal or corporate bond presents a relatively low risk of default.

Exchange Traded Fund (ETF) - an exchange traded fund (ETF) is a type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same as a regular stock.

Federal Family Education Loan Program (FFELP) - a program that worked with private lenders to provide education loans guaranteed by the federal government.

Business Development Program (BDC) - an organization that invests in small- and medium-sized companies as well as distressed companies.

You should carefully consider the investment objectives, potential risks, management fees, charges and expenses of the fund before investing. The fund's prospectus contains this and other information about the fund and should be read carefully before investing. You may obtain a current copy of the fund's prospectus by calling 1-800-544-6060.

Fixed income investments are affected by a number of risks, including fluctuation in interest rates, credit risk, and prepayment risk. In general, as prevailing interest rates rise, fixed income securities prices will fall.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. There is no guarantee that this, or any, investing strategy will succeed.

Diversification does not ensure a profit or guarantee against loss.

There is no affiliation between Ultimus Fund Distributors, LLC and the other firms referenced in this material.

15981893-UFD-11/30/2022